Code okof is an old reference. New classifier-reference okof

The accountants of all Russia have been trying to solve the next puzzle since 01/01/2017.

From 01/01/2017 All-Russian classifier of fixed assets OK 013-94 has lost force. A new classifier came into force - OK 013-2014 (SNA 2008), approved by Order of the Federal Agency for Technical Regulation and Metrology of December 12, 2014 N 2018-st "On the adoption and implementation of the All-Russian Classifier of Fixed Assets (OKOF) OK 013 2014 (SNA 2008). "

On February 2, 2016, the government commission on the use of information technology to improve the quality of life and the conditions for doing business approved the direct and reverse transition keys between the editions of OK 013-94 and OK 013-2014 (SNA 2008) of the All-Russian Classifier of Fixed Assets (hereinafter - OKOF).

The 1C company, as always, took care of customers by including an assistant for OKOF replacement in the functionality of the program “Accountancy of State Institution 8” at the beginning of 2016.

At the December seminars in 2016, representatives of the Ministry of Finance of the Russian Federation explained that fixed assets received at the institution before 01.01.2017 should be transferred to the new OKOF using the transfer key, without changing their depreciation group and useful lives.

In software products, it was recommended that OKOF be replaced after the submission of statistical reports, because according to paragraph 5 of the Guidelines for filling out the federal statistical observation form No. 11 “Information on the presence and movement of fixed assets (funds) and other non-financial assets”, approved by order of the Federal State Statistics Service dated November 24, 2015 N 563, for the classification of fixed assets in the report for the 2015 reporting year, the classifier of fixed assets OK 013-94, introduced on January 1, 1996, is used. Decree of the Gosstandart of Russia of December 26, 1994 N 359 and valid until 01.01.2017.

When performing the conversion, methodological difficulties may arise when the old OKOF does not have a direct correspondence to the new one.

Two letters of the Ministry of Finance of the Russian Federation: Letter dated 02.27.2016 No. 02-07-08 / 78243 “On the introduction of a new All-Russian Classifier of Fixed Assets (OKOF) from January 1, 2017” and Letter dated 02.30.2016 No. 02-08-07 / 79584 in addition to the letter of the Ministry of Finance of Russia dated December 27, 2016 No. 02-07-08 / 78243 on the transition to the new classifier of fixed assets in 2017, clarify the situation in cases of lack of correspondence between the old and the new OKOF.

Most institutions submitted statistical reports for 2016 and, in operating mode, transcoded OKOF in the inventory card of the fixed asset.

And suddenly rumors began to appear that it was not necessary to recode the fixed assets, which are recorded on the balance sheet of the institution until 01/01/2017, it was necessary to leave them on the old OKOF.

In the institutions in which the transcoding was carried out, there began to be talk about the need to return everything back, and the old OKOFs should be indicated in the fixed assets cards.

When clarifying the sources of information, it was found that some consulting information systems in response to user questions about the search for conformity of the OKOF began to give strange answers, namely: “Yes, you do not need to change anything! Leave it as it is! "Keep records on the new OKOF from 01.01.2017, and do not touch the old fixed assets at all!”

This view was joined by numerous lecturers at seminars held in various parts of the country, referring to the above letters of the Ministry of Finance, apparently interpreting in their own way the phrase: “If material assets, which in accordance with Instruction 157n relate to fixed assets, are not included in OKOF OK 013-2014 (SNA 2008), then such objects are accepted for accounting as fixed assets with grouping in accordance with the All-Russian Classifier of Fixed Assets OK 013-94 ”.

Why this phrase was adopted as a guide not to make any changes is completely incomprehensible. It just says that you DO NOT need to rearrange fixed assets in accounting, but you should leave fixed assets in those accounts on which they were recorded before 01.01.2017.

But the accountants have already had doubts, and in cases of a large number of fixed assets with OKOF that do not have a new edition, these doubts have become a firm belief that nothing needs to be done, no transcoding should be done, and in general, return everything to us, as it was!

In order to prevent incorrect information, we offer several undeniable arguments in favor of the fact that the OKOF of fixed assets that are recorded on the balance sheet of an institution before 01.01.2017 still needs to be changed.

In the section on the line with the code 040 "OKOF Code", the code of the real estate object is indicated in accordance with the All-Russian Classifier of Fixed Assets. The line to fill looks like this:

As can be seen in the figure, the structure of the OKOF of real estate should comply with OK 013-2014 (SNA 2008). And since real estate is not from the list of the most frequently acquired non-financial assets by the institution, and most likely, this section reflects information on real estate registered by the institution until 01/01/2017, therefore, there can be no question that OKOF of these objects should not be converted to new ones.

We remind you that to replace OKOF in fixed assets, you should:

1.Download the new OKOF classifier

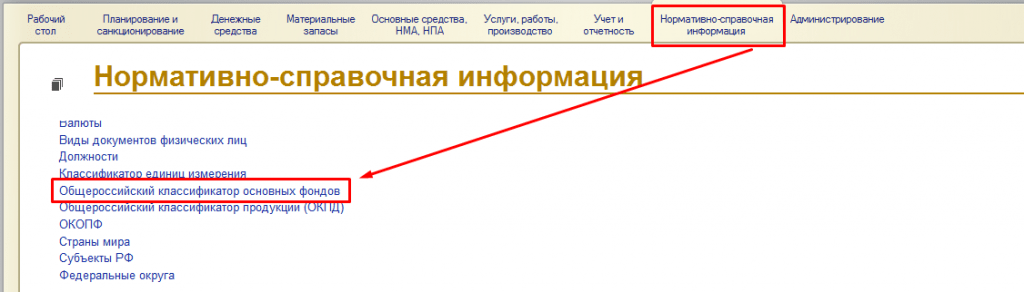

Section "Normative and reference information" - link to the navigation bar "All-Russian Classifier of Fixed Assets"

On the command panel, click the "Download Classifier" button and in the window that appears, specify the path to the okof.xml file, which is located in the program update release folder.

Select the okof.xml file and click the "Open" button.

Then you should click on the button “Download data”.

The download of the directory will begin, which, depending on the location of the information base, as well as on the system characteristics of the computer, can take from several minutes to a long time.

Accounting of a public institution (rev. 1)

The menu item "Fixed assets" - "OKOF"

In the classifier window, click the "Download Classifier" button, set the flag in the appropriate position and click the "Next" button

Using the "Add" button, specify the path to the configuration update release folder containing the okof.xml file and click the "Next" button.

After the classifier is loaded, the “Finish” button is pressed.

After loading, the directory “All-Russian Classifier of Fixed Assets” will contain two classifiers: OK 013-2014 and OK 013-94.

2. Use the OKOF replacement assistant

Accounting of a public institution (rev.2)

Section "Administration" - subsection "Changing the law" - link "Assistant replacing OKOF"

In the assistant window, click on the "Fill" button to fill the tabular section with the list of OKOF from the elements of the "Fixed Assets" directory of the specified institution. If there is no corresponding position OK 013-2014 in the transition key, the necessary position should be selected from the classifier manually, after selecting codes that are identical in value. It is recommended to fix such positions on a commission basis.

