Document recalculation of personal income tax in 1s 8.2. How to reflect the recalculation of tax on personal income (personal income tax) in the configuration? Accrual of personal income tax

Calculation of personal income tax

If the tax agent did not retain the regulated current legislation income tax individuals Since his employee or withheld an amount less than expected, the missing difference must be recovered from the taxpayer.

If an employee continues to work in the enterprise, then after correcting a mistake or changing his status (eg, tax resident) during the next calculation of personal income tax in programs on the platform 1C Enterprise 8 the missing amount will be automatically calculated and withheld.

If non-payment of personal income tax is revealed when it is not possible to withhold tax (for example, after the dismissal of an employee or after the end tax period) then the company will not be able to recover personal income tax. According to paragraph 5 of Article 226 of the Tax Code of the Russian Federation, in this case, the tax agent must notify the taxpayer in writing and tax authority (at the place of registration) about the impossibility of collecting personal income tax and indicating the amount of tax in the form of 2-personal income tax approved by order of the Federal Tax Service of Russia of November 17, 2010 No. MMV-7-3 / [email protected]

For this, it is necessary to form systems in the program 1C Enterprise 8 help 2-personal income tax in paper or in electronic format and send it to the tax authority at the place of registration.

Refund of personal income tax

If for any reason the tax agent has retained a large tax rate with taxpayer income, the difference must be returned. Refund and offset of excessively collected and paid tax amounts is regulated by the Tax Code Russian Federation (Articles 78 and 79). IN new edition Clause 1 of Article 231 of the Tax Code of the Russian Federation, which entered into force on January 1, 2011, specifies the procedure for returning personal income tax to the taxpayer from whom the tax agent withheld tax in excess of the current rate.

If the reason for withholding a larger tax amount is a change in the state of income or deductions, then from the beginning of the current year, the tax agent must notify the taxpayer within 10 days from the day the error is discovered. In this case, you must specify the exact amount that was kept in excess of the established rate. The form of taxpayer notification is not established by applicable law, therefore, it can be arbitrary.

The amount of personal income tax withheld in excess of the established rate is refundable, the basis of which is a written statement by the taxpayer (paragraph 1, article 231 of the Tax Code). That is why it should be indicated in the taxpayer’s notice of excessively withholding tax a warning about the need to write a written application for a refund. The return of personal income tax is possible only in non-cash form. Thus, when drawing up the application, the taxpayer must indicate the details of the personal bank account to which the funds will be transferred.

To process the return of personal income tax in programs 1C Enterprise 8, for example, in 1C ZUP 8 ( 1C: Salary and HR 8) you need to perform actions in the following order:

- enter a document in the database Return personal income tax: Desktop programs 1C: Salary and personnel management;

- go to the tab "Taxes and contributions";

- select the menu "Return personal income tax".

- Make a transfer of funds on the basis of the document.

Note! Responsibility for not informing about tax withheld in excess of tax rate is not provided for by applicable law. An informed employee may reserve the right not to insist on return personal income tax. That is, if the employee continues to work and did not submit an application for the return of personal income tax, then with subsequent calculations of personal income tax in programs, the amount withheld above the rate will be automatically credited.

Good day.

This is not the first time I have encountered such a problem in typical 1C 3.0 configurations when calculating salary. Wherein it is and about 1C Salary and personnel management 3.0, and about 1C Accounting 3.0. In 1C, when calculating wages in the payroll sheet or in the pay slip, the amount “excessively withheld personal income tax” comes out. Where did she come from? Where to see her? How to remove it, even with hands? How to make it no longer appear?

The worst thing is that it affects the amount payable to the employee. In most cases, the amount of excessively withheld personal income tax is equal to the personal income tax accrued in the current month, although there may be inconsistencies.

This article will not discuss when excessively withholding personal income tax does indeed have a place to be, I will talk about the most commonplace case when it appears in the program, but it should not be. In versions 3.0, this error is very easy to achieve and it is not immediately clear what to do about it.

So, today I suggest you deal with this misfortune. I hope many will thank me)) Do not skimp on comments, registration takes 5 seconds, I do not send spam to my visitors

Let's start in order. The first thing I want to tell is methodology for calculating excessively withholding personal income tax and the reasons for its incorrect appearance.