The All-Russian Classifier of Fixed Assets OK 013-94 is a regulatory document, which is the main classifier of fixed assets in Russia and was applied until January 1, 2017 ( old (inactive) version).

The All-Russian Classifier of Fixed Assets OK 013-94 is part of the Unified System for the Classification and Coding of Technical, Economic and Social Information (ESKK) of the Russian Federation.

The all-Russian classifier of fixed assets is often referred to in abbreviated form - OKOF.

A comment

The All-Russian Classifier of Fixed Assets OK 013-94 was approved by Decree of the State Standard of the Russian Federation of December 26, 1994 N 359. This version of the classifier was applied until January 1, 2017 (from this date the new version of OKOF - is applied).

The order of the FEDERAL AGENCY FOR TECHNICAL REGULATION AND METROLOGY dated April 21, 2016 No. 458 approved direct and reverse transition keys between the editions of OK 013-94 and OK 013-2014 (SNA 2008) of the All-Russian Classifier of Fixed Assets.

OKOF is the main classifier of fixed assets (fixed assets) in Russia. Under fixed assets understand the means of durable labor (over 12 months).

In modern documents, the term "" is used. OKOF uses the term “fixed assets”, but in exactly the same meaning. The fact is that in the days of the USSR it was the term “fixed assets” that was used for the same assets. OKOF has inherited this term.

When developing the OKOF, the following were taken into account: International Standard Industriel Classification of all Economic Activities (ISIC), International Basic Product Classification (CPC), Central Product Classification (CPC), United Nations standards for international system of national accounts (SNA), the Regulation on accounting and reporting in the Russian Federation, as well as the All-Russian Classifier of Economic Activities, Products and Services (OKDP), for which ISIC and CPC are used zovymi.

The objects of classification in OKOF are fixed assets.

Fixed assets are assets produced that are used repeatedly or continuously for a long period, but not less than one year, for the production of goods, the provision of market and non-market services. Fixed assets consist of tangible and intangible fixed assets.

Material fixed assets (fixed assets) include: buildings, structures, machinery and equipment, measuring and regulating instruments and devices, dwellings, computers and office equipment, vehicles, tools, production and household equipment, working, productive and pedigree cattle, perennial plantations and other types of tangible fixed assets.

Intangible fixed assets (intangible assets) include computer software, databases, original works of the entertainment genre, literature or art, high-tech industrial technologies, other intangible fixed assets that are objects of intellectual property, the use of which is limited by the ownership rights established for them.

OKOF for accounting and taxation

For taxation and accounting, OKOF is important in that it is a complete and regularly updated Russian classifier. Based on it, approved. Decree of the Government of the Russian Federation of 01.01.2002 N 1. is used to determine the object, which allows you to determine on the basis of which is charged for income tax. Classification can also be used for accounting.

Example

We determine the depreciation group of the purchased household air conditioner. There is no such object (since there are enlarged groups of fixed assets up to the class level). In OKOF we find under the code 16 2930274 "Air conditioners household". This type of fixed assets is included in the class "Household appliances" with the code OKOF 16 2930000.

In the group of fixed assets with code 16 2930000, "household appliances" refers to the third depreciation group. So household air conditioning belongs to the third depreciation group (the useful life is more than three and up to five years).

All-Russian Classifier of Fixed Assets OK 013-94

Each OKOF item includes a nine-digit digital decimal code (OKOF code), control number (CN) and name. The control number is calculated in accordance with the current methodology for calculating and applying control numbers to protect classifier codes.

The OKOF code structure consists of 9 characters (digits). A space is placed between the second and third characters of the code.

The general structure of nine-digit codes for the formation of groupings of objects in OKOF is presented in the form of the following scheme:

X0 0000000 - section

XX 0000000 - subsection

XX XXXX000 - Class

XX XXXX0XX - subclass

XX XXXXXXX - view.

Groupings of objects in OKOF up to the level of subclasses are constructed according to the hierarchical classification method, and at the level of types, facets (lists) are used with their binding to the lower level of the hierarchical structure of the classifier - to subclasses within the code interval allocated for this subclass.

Sections are the highest level of division, formed taking into account the classification of fixed assets adopted in the SNA.

OKOF two section:

1- tangible fixed assets

2 - intangible fixed assets

Subsection represents the level of division of classification objects, taking into account their significance for the economy as a whole and established traditions.

Section 1 “Material fixed assets” presents the subsections:

11,000,000 BUILDINGS (EXCEPT RESIDENTIAL)

12 0000000 STRUCTURES

13,000,000 HOUSES

14 0000000 MACHINERY AND EQUIPMENT

15 0000000 VEHICLES

16 0000000 INVENTORY PRODUCTION AND ECONOMIC

17 0000000 CATTLE WORKING, PRODUCTIVE AND BREED (EXCEPT YOUNG AND CATTLE FOR SLAUGHTER)

18 0000000 PLANTS PERENNIAL

19 0000000 MATERIAL BASIC FUNDS NOT INCLUDED IN OTHER GROUPINGS

Section 2 “Intangible fixed assets” presents the subsections:

20 0000000 NON-MATERIAL MAJOR FUNDS

21,000,000 GEOLOGICAL - EXPLORATION

22 0000000 COMPUTER SOFTWARE

23 0000000 ORIGINAL WORKS OF THE ENTERTAINMENT GENRE, LITERATURE OR ART

24 0000000 SCIENTIFIC INDUSTRIAL TECHNOLOGIES

25 0000000 NON-MATERIAL MAJOR FUNDS OTHER

Classes provide detailing of classification objects and may be the least significant level of their classification. The classes of fixed assets are formed mainly on the basis of the corresponding classes of products according to OKDP.

In cases where the OKOF class consists of groups represented in various OKDP classes or does not have an analogue in OKDP due to the specifics of fixed assets, the OKOF class code has the following structure: XX 000X000.

Subclass reveals with necessary detail the selected class.

View provides detailing of classification objects necessary for performing accounting functions, without switching to specific types of objects.

Example

15 0000000 VEHICLES - section and subsection (15)

Inside the subsection "VEHICLES"

15 3410000 Cars - class (15 3410)

15 3410010 Passenger cars - subclass (15 3410010)

Inside the subclass "Cars" types:

15 3410100 Passenger cars of especially small class (with engine displacement up to 1.2 l)

15 3410101 Passenger cars, especially small class for individual and official use

15 3410110 Passenger cars of small class (with an engine displacement of more than 1.2 to 1.8 liters inclusive)

15 3410020 Trucks, road tractors for semi-trailers (general purpose vehicles: flatbed, vans, cars - tractors; cars - dump trucks) - subclass

Example

15 3510000 Ships - class

15 3511000 Commercial and passenger vessels - class

15 3511010 Self-propelled marine vessels - subclass

15 3511011 Self-propelled marine dry cargo vessels - subclass

15 3511102 Sea and cotton log carriers - view

Example

We determine the depreciation group of construction equipment “formwork”. Formwork (from “deck”, “formwork” - covered with flooring from boards, etc.) - a set of elements and parts designed to give the required shape to monolithic concrete or reinforced concrete structures being erected at a construction site.

In this class of fixed assets there. Turning to OKOF, we find that “formwork” is listed under OKOF 14 2924243. To determine the depreciation group, you need to determine which class, subclass OKOF 14 2924243 belongs to?

Based on the OKOF, we determine that this code belongs to class 14 2924000 “Machines and equipment for the mining industry, construction and operation of quarries”, subclass 14 2924010 “Hoists and conveyors for mines, mining machines and equipment”.

The fixed assets with the OKOF code corresponding to subclass 14 2924010 “Hoists and conveyors for mines, tunneling machines and equipment” belong to the 2nd depreciation group (useful life of more than two and up to three years).

OK 013-2014 (SNA 2008). All-Russian Classifier of Fixed Assets (applicable from January 1, 2017)

The following code structure has been adopted at OKOF: XXX.XX.XX.XX.XXX

The first three characters correspond to the code for the type of fixed assets shown in table 1.

The following characters correspond to codes from the All-Russian product classifier by type of economic activity OKPD2 OK 034-2014 (CPA 2008) and can have a code length of two to nine characters depending on the length of the code in OKPD2. When you include positions in OKOF from OKPD2, a classification object should be formed that can be used as fixed assets.

If the objects of fixed assets do not have the appropriate groupings in OKPD2 or in the OKOF, their different classification is required, the fourth and fifth characters of the OKOF code have the value "0". Such fixed assets include expenses on land improvement, expenses on transfer of ownership of non-produced assets, research and development, and others.

For example, in OKOF there is a grouping "230.00.11.10 Costs of land reclamation works". For certain positions, OKOF provides explanations starting with the words "This grouping includes" (also includes, including includes, does not include).

SNA 2008 |

OKOF |

||

Alphanumeric designation |

The code |

Name of types of fixed assets |

|

AN111 |

Residential buildings |

RESIDENTIAL BUILDINGS AND ROOMS |

|

AN112 |

Other buildings and structures |

BUILDINGS (EXCEPT RESIDENTIAL) AND CONSTRUCTIONS, EXPENDITURES FOR IMPROVEMENT OF LANDS |

|

AN1121 |

Non-residential buildings |

BUILDINGS (EXCEPT RESIDENTIAL) |

|

AN1122 |

Other facilities |

STRUCTURES |

|

AN1123 |

Land improvements |

LAND IMPROVEMENT COSTS |

|

AN113 |

cars and equipment |

MACHINES AND EQUIPMENT, INCLUDING ECONOMIC EQUIPMENT, AND OTHER OBJECTS |

|

AN1131 |

Transport equipment |

VEHICLES |

|

AN1132 |

Information, computer and telecommunication (ICT) equipment |

INFORMATION, COMPUTER AND TELECOMMUNICATION (ICT) EQUIPMENT |

|

AN1133 |

Other machinery and equipment |

OTHER MACHINES AND EQUIPMENT, INCLUDING ECONOMIC INVENTORY, AND OTHER OBJECTS |

|

AN114 |

Weapon systems |

WEAPON SYSTEMS |

|

AN115 |

Cultivated Biological Resources |

CULTURED BIOLOGICAL RESOURCES |

|

AN1151 |

Resources of animals bringing products on a regular basis |

CULTURED ANIMAL ORIGIN RESOURCES PRODUCING PRODUCTS repeatedly. |

|

AN1152 |

Resources of trees, crops and plantations bringing products on a regular basis |

CULTIVATED VEGETABLE RESOURCES RESPONDINGLY TO PRODUCTS |

|

AN116 |

Costs related to transfer of ownership of non-produced assets |

TRANSFER OF PROPERTY RIGHTS TO UNPROFORED ASSETS |

|

AN117 |

Intellectual Property Products |

INTELLECTUAL PROPERTY OBJECTS |

|

AN1171 |

Research and development |

||

Find out which codes are not included in the new OKOF. The new classifier does not show the names of objects, but only their general purpose. Therefore, when choosing a code, an accountant needs to know "what is it for?"

With the release of the new classifier, the selection of the OKOF code has become even more exciting. A sharp reduction in the volume and detail of the classifier clearly shows that this detail is actually not needed by anyone, is not important and not interesting.

- Important article:

Let's consider in the article how to “guess” the accountant for the new OKOF.

Is there a correspondence between OKOF and the accounting account

The new classifier does not allow establishing an unambiguous correspondence between fixed assets accounts and OKOF codes (see table. 1). Therefore, officials issued transitional keys that must be used to determine the desired code. After all, the old classifier (OK 013-94) allows you to correlate the OKOF code and the accounting code.

Using a new OKOF, an accountant may encounter such a problem. It is impossible to draw a line between “Machines and equipment” and “Production and household equipment”. In the new classifier they were reduced to one group.

The only thing that can be done is to pick up the code according to the new classifier. And then using the reverse transition key to determine the code from the old OKOF. If the old code from group 16 corresponds to the selected new code, then the object should be assigned to “Production and household inventory”.

Table 1. OKOF codes and accounting accounts according to Instruction No. 157n

| OK 013-2014 | Instruction No. 157n |

||

| Name of types of fixed assets | Score | Name / Appointment |

|

| Residential buildings and premises | "Living spaces" |

||

| Buildings (except residential) | "Non-residential premises" |

||

| Facilities | "Buildings" |

||

| Land Improvement Costs | "Land" (this is not a fixed asset, but a kind of non-produced assets) |

||

| Vehicles | "Vehicles" |

||

| Information, computer and telecommunication (ict) equipment | "Cars and equipment" |

||

| Other machinery and equipment, including household equipment, and other objects | “Machinery and equipment” (except for single code items that can be attributed to “Production and economic inventory”) |

||

| Weapon systems | "Cars and equipment" |

||

| Cultivated animal resources that repeatedly produce products | “Other fixed assets” |

||

| Cultivated resources of plant origin, repeatedly producing products | “Other fixed assets” |

||

| Costs of transfer of ownership of non-produced assets | |||

| Research and development | |||

| Subsoil exploration and mineral reserve expenditures | “Investments in non-produced assets” |

||

| Software and Databases | “Intangible assets” (if there is an exclusive right) |

||

| Software | “Intangible assets” (if there is an exclusive right) |

||

| Database | “Intangible assets” (if there is an exclusive right) |

||

| Originals of entertainment, literature or art | “Intangible assets” (if there is an exclusive right) |

||

| Library Funds |

|||

| Other intellectual property | “Intangible assets” (if there is an exclusive right) |

||

| Library Funds |

|||

What OKOF code should not be searched

Before looking for a code in OKOF, make sure that a thing can be classified as a fixed asset (OS). Let me remind you that such an asset should:

- to be an independently functioning object (that is, not a permanent part, not a fixture, not belonging to another object);

- be used for longer than 12 months;

- relate to fixed assets in accordance with the accounting policies of the institution.