As you know, in personal income tax cards there is such a thing as "Accrued personal income tax" and "Paid personal income tax", in practice they are almost always equal, but in theory they can differ. For example, if the employee has not been paid the accrued. So, since this is possible, then 1C should keep records of such situations and it is maintained. For accounting purposes, the accumulation register " Payments of taxpayers with a personal income tax budget". The accrual documents make the movement" income "in it, and the payroll sheets make the movement" expense ".

In this case, personal income tax is taken into account as is known on an accrual basis. Those. the program analyzes all movements from the beginning of the year at the end of the current month (checked 100% watched requests). Accordingly, if previously paid for the employee was more than accrued (well, you never know), then the employee must pay these amounts on hand. For example, for the whole year 3900 rubles of personal income tax were charged and 4000 rubles were paid, so when calculating the current month, we must pay 100 rubles more to a person’s hands.

Now about the cause of the error: You calculated your salary, verified everything and you liked everything, form a statement of payment, spend it. In our accumulation register “Calculations of taxpayers with a personal income tax budget” there is a receipt made by the document “Payroll” and an expense made by the document “Statement to the bank”. The amounts of income and expense are equal, everything is beautiful. After that, you recalculate the salary for any reason, without having issued a statement. It’s not even necessary to replenish the accruals, just adjust the amount with your hands, personal income tax is recalculated automatically. When calculating the accrual document ignores its own movements, this is correct, but he sees the movements of our statement. As a result, we have paid personal income tax without accrued, expense without income. And this amount falls into " Excessively stunned personal income tax".

Now where to see it: You will most likely see this only in the report, or notice that the statement after overfilling increased the amount of payments. The fact is that by default, 1C Accounting 3.0, that in 1C Salary and Human Resources 3.0 field where this amount is stored is hidden in all documents.

To begin, let's do the following: in the form of an accrual document, click the "all actions" button. We’ll select “Change shape” from the drop-down menu. Then if you have activated the personal income tax data plate in the form, then you will immediately see the “tax to offset tax”. Put a daw in front of him.

Voila, we found the enemy. At least we see him. Praise heaven, if the program ends correctly, this setting will be saved and you won’t have to do it again. Now the enemy is always visible and you can always detect it in advance.

This field is in all accrual documents where personal income tax is calculated immediately. In bookkeeping, this is one document, and in ZUP their handful.

Now how to fix it: it’s not so simple, even in ZUP it is conceived that the personal income tax is considered by itself and its manual adjustment is not convenient. You can poke twice in the amount, but before you allow it to be corrected, the program will verify whether you have a good mind by asking a stupid question. And so on each line. not only will she ask, she will mark the corrected lines as manually edited (highlighted in bold), which can affect auto recalculation when editing charges. but 1C didn’t leave us any other way.

Now how to prevent this?: it’s very simple (probably) to spread out the statements before editing the charges.

In small offices, this is enough, but in large ones, where I consider several people to pay, this is not suitable at the same time. Usually I use a simple processing that analyzes the presence of “Excessively withholding personal income tax”, finds the documents that formed it, corrects the tabular part of the accrual document “Personal income tax”, resets the amounts in the column “ tax deductible "and redirects the document. The plus is that it does not set the manual adjustment flag in the lines. No need to poke into every line of the document. She will not miss a single document.

It’s easy to use the processing, it has a “only report” checkbox and period selection fields. When the "only inform" checkbox is selected, the processing does nothing, only reports the names of documents, if any. Those. It can also be used as a test.

If you want to embed it in the database, modify it according to the instructions in the article Creating external processing for managed forms. Simply processing, with the possibility of registration in additional reports and processing.

Thank you, see you soon. Write reviews.

Upon receipt of income by an employee, the organization, as a tax agent, is required to calculate personal income tax on employee taxable income, withhold it and transfer the amount withheld to the budget (paragraph 1 of Article 226 of the Tax Code of the Russian Federation).

Excessively withheld personal income tax occurs in the following situations:

- Deductions provided retroactively.

- When changing status from non-resident to resident.

- Perform any recalculations. For example, when an employee was calculated s / w for the month, and later it turned out that leave was granted without pay.

Deductions granted retroactively

Let's consider how it is taken into account unnecessarily by the example when the employee wrote a retroactive deduction application. In other cases, proceed in the same way.