This is stated in paragraph 44 of Instruction No. 157n.

And should not:

- be included in the list of facilities that, according to Instruction No. 157n, relate to inventories regardless of the useful life (for example, chainsaws);

- to be disposable (that is, it is repeatedly or constantly used in activities).

If the object does not meet the listed criteria, you should not search for the code in OKOF. For example, take the OKOF code 310.30.92.20 "Wheelchairs, except for parts and accessories." Paragraph 99 of Instruction No. 157n states that vehicles for the disabled are classified as inventory. Therefore, it makes no sense to look for this code.

Table 2 shows the objects that the new OKOF does not need to be included in fixed assets. This list is far from complete. Previously, such assets were named as fixed assets. If material values \u200b\u200bare not included in the new OKOF, but according to the norms of Instruction No. 157n these are fixed assets, take objects for accounting as fixed assets.

Table 2. What should not be included in the OS

| OKOF code | Name |

| Metal sanitary equipment |

|

| Heating radiators |

|

| Other equipment and devices for heating and hot water supply |

|

| Enamelled cast iron bathtubs |

|

| Enamelled steel bathtubs |

|

| Sinks |

|

| Household washbasins |

|

| Small enameled shower trays |

|

| Outdoor Toilet Bowls |

|

| Hand torches, special technological purpose |

|

| Household sewing machines |

|

| Special mounting tool |

|

| Processors |

|

| Microprocessors |

|

| Internal storage devices |

|

| Sound and video recording equipment, reproducing |

|

| Radio complexes (musical centers) |

|

| Microphones |

|

| Loudspeakers |

|

| Headphones, headsets |

|

| Cabinets layout with installation |

|

| Tire fitting and tire repair tools |

|

| Equipment for regulation and road safety |

|

| Tourist tents |

|

| Sleeping bags |

|

| Carpet paths |

|

| Carpets and other textile floor coverings |

|

| Non-electric household appliances for cooking and heating plates |

|

| Special furniture for sitting with a metal frame |

|

| Ski poles |

|

| The equipment is refereeing, training and other for winter sports. Winter Sports Equipment |

|

| Injury, training and other equipment for acrobatics and gymnastics |

|

| Track and field equipment |

|

| Refereeing, training and other equipment for sports games |

|

| Cargo simulators |

|

| Exercise machines universal isometric |

|

| Sports equipment and supplies for educational institutions |

|

| Theatrical scenery, designs and props |

|

| Museum inventory |

|

| Library Inventory |

|

| Library shelving |

|

| Inventory for household purposes |

New OKOF for the purpose of the facility

The main method of finding the code is by the purpose of the asset. The new classifier is not as detailed as the previous one. It has 10 times less codes than the old one. And very often in the new OKOF it is not the name of the facility that is listed, but the general purpose of the group of facilities: “Equipment for ...”. Therefore, when choosing a code, an accountant needs to know not just “what is it”, but also “why is it needed”.

Example 1:

The facility acquired the Patriot PT SE24 Chopper. There is no chopper in the new classifier.

The accountant needs to find out what it is intended for and look for it by purpose. The description says: "Patriot PT SE24 is a highly reliable garden shredder designed to process small tree branches and bushes." So, you need to look for garden equipment in the classifier. By searching the fragment of “gardens” we quickly enough find the code 330.28.30.86.120 “Equipment for gardening not included in other groups”.

Search can be carried out not by the whole word, but by its fragment. Sometimes this method is even more effective. I will give an example how to determine the necessary code in this case.

Example 2:

A medical university received a device “Monobinoscope MBS-02” from a commercial organization.

Since this is medical equipment, the accountant conducted a search on the piece of "medical". He found code 330.26.60, "Equipment for irradiation, electrical diagnostic and therapeutic, used for medical purposes." But this is the group code. It is necessary to clarify the code to the fourth value. In the description of the purpose of the device, the accountant read: "... is intended for the prevention, diagnosis, rehabilitation therapy and treatment of functional visual disturbances ...".

It is unclear whether this device can be attributed to group 330.26.60 (its name contains the word “radiation”, and the name of the equipment that it includes includes the words “x-ray, alpha, beta or gamma radiation”). The accountant had to find out if such radiation is used in this device. From the documentation it follows that this device is exposed to bright light. So the group 330.26.60 is not suitable. As a result, he chose the code 330.32.50.21.112 "Therapeutic equipment."

Now many educational institutions put navigators on cars. Consider how to find the code for them.

Example 3:

An educational institution bought a navigator.

The accountant shortened the search bar to “navigat” and found the code 330.26.51.11 “Compasses to determine the direction; other navigational instruments and devices. ” The explanation for this code says that it includes navigation tools and devices for services such as the Galileo Global Positioning System (GPS), GLONASS or GLONASS / GPS.

How to use a direct transition key

The method of searching for the purpose of the subject is quite time-consuming and also not always effective. For example, you need to find the code for a completely ordinary subject such as a TV using the new OKOF. The only thing that can be found is 320.26.30.1 “Communication equipment, radio or television transmitting equipment”.

But the television does not transmit anything, it only receives. How to be? We remember that there were televisions in the old classifier. And then a direct transitional key comes to the rescue. This is a huge table where each of the codes according to the old classifier is assigned a code according to the new OKOF. At first glance, the algorithm is as follows:

- we find the code for the object according to the old classifier;

- using the direct transitional key, we determine the corresponding code according to the new classifier.

In fact, everything is not so simple.

- The new classifier is much “poorer” than the old. Therefore, the new codes found by the direct transitional key can greatly surprise the accountant.

- In many cases, the direct transition key does not contain a specific code for the new classifier, but only gives a hint in which group to look for.

- The direct transitional key contains errors and typos.

So what code is assigned to the TV? The accountant can find the code 14 3230102 “Color TV sets” from the old classifier. According to the direct transitional key, this code corresponds to the new code 320.26.30.1 “Communication equipment, radio or television transmitting equipment”. That is, according to the new classifier, the TV still refers to the transmitting equipment.

Now we find the code for the air conditioner. They are in almost every institution.

Example 4:

The institution bought air conditioning. According to the classifier, on the first attempt, the accountant discovered code 330.28.25.1 “Heat exchangers; industrial equipment for air conditioning, refrigeration and freezing equipment. "

He was confused by the word "industrial." Then he found the code 330.28.25.12.110 "Industrial air conditioners." The accountant recalled that in the old OKOF there were domestic air conditioners. Indeed, this is code 16 2930274 "Air conditioners, domestic, electric air coolers."

Using the transient key for this code, you must independently determine the correspondence in the new codes from 330.28.23 to 330.28.29. However, in 50 positions, the accountant was able to find all the same “industrial” air conditioners. And also code 330.28.25.12.190 "Other equipment for air conditioning, not included in other groups." He applied it.

We’ll deal with musical instruments now. From “music”, the new OKOF contains only the building of a music school and musical works. The only way out is to look for the matching key for the old code 14 3692000 “Musical instruments” using the transitional key. Found the code 330.32.99.53 "Devices, apparatus and models intended for demonstration purposes"? Somewhere here, according to the direct transitional key, the pianos and accordions should also be “hiding”.

The currently existing All-Russian Classifier of Fixed Assets (OKOF) was approved by Decree of the State Standard of the Russian Federation of December 26, 1994 No. 359 (hereinafter - OK 013‑94) and has been used for 20 years. During this time, he repeatedly underwent adjustments. But experts have repeatedly pointed out that this classifier requires fundamental changes, since the terms and concepts in it do not correspond to realities. And then they waited. By the order of Rosstandart dated 12.12.2014 No. 2018-st, the new OKOF (OK 013-2014) was approved, which will come into force in 2017. Read more about the new classifier and the procedure for switching to new codes - in the material presented.

The new OKOF is developed in accordance with the United Nations System of National Accounts (SNA 2008), the European Commission, the Organization for Economic Co-operation and Development, the International Monetary Fund and the World Bank Group, as well as with the All-Russian Classifier of Products by Economic Activities (OKPD2) OK 034‑ 2014 (CPA 2008).

The introduction of the new OKOF is designed to ensure the transition of organizations to the classification of fixed assets adopted in international practice based on the 2008 SNA.

It is specified that public sector organizations should use the new OKOF for budget (accounting) accounting purposes in cases provided for by federal standards, unless otherwise established by authorized bodies of state regulation of accounting.

To date, several federal accounting standards have been developed for the public sector. Moreover, not one of them has yet been adopted. Drafts of such standards are available on the official website of the Ministry of Finance of the Russian Federation.

The mandatory use of OKOF for accounting (budget) accounting purposes is currently established by Instruction No. 157n. According to paragraphs 45, 53, 67 of Instruction No. 157n, the grouping of fixed assets and intangible assets for the purpose of accounting (budget) accounting by state (municipal) institutions is carried out according to the types of property corresponding to the classification subsections established by OKOF.

Changes in the OKOF Code Structure

The form and structure of OKOF codes will also change from 2017. If now the code consists of 9 characters, then from next year it will include 12.Based on the specified scheme, according to the current OKOF code corresponding to passenger cars (15 3410010), these objects belong to the subsection of the classifier 15 0000000 "Means of transport". Taking into account the requirements of Instruction No. 157n in accounting (budget) accounting, these objects should be taken into account on account 0 101 05 000 “Vehicles”. That is, now there is a relationship between the OKOF code and the number of the account for accounting for fixed assets.

If you look at the new OKOF code for the same cars, then there is no link between it and the account number. It is unclear how institutions will group fixed assets for accounting purposes, relying on the new OKOF.

Grouping of fixed assets in the new OKOF

The new OKOF includes 7 generalized types of fixed assets, some of which are further subdivided into subspecies. As indicated above, the code of the type (subspecies) of fixed assets forms the first 3 characters of the OKOF code. In the table, we consider in detail the name of the grouping types (subspecies) of fixed assets and find out whether they coincide with the subsections of the current OKOF.| Designation and name of groupings in the new OKOF | Description of groupings | Comparison with sections (subsections) of the current OKOF | |

| 100 "Residential buildings and premises" | Residential buildings and premises include residential premises and buildings or certain parts of buildings that are used wholly or mainly as places of residence, as well as any interconnected extensions and buildings and all fixed fittings and equipment installed in residential buildings | This group corresponds to subsection 13 0000000 "Housing" | |

| 200 "Buildings (except residential) and facilities, land improvement costs" | |||

| including | 210 "Buildings (except residential)" | This group includes whole non-residential buildings or parts thereof, not intended for use as housing and representing architectural and construction objects, the purpose of which is to create conditions (protection against atmospheric influences, etc.) for labor, social and cultural services for the population, storage material values, etc. | This group corresponds to subsection 11 0000000 “Buildings (except residential)” |

| 220 "Buildings" | Structures include engineering and construction projects erected with the help of construction and installation works. Structures are objects that are firmly connected to the ground. Examples of facilities include facilities such as highways, streets, roads, railways, and airfield runways; bridges, overpasses, tunnels; water mains, dams and other hydraulic structures; trunk pipelines, communication and power lines; local pipelines, mines and facilities for recreation, entertainment and leisure activities. The buildings also include historical monuments that cannot be defined as residential or non-residential buildings | This grouping corresponds to subsection 12 0000000 “Structures” | |

| 230 "Costs for land improvement" | This grouping includes the result of actions that lead to a significant increase in the quantity, improvement of the quality or productivity of the land or prevents its deterioration, for example, the costs of land reclamation, land clearing, land restoration, land relief (layout of the territory). These improvements cannot physically be separated from the land itself and do not lead to the creation of tangible assets (buildings, structures) that could be shown in balance sheets separately from the land itself | Now similar expenses are recorded under code 19 0009010 “Capital expenditures for land improvement (reclamation, drainage, irrigation and other works)” | |

| 300 "Machinery and equipment, including household equipment, and other objects" | |||

| including | 310 "Vehicles" | This group includes vehicles designed to move people and goods. | This group corresponds to subsection 15 0000000 "Means of transport" |

| 320 "Information, computer and telecommunication (ICT) equipment" | This grouping includes information equipment, complete machines and equipment designed to convert and store information, which may include electronic control devices, electronic and other components that are parts of these machines and equipment. | A separate grouping for the specified equipment has not been allocated in the current OKOF. Partially relevant equipment is now included in subsection 14 0000000 “Machinery and equipment” | |

| ICT equipment also includes various types of computers, including computer networks, independent data input-output devices, as well as communication systems equipment — transmitting and receiving equipment for radio communications, broadcasting, and television, and telecommunication equipment | |||

| 330 "Other machinery and equipment, including household equipment, and other objects" | This grouping classifies machines, equipment and devices that are not related to vehicles and ICT equipment. To reflect national characteristics, this group includes household equipment, that is, items that are not directly used in the production process, as well as production equipment, that is, technical items that are involved in the production process, but cannot be attributed to either equipment or facilities | This group includes the bulk of fixed assets that now refer to subsections 140000000 “Machinery and equipment”, 160000000 “Industrial and economic inventory” and 19 0000000 “Other material fixed assets” | |

| 400 "Weapon Systems" | These include fixed assets acquired for military purposes, such as weapons; controls for troops and weapons (fire); space rocket systems (complexes); military aircraft; equipment for taking off, landing and maintenance of aircraft; combat tracked and wheeled vehicles (tanks, infantry and landing fighting vehicles, etc.), etc. | There is no separate grouping for these objects in the current OKOF. Some objects related to weapons systems are now contained in subsections 140000000 “Machinery and equipment” and 150000000 “Means of transport” | |