For example, an employee submitted an application for a deduction not in January, but in March. The salary for January, February has already been calculated and personal income tax is calculated.

How to register the right to standard tax deduction for personal income tax in 1C ZUP 3.0 (2.5) see in our video:

The first version of the event: when the total amount of personal income tax for the current month is positive

In 1C 8.3 ZUP 3.0here is the calculation of the salary for January 2016: the taxable income will be 16,500 rubles. and the tax on it is 2,145 rubles. A similar calculation will be for February 2016:

In March 2016, an employee wrote an application for a deduction for one child:

When calculating the salary for March 2016, we pay attention to the personal income tax tab. On the Charges tab, the calculation will be the same as in January and February:

First, we see that a deduction of 1,400 rubles was applied. (The applied deductions column is filled). Secondly, in addition to the line for March 2016, lines for the previous months appear. Tax in the amount of -182 rubles. corresponds to the amount of tax that must be recalculated taking into account the deduction, i.e. 1,400 * 13% \u003d 182 rubles. Thus, in March personal income tax will be recalculated and tax amounts for January and February will be taken into account. Paying salary for March, the tax will be deducted taking into account this recalculation:

In 1C 8.2 ZUP 2.5 the calculation will be similar. The only difference is how the deduction information is entered.

In 1C for payroll ed. 2.5 in order to assign deductions to an employee, you must open an individual’s card (Desktop - Personnel records - See also - Individuals or go from an employee’s card using the link “More information about an individual ..”), execute the “Personal Income Tax” command in top command bar:

In the Data entry for personal income tax window, enter information on deductions:

When calculating the salary for March 2016, we also see the recalculation of personal income tax for January and February 2016:

We pay salary for March, draw up a document and see the register of personal income tax payments with the budget. In this register with the type of movement “Consumption” (“minus”), personal income tax withheld is recorded:

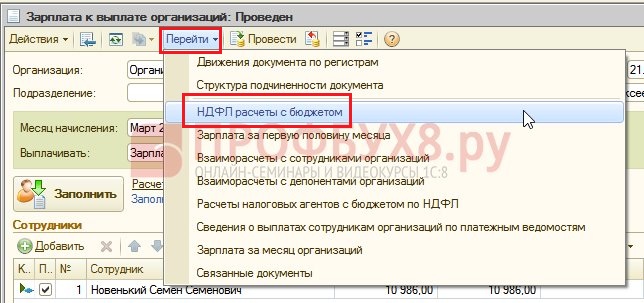

You can view the records that turned out in the personal income tax register of calculations with the budget by clicking in open document Salary to pay organizations button Go to - PIT calculations with the budget:

The second version of the event: when the total amount of personal income tax for the current month is negative

In the examples under consideration, the tax amount for March 2016 was enough so that in the aggregate for three months the tax amount would be positive. But there are situations when the tax amount for the current month may not be enough and the tax will turn out to be negative.

IN ZUP 3.0 for example, the employee A. Sokorina worked in March only one day, the rest of the time she took a vacation without saving the salary.

Then, when calculating the salary for March 2016, she will have the following calculation:

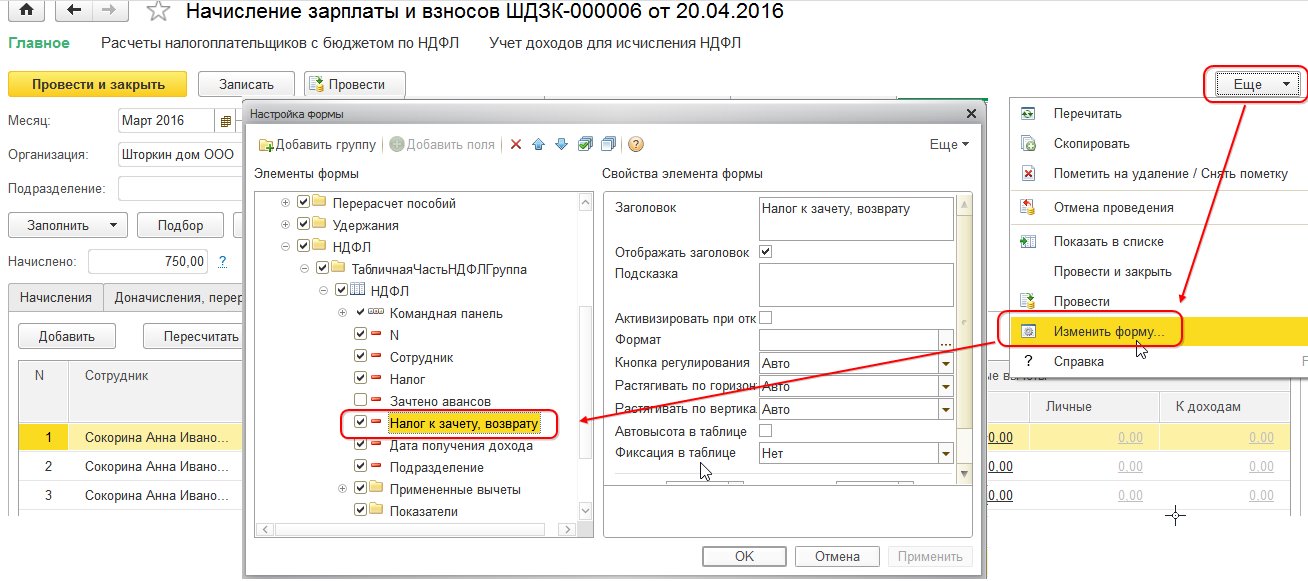

Taxable income will be 750 rubles. Personal income tax on this amount - 98 rubles. But since the deduction is due to the employee, it will not be applied in its entirety, but only for 98 rubles. The remaining amount is 182 - 98 \u003d 84 rubles. will set off the next billing month. The amounts for January and February will also be set off next month. Such amounts that cannot be taken into account in the current calculation appear in the Tax to offset, refund column.

If this column is not visible in 1C ZUP 8.3, then you can enable its display using the More button - Change form. This column must always be monitored, since it keeps records of excessively withholding personal income tax. Program 1C 8.3 ZUP 3.0 keeps a record of such amounts separately and does not offer them for payment:

We will pay salary for March and see that the amount payable has not been increased by the amount of excessively withheld tax and is equal to 750 rubles:

We will form a settlement sheet for March. The amount of excessively withheld tax is accounted for as debt to the company at the end of the month:

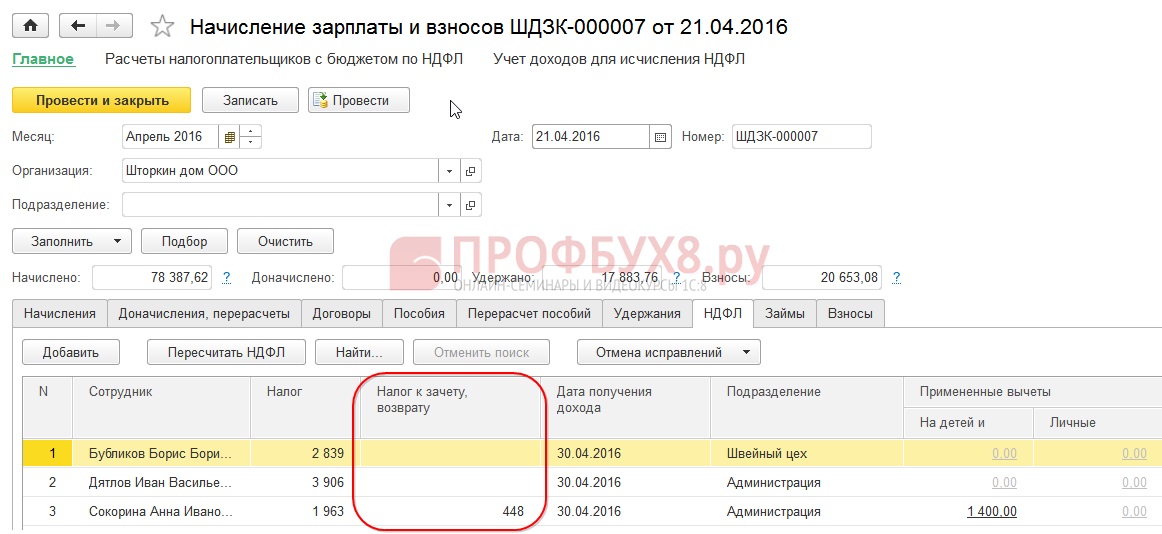

Let's see the salary set for March 2016, we will be interested in the personal income tax line:

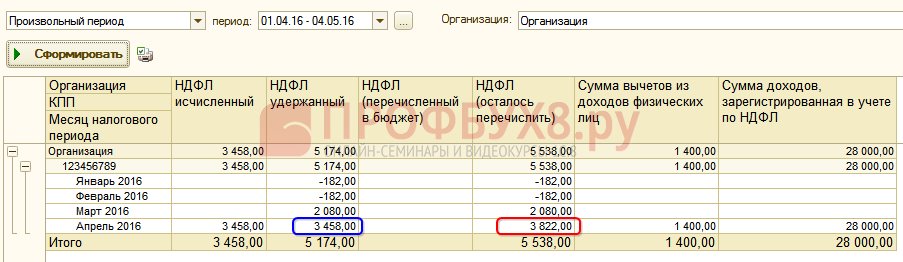

As we see in the total amount of personal income tax (6,545 rubles), there is an amount with excessively withheld personal income tax (-448 rubles), which should not affect the tax withheld. According to the law, the amount of personal income tax withheld must be transferred to the budget, and in the code we see the amount of the calculated personal income tax. Thus, the amount to be transferred to the budget for March should be 448 rubles. more than in the vault.

In the statement on the payment of salaries, personal income tax was recorded for transfer in the amount of 6,993 rubles, which is 448 rubles. more than in the vault (6 545 + 448 \u003d 6 993 rubles):

Let's calculate the salary for April 2016 and look at the personal income tax tab:

For employee A. Sokorina, an excessively withheld personal income tax is set off in the amount of 448 rubles. Now the amount in the column Set-off tax, refund stands with a plus sign:

In the payroll for April, debt is an amount that does not include excessively withheld personal income tax. Thus, the amount of 448 rubles. was set off. This information is told to us by the information “Reference”:

Pay employees salary for April 2016:

The amount of personal income tax for the code was 8,708 rubles, and the amount necessary to transfer was 8,260 rubles, which is 448 rubles. smaller. The amount of tax withheld is different from the amount calculated for the credited amount of excessively withheld personal income tax.

If the sum of personal income tax contains negative values \u200b\u200bin the code, then when transferring personal income tax to the budget, these amounts should not be taken into account. Accordingly, the amount in the code and the amount when paying personal income tax will never be equal. Also, if negative amounts are set off next month, the amount in the personal income tax bill will not be equal to the amount for the transfer of personal income tax to the budget.

In addition, the amount of excessively withheld personal income tax can be set off in the calculation of the next month. The employee can write a statement and he will be refunded excessively withheld tax.

Change of status from non-resident to resident

If an excessively withheld personal income tax has arisen as a result of a change of status from a non-resident to a resident, then the tax is not refundable, but can only be offset in the calculation next months. If at the end of the tax period not all of the amount is credited, then the organization submits information about excessively withheld personal income tax to the tax and the tax itself returns this amount to the employee after his appeal.

Excessively withholding personal income tax - what to do?

We will learn how to return excessively withheld personal income tax in the program 1C 8.3 (8.2) for personnel.

How to return excessively withheld personal income tax in 1C ZUP 8.3 (rev.3.0)

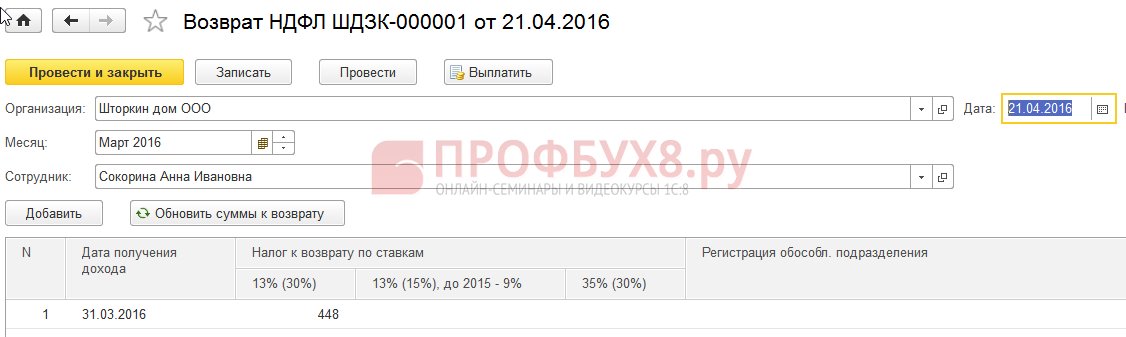

- We draw up a document for tax refund: section Taxes and contributions - Return of personal income tax:

- A document for the payment of salary, in which we already see that the amount is paid in the amount of 1,198 rubles (750 rubles (salary) + 448 rubles (returned by personal income tax):

In the pay slip we see that the amount of excessively withheld personal income tax was formed and in the same month it was offset, that is, returned and paid together in the salary for March 2016:

In case of return of personal income tax, you must manually make an entry in the Calculation of tax agents register with the personal income tax budget for the correct display of information on personal income tax for transfer. To do this, create the Data Migration document. We choose in the setup of the composition of the registers - the accumulation register. Calculations of tax agents with a personal income tax budget. Fill it as an “expense” with the amount of “-448.00 ″:

Thus, we adjusted the information on the transferred personal income tax to the budget for the amount of the return.

For possible errors when holding personal income tax in 1C ZUP 3.0, see our video tutorial:

How to return excessively withheld personal income tax in 1C ZUP 8.2 (rev.2.5)

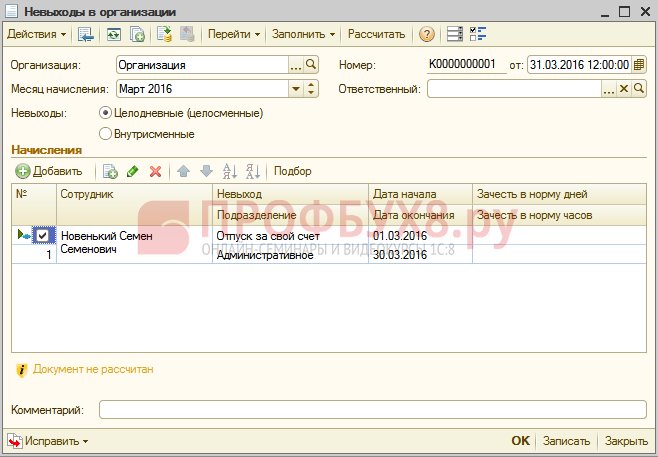

Suppose an employee takes a vacation without saving from 03/01/16 to 03/30/16.

Thus, in March, he worked only 1 day:

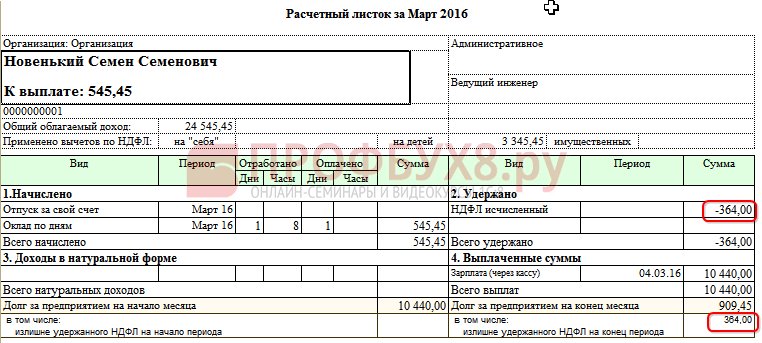

We calculate his salary for March 2016 and see that the amount of personal income tax with a minus sign has formed, that is, excessively withheld personal income tax has arisen:

This amount does not increase the amount payable and is stored in a separate personal income tax register for offset. You can see it by clicking on the Go button in the posted document Payroll:

If excessively withholding personal income tax arises, a record with a “+” sign is placed in the register. In the payroll for March, the debt at the end of the month is 909.45 rubles, of which 364.00 rubles are the amount of excessively withheld personal income tax:

The amount of excessively withheld personal income tax should not increase the amount payable. As we see, having generated a document for the payment of salaries for March 2016, the amount payable is 545.45 \u003d 909.45 -364.00 rubles:

When a payment document is posted, a zero amount of tax withheld is recorded, and thus a difference arises between the calculated and withheld personal income tax. We can see the calculated tax in the salary code or in the payroll of employees:

In the arch for March 2016 in the amount of personal income tax calculated 1,716.00 rubles. there is a negative amount of tax. You need to transfer to the budget the amount withheld, that is, for March 2016. should be transferred to the amount of 364 rubles. more than we see in the arch.