| 500 Cultivated Biological Resources | |||

| including | 510 "Cultivated resources of animal origin, repeatedly producing products" | This group includes animals that repeatedly produce products and whose natural growth and restoration are under the direct control, responsibility and management of specific legal entities. Slaughter animals, including poultry, do not belong to fixed assets, but are regarded as inventories | Mainly corresponds to subsection 17 0000000 "Livestock, productive and breeding" |

| 520 "Cultivated resources of plant origin, repeatedly producing products" | This includes all types of cultivated perennial plantations that repeatedly produce products, including rare plants whose natural growth and restoration are under the direct control, responsibility and management of specific legal entities, regardless of the age of these plantations. Trees that are grown for wood and produce finished products only once after harvesting are not fixed assets, like crops or vegetables that produce only a single crop | Mainly corresponds to subsection 18 0000000 “Perennial plantings” | |

| 600 “Costs of transfer of ownership of non-produced assets” | This group includes expenses associated with the transfer of ownership of non-produced assets, the value of which relates to the assets produced, but cannot be included in the value of other assets produced. Therefore, these costs should be considered as a separate category of fixed assets | Compliance with current OKOF not established | |

| 700 "Objects of intellectual property" | This grouping includes intellectual products that are the result of mental, intellectual, spiritual activity, research, development, innovation, mineral exploration and evaluation of mineral reserves, allowing to achieve knowledge that developers can sell or use for their own benefit in production, since the use of this knowledge is limited through legal or other protection | Corresponds to section 20 0000000 “Intangible fixed assets” | |

Transition to the new OKOF

In order to make the transition to the new OKOF more correct and quick, from 2017 Rosstandart issued Order No. 458 of April 21, 2016, which approved the transition keys between the editions of OK 013‑94 and OK 013‑2014 of the All-Russian Classifier of Fixed Assets. This document presents both a direct transition key that provides for the transition from the current OKOF (OK 013‑94) to the new OKOF (OK 013‑2014) (Volume 1), and a reverse transition key, respectively, from the new to the current OKOF (Volume 2) .Both keys are presented in the form of tables in which, for comparison, the codes and names of the positions of the current and new OKOF are given.

In direct transition key each position of OKOF OK 013‑94 is set to correspond to one or more positions of OKOF OK 013‑2014, for example:

| OKOF OK 013‑94 | OKOF OK 013‑2014 | ||

| The code | Item Name | The code | Item Name |

| 11 4528801 | Club (except rural) | 210.00.12.10.560 | Club buildings |

| 11 4528802 | Club rural | 210.00.12.10.560 | Club buildings |

| 11 4528812 | House of Culture Rural | 210.00.12.10.580 | Buildings of houses of culture |

| 11 4528813 | House of Culture District | 210.00.12.10.580 | Buildings of houses of culture |

| 11 4528814 | City Culture House | 210.00.12.10.580 | Buildings of houses of culture |

| 11 4528821 | Planetarium | 210.00.12.10.620 | Planetarium buildings |

| 11 4528841 | Theater | 210.00.12.10.630 | Theater buildings |

For OKOF OK 013‑94 items, the names of which contain specific types of fixed assets that are not in OKOF OK 013‑2014, compliance is established in OKOF OK 013‑2014 (SNA 2008) based on the scope of concepts of the corresponding positions.

For positions of OKOF OK 013‑94, which, in accordance with the definition of fixed assets given in OKOF OK 013‑2014, are not fixed assets, in the column “Name of position”, the entry “Are not fixed assets” is made. This means that compliance with such positions is not established, for example:

| OKOF OK 013‑94 | OKOF OK 013‑2014 | ||

| The code | Item Name | The code | Item Name |

| 16 3696600 | Theatrical scenery, designs and props | ||

| 16 3696601 | Stage clothes | Are not fixed assets | |

| 16 3696602 | Stage machines | Are not fixed assets | |

| 16 3696603 | Soft scenery | Are not fixed assets | |

| 16 3696604 | Volumetric scenery | Are not fixed assets | |

| 16 3696605 | Stage props | Are not fixed assets | |

| 16 3696606 | Stage draperies | Are not fixed assets | |

| OKOF OK 013‑2014 | OKOF OK 013‑94 | ||

| The code | Item Name | The code | Item Name |

| 740.00.10.13 | Phonograms | 19 0001023 | Phonodocuments (sound recordings) |

| 740.00.10.08 | 19 0001020 | Film and photo documents | |

| 19 0001021 | Cinema materials and documents in the form of video | ||

| 19 0001022 | Photo documents | ||

| 19 0001024 | Rare and unique film and photo documents | ||

| 23 0001060 | Photographic works and works obtained by methods similar to photography | ||

If the OKOF OK 013‑2014 items cannot be established in OKOF OK 013‑94, then for OKOF OK 013‑94 in the column “Name of the position” the entry “Compliance is not established” is made, for example:

| OKOF OK 013‑2014 | OKOF OK 013‑94 | ||

| The code | Item Name | The code | Item Name |

| 330.28.23.12 | Electronic calculators and devices for recording, copying and outputting data with the functions of pocket calculators | ||

| 330.28.23.12.110 | Electronic calculators | No match | |

| 330.28.23.12.120 | Pocket-sized devices for recording, copying and outputting data with functions of counting devices | No match | |

It should be noted that both forward and reverse transition keys are for reference.

To advise interested parties on the transition to the new edition of OKOF OK 013‑2014 (SNA 2008), a hotline was opened in Rosstandart by calling (499) 236‑24‑39, 236‑73‑70, as well as in the Department of All-Russian Classifiers of Technical and Economic Federal State Unitary Enterprise “Standardinform” Rosstandart by phone (495) 531‑26‑19 (http://www.gost.ru/).

Starting from 2017, state (municipal) institutions will use the new OK 013‑2014 classifier instead of the current OKOF. With the introduction of this document, the structure of OKOF codes assigned to fixed assets will change from 9-digit to 12-digit. The big difficulty lies in the fact that the new codes are not associated with the numbers of accounts in which fixed assets are recorded in accordance with Instruction No. 157n.

In addition, the groups of fixed assets in OKOF will significantly differ. In particular, if now production and household equipment, machinery and equipment, other tangible fixed assets are separate groups, then from 2017 they will be merged into one.

In general, if we compare both classifiers, then moving to a new OKOF, according to the author, will be difficult given the fact that many fixed assets that are now in one group will need to be assigned to a completely different one (with a different name, designation). Also, individual property objects included in the current OKOF will not be fixed assets from 2017.

To help organizations transition to the new OKOF, Rosstandart prepared direct and reverse transition keys; In addition, a hotline has been opened to advise stakeholders.

Instructions for the application of the Unified Chart of Accounts for state authorities (state bodies), local governments, governing bodies of state extra-budgetary funds, state academies of sciences, state (municipal) institutions, approved. By the order of the Ministry of Finance of the Russian Federation dated 01.12.2010 No. 157n.

In 2017, the new All-Russian Classifier of Fixed Assets OK 013-2014 (SNA 2008) comes into force.

From 01.01.2017 the All-Russian Classifier of Fixed Assets OK 013-94 approved by Decree of the State Standard of Russia dated 12/26/1994 No. 359 is canceled and the All-Russian Classifier of Fixed Assets OK 013-2014 (SNA 2008), adopted and enforced by the Order of Rosstandart, is introduced dated 12.12.2014 No. 2018-st (hereinafter referred to as the new OKOF). By the order of Rosstandart dated 04.21.2016 No. 458, direct and reverse transition keys between the editions of OK 013-94 (hereinafter referred to as the old OKOF) and OK 013-2014 (SNA 2008) of the All-Russian Classifier of Fixed Assets are approved.

Decree of the Government of the Russian Federation of 07.07.2016 No. 640 made corresponding changes to the Decree of the Government of the Russian Federation of 01.01.2002 No. 1 "On the Classification of Fixed Assets Included in Depreciation Groups".

According to OK 013-2014, OKOF is used for budgetary (accounting) accounting by public sector organizations in cases provided for by federal standards, unless otherwise specified by authorized bodies of state regulation of accounting. The use of OKOF for the classification of fixed assets is established by the Instructions for the application of the Unified Chart of Accounts of Accounting, approved by order of the Ministry of Finance of Russia dated 01.12.2010 No. 157н.

In this regard, starting from versions 1.0.42 of edition 1 (BSU1) and 2.0.47 of edition 2 (BSU2), respectively, in the delivery of “1C: Accounting of state institution 8” the file of the classifier of fixed assets okof.xml.

File okof.xml contains both classifiers - OK 013-94 and OK 013-2014. In this case, the codes OK 013-2014 established compliance with depreciation groups in accordance with Decree of the Government of the Russian Federation of 07.07.2016 No. 640. After downloading it in the directory " OKOF»Both classifiers will be available.

From 01/01/2017 it is supposed to include only OK 013-2014 in the delivery (okof.xml file).

According to the explanations of the methodologists of the Department of Budget Methodology of the Ministry of Finance of Russia (Letter of the Ministry of Finance of Russia dated December 27, 2016 N 02-07-08_78243), depreciation groups and useful lives do not change due to changes in the OKOF due to changes in the OKOF. New depreciation groups are used for fixed assets acquired from 01.01.2017: “Grouping of fixed assets accepted for accounting (budget) accounting from January 1, 2017 should be carried out in accordance with the grouping provided by the All-Russian Classifier of Fixed Assets OKOF OK 013-2014 ( SNA)) and the useful lives determined by the provisions of Decree of the Government of the Russian Federation of January 1, 2002 N 1 "On the classification of fixed assets included in depreciation groups" (as amended I am of the Russian Federation from July 7, 2016 N 640). "

A similar position with the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia (letter of the Ministry of Finance of Russia dated 08.11.2016 No. 03-03-РЗ / 65124):

“A taxpayer shall have the right to increase the useful life of an item of fixed assets after the date of its commissioning if, after reconstruction, modernization or technical re-equipment of such an object, the useful life has increased. In this case, the increase in the useful life of fixed assets can be carried out within the terms established for the depreciation group in which such fixed asset was previously included.

Other cases of changes in useful lives fixed assets previously put into operation (transfer from one depreciation group to another), code provisions not provided.

Considering the above, in respect of fixed assets put into operation after 01/01/2017, the Classification of fixed assets should be applied to determine the useful life as amended by the Decree of the Government of the Russian Federation of 07.07.2016 No. 640.

In respect of fixed assets put into operation before 01/01/2017, the useful life determined by the taxpayer when putting them into operation is applied. ”

To replace the OKOF codes in the directory " Fixed assets"Processing is applied" OKOF replacement assistant».

Attention!The operation of replacing OKOF codes in the Fixed Assets directory is irreversible, the conversion to the “opposite direction” is not provided!

Before transcoding, save an archive copy of the infobase.

The grouping of fixed assets in the new OKOF differs from OK 013-94.

Statistical reporting for 2016 form No. 11 (short) “Information on the availability and movement of fixed assets (funds) of non-profit organizations”, approved. by order of the Federal State Statistics Service of June 15, 2016 No. 289, compiled according to the old OKOF (OK 013-94).

OKOF codes should not be replaced in the “ Fixed assets»Before reporting for 2016 (the deadline for submitting form No. 11 (short) is April 1).

Download new OKOF (OK 013-2014)

To download the new OKOF, you should open the directory " All-Russian Classifier of Fixed Assets»

- BSU1 - menu "OS, NMA, NPA - OKOF" of the main menu, the "Full" interface;

- BSU 2 - the section "Normative and reference information", the command bar navigation "All-Russian Classifier of Fixed Assets"), or in the section " Administration"By the command" Support and Service"Go to the section" Other classifiers"And open the hyperlink" ".

The new OKOF can be loaded into the directory by pressing the " Download Classifier"On the list form.

The “ OKOF Downloads »in which to select the file okof.xml.File okof.xmllocated in the "StateAccounting" configuration template directory. Having specified the path to the file, click the " Download data».

The process of loading the classifier will begin. At the end of the download, click the " Close". There will be 2 classifiers in the directory:

Indication of new OKOF codes for objects accepted for accounting from 01.01.2017

After loading the new OKOF in the documents on acceptance of the OS for accounting, to indicate the code object according to OKOF, you should first select the appropriate classifier.

When specifying a code for OKOF depreciation group and useful life, in months automatically filled if for the specified value of the attribute OKOF Code only one depreciation group is provided.

When specifying the code for the new OKOF, the Depreciation Group and useful lives are indicated in accordance with Resolution of the Government of the Russian Federation dated 01.01.2002 No. 1 "On Classification of Fixed Assets Included in Depreciation Groups" as amended by Resolution of the Government of the Russian Federation dated 07.07.2016 No. 640.

Replacement of OKOF codes for fixed assets accepted before 01.01.2017

To replace the codes for OKOF in the directory " Fixed assets"Processing is applied" OKOF replacement assistant » (BSU1 - menu "Service - Utilities" of the main menu, the interface "Full"; BSU2 - section "Administration", the action panel command "OKOF Replacement Assistant"), then - Assistant.

In the Assistant form, specify the organizationwhose fixed assets are to be transcoded.

With a large range of fixed assets (more than 10,000), the list of processed objects can be limited by specifying the appropriate group of the directory “ Fixed assets».

When you click " Fill" in the table Helper codes (and their names) assigned to the OS objects according to the old OKOF and the codes corresponding to them according to the new OKOF will be reflected.

For automatic code assignment according to the new OKOF, the table of transitional keys “Direct transitional key from OKOF OK 013-94 to OKOF OK 013-2014 (SNA 2008)” is used, approved by the order of Rosstandart dated 04.21.2016 No. 458.

Automatically a new code is determined only if the code (grouping) is unambiguously in OKOF OK 013-94 and OKOF OK 013-2014.

The new code may not be automatically determined for the following reasons:

- If the position in OK 013-94 according to OK 013-2014 is not fixed assets (for example, 16 1722110 Carpet paths according to the new OKOF are not fixed assets).

- If for grouping by OKOF OK 013-94 there is no unambiguous correspondence in OKOF OK 013-2014, that is, objects assigned to the same code according to OK 013-94 must be assigned different codes according to OK 013-2014 (for example, for position 16 3612371 “ Work tables "in the table of transition keys says:" In accordance with the definition of fixed assets in OKOF OK 013-2014 (SNA 2008) - choose from 330.31.01.1 ")

In the latter case, for each object from such a grouping, a new OKOF code should be indicated individually.

It should be noted that specific positions from the grouping according to OK 013-94 may relate to another grouping according to OK 013-2014. For example, if OKOF (OK 013-94) did not have an appropriate position for the object, some accountants assigned the code 19 0000000 to the objects. For code 19 0009000 “Other tangible fixed assets not specified in other groupings,” the transition key table says: “Not are fixed assets. ” In this case, for each object from such a group, you should independently determine the codes for the new OKOF and indicate their objects .

To indicate individual codes, objects of the group should select the corresponding line, click the " Customize by Object».

In the opened object-by-object change of OKOF codes, a new OKOF code for each object should be indicated.

For example, for position 16 3612371, according to the transition key table, the new code must be selected from group 330.31.01.1.

In the corresponding line of the object-by-object change of OKOF codes Helper open the directory " OKOF"(Step 1), we select a new classifier OK 013-2014. To quickly find the code 330.31.01.1 in it, turn off the hierarchical viewing of the directory list (step 2) and specify the code 330.31.01.1 in the search (step 3).

We see that the code 330.31.01.1 is a grouping. We select the appropriate code for the OS object (using the “ Select" or double click).

Also, by copying the new code into the transition key table, you can paste it in the corresponding line of the object-by-object change table of OKOF codes Helperhaving previously made the line active, and confirm the entry by pressing the " Enter » (Enter).

A list of objects with installed codes can be printed (button “ List»).

Having specified new codes, press the button “ OK" OBOF change code forms Helper.

If one new code can be applied to the entire group of objects, it can be set directly in the main form of the Helper. This code will be applied to all objects of the group OS.

To transcode, press the “ Replace Codes».

On completion, a corresponding message is issued.

Recoding in several stages is possible. When you restart the Assistant or click the "Fill" button again, only the old OKOF groupings are included in the table, if the objects included in them do not establish compliance with the new OKOF.

If compliance was not configured for all OKOF groupings (OS objects), in the table Helper the corresponding lines will remain.

Match the remaining items and replace the codes.

Reclassification of fixed assets

According to OK 013-2014, OKOF is used for budgetary (accounting) accounting by public sector organizations in cases provided for by federal standards, unless otherwise specified by authorized bodies of state regulation of accounting.

According to paragraph 53 of the Instructions for the application of the Unified Chart of Accounts, approved by order of the Ministry of Finance of Russia dated 01.12.2010 No. 157n, fixed assets are grouped by property groups provided for in paragraph 37 of this Instruction (real estate of an institution, especially valuable movable property of an institution, other movable property institutions, property - leased items) and types of property corresponding to the classification subclauses established by OKOF.

The table shows the general correspondence of the groups of fixed assets in the Unified chart of accounts of accounting and OKOF in the revisions OK 013-94 and OK 013-2014.

|

ESBU Account |

Grouping by OK 013-94 |

Grouping by OK 013-2014 |

|||

|---|---|---|---|---|---|

| number | name | the code | name | the code | name |

| 101 02 | Non-residential premises | 11 0000000 | building (except residential) | 210.00.00.00.000 | building (except residential) |

| 101 03 | Facilities | 12 0000000 | facilities | 220.00.00.00.000 | facilities |

| 101 01 | Residential premises | 13 0000000 | dwellings | 100.00.00.00 | residential buildings and premises |

| 101 04 | Cars and equipment | 14 0000000 | cars and equipment | 320.00.00.00.000

330.00.00.00.000 | informational, computer and television communication (ikt) equipment Other machines and |

| 101 05 | Transport facilities | 15 0000000 | facilities transport | 310.00.00.00.000 | facilities transport |

| 101 06 | Industrial and economic inventory | 16 0000000 | inventory industrial and economic | 330.00.00.00.000 | other cars and equipment, including economic inventory and other objects |

| 101 07 | Library fund | 19 0001000 | library funds bodies of scientific technical information archives, museums and similar institutions | ||

| 101 08 | Other basic facilities | 19 0009010 | capital costs for land improvement (reclamation, drainage irrigation and other works | 230.00.00.00 | expenses for land improvement |

| 101 08 | Other basic facilities | 17 0000000

19 0000000 | livestock productive and tribal (except young animals and cattle for slaughter) Planting Material core | 510.00.00.00.000

520.00.00.00 | cultivated animal resources origin repeatedly giving production Cultivated resources |

| 400.00.00.00 | weapon systems | ||||

Due to the inconsistencies of the groups in the old and new OKOF, questions arise:

Based on the new OKOF code, will it be necessary to “transfer” an object accepted for accounting (budget) accounting as part of fixed assets until January 1, 2017, to another analytical accounting account?

If the corresponding position in OK 013-94 according to OK 013-2014 is not fixed assets, is it necessary to write off the object from the composition of fixed assets and take it into account as part of material reserves? What records to make a transfer?

Answers to these and similar questions are given in the letter of the Ministry of Finance of Russia dated 12.27.2016 N 02-07-08_78243:

Assets of fixed assets accepted for accounting (budget) accounting as part of fixed assets before January 1, 2017 are subject to reflection in accounting (budget) accounting in accordance with Instruction 157n with grouping in accordance with OK 013-94 and useful life of these objects, established taking into account the provisions Decree of the Government of the Russian Federation of January 1, 2002 N 1 "On the classification of fixed assets included in depreciation groups" (as amended until 01.01.2017).

If there are no positions in the new OKOF OK 013-2014 codes (SNA 2008) for accounting objects that were previously included in groups of material assets, which are fixed assets by their criteria, the commission for the receipt and disposal of assets of the accounting entity may make an independent decision on the allocation of these objects to the corresponding group of codes OKOF OK 013-2014 (SNA 2008) and the determination of their useful lives.

With the introduction of the new OKOF OK 013-2014 (SNA 2008) from January 1, 2017, during the transition between fiscal years (inter-reporting period), operations should not be carried out to transfer the balances of fixed assets to new groups, as well as operations to recalculate depreciation.

Thus, for fixed assets accepted for accounting (budget) accounting as part of fixed assets before January 1, 2017, OKOF OK 013-2014 (SNA 2008) is used only for statistical purposes.

As noted above, it is not necessary to replace OKOF codes for fixed assets that were registered before 01.01.2017, before compiling statistical reports for 2016 (the deadline for submitting form No. 11 (short) is April 1), since the classification of all objects The OS for the new OKOF will be required only for compiling statistical reports for 2017. At the same time, we recommend conducting a test conversion to copies bases in order to pre-determine objects for which compliance with the new OKOF will not be automatically found and decide on such objects.