See the amount that should be transferred for March 2016. it is possible in the report Analysis of accrued taxes and contributions on the date when the salary for March was paid. In our example, it is 04/05/2016. In the NDFL column withheld, the amount to be transferred to the budget will be indicated:

There are two possible scenarios for working with such personal income tax:

- either read out in the following months;

- or return it at the request of the employee.

The amount of excessively withheld personal income tax is counted in the following months

We calculate the salary for April 2016. For the employee, S.N. taxable income is 12,000 rubles. - 1,400 rubles. (deduction) \u003d 10 600 rub. Personal income tax on this income 10,600 * 13% \u003d 1,378 rubles. - this is visible on the personal income tax tab:

When conducting this document, an entry is made in the personal income tax accumulation register for offset, but already with the “-“ sign, that is, the amount that was previously recorded in this register with the “+” sign in March 2016, this document was written off:

Upon payment of a salary for April, the amount “To be paid” will be more by 364 rubles:

We will formulate the PIT analysis report on the payroll date for April 2016 (as of 05/04/2016) and see how much you need to transfer to personal income tax budget for April 2016. And as you can see from the report, this amount is 3,094.00 rubles. less than the amount of the set 3 458.00 rubles. at 364.00 rub:

If an employee wrote an application for personal income tax return

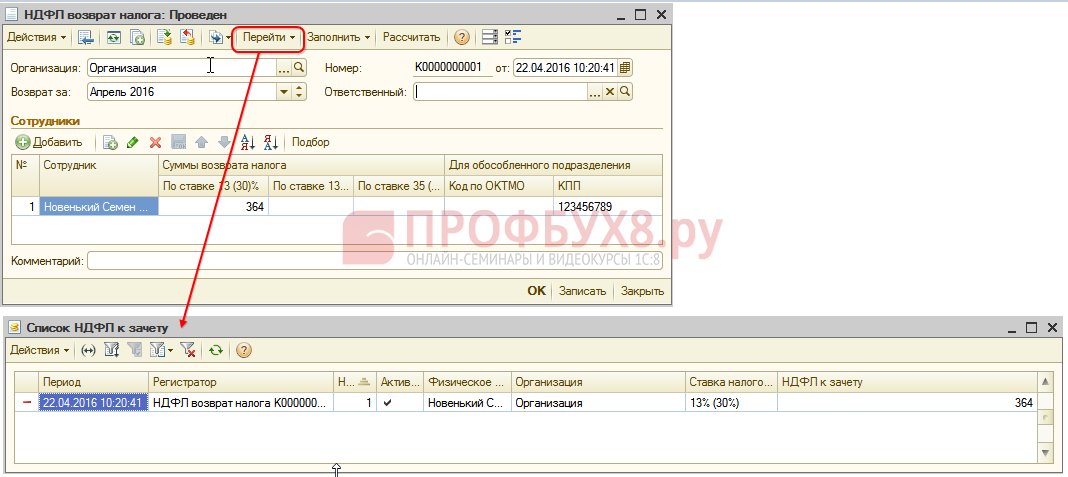

We create a document for the return of personal income tax: Desktop - Taxes - Return of personal income tax. During this document, entries are made to the registers.

In the personal income tax register for offset in the amount of equal amount tax refund with a “-“ sign. Thus, excessively withheld tax is considered to be written off:

In the register Salary for a month of organizations, fixes the amount that will be paid to the employee:

In the personal income tax register calculations with the budget, forms an entry with the “-“ sign, which reduces the amount of tax withheld by 364 rubles:

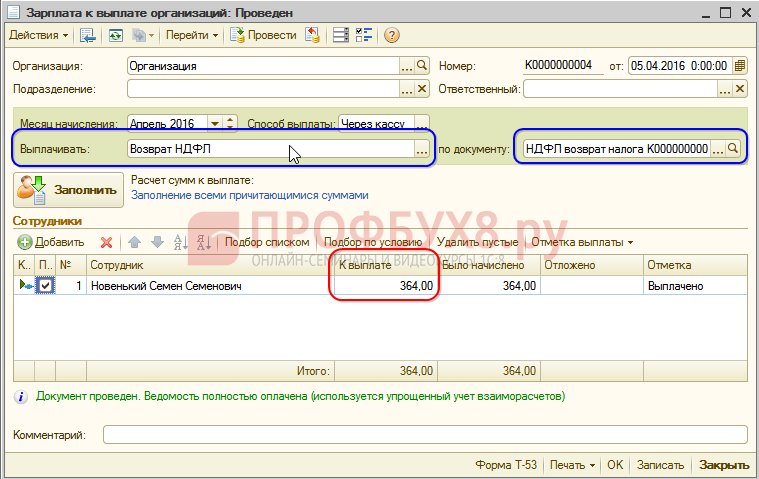

We pay the registered personal income tax return:

When a document is recorded in the NDFL register for offset, the amount of the calculated tax when calculating the salary for April 2016 will already be different, since the amount was debited earlier by the NDFL Refund document:

Forming a payment for April 2016, the amount paid is 364 rubles. less than in the previous example:

We return to the report Analysis of assessed taxes and contributions and form it on the date of payment. The amount of tax withheld to be transferred to the budget has not changed compared to the previous example:

In ZUP 2.5, as well as in ZUP 3.0, when the personal income tax is returned, the amount of the personal income tax transferred in the Calculation of tax agents register does not decrease with the personal income tax budget, so you have to manually adjust this amount.

The discrepancy in the amount of personal income tax and personal income tax withheld for transfer can be seen if you generate a report Analysis of assessed taxes and contributions for the period from April to the date of payment of salary:

In order to adjust the amount for transfer, we use the document Data Transfer. We create an entry in the accumulation register. Calculations of tax agents with a personal income tax budget with the type of income movement for the amount of personal income tax returned with a minus sign, thereby reducing the amount to be transferred:

Once again we form a report with the same parameters and see that the amount of personal income tax withheld began to equal the amount of personal income tax for transfer:

Summarize. If, for some reason, excessively withheld personal income tax appears in your calculation, now you know how to return excessively withholding personal income tax for its correct accounting in 1C programs.

The moment of registration of withheld personal income tax in 1C ZUP 2.5 depends on the flag “When personal income tax accept the calculated tax as deductible. ” Each option, depending on whether the box is checked or not, has its own nuances that require increased attention. See more about this in our video:

In order to bring to you all the most relevant information on the formation of the 6-NDFL form, to understand all the intricacies and nuances of filling out the calculation in 1C, the Profbuh8 team ( 1

ratings, average: 5,00

out of 5)

These materials are available.

to view only registered

subscribers of the project Profbuh8.ru

Today I will review step by step instructions for accounting of personal income tax (abbreviated PIT) in 8.3 (version 3.0).

As probably everyone knows, the main tax that is withheld from our salaries is personal income tax. The remaining deductions are mainly paid by the employer (for example, these are deductions in pension Fund and fund health insurance. They are also called “insurance premiums”).

In 2017, the personal income tax rate is still 13% of total amount accruals minus deductions.

Deductions may be different. One of the most standard and common deductions is a deduction on minor child. For the first and second child in 2015, the amount of the deduction is 1,400 rubles, for the third and disabled child 3,000 rubles.

Deductions for adult students and other deductions are also applied, which we will not consider in this article, it is devoted to another topic.

How are deductions applied? Very simple. They are deducted from tax base before the personal income tax is calculated and withheld.

For example:

The salary of an employee is 40,000 rubles. From this amount, he must pay tax. But if he has a minor child, then we must apply a deduction! And the tax will be taken already from the amount of 40,000 - 1,400 \u003d 38 600 rubles. Total to be paid to the employee (if he has no other deductions or obligations) 38 600 - 13% \u003d 33 582 ruble. Personal income tax leave 5 018 rubles.

So, approximately we figured out how personal income tax is calculated. Now let's see how operations are reflected personal income tax accounting in 1s 8.3, and check for example the amount to be withheld.

Retention of personal income tax in 1C ZUP 8.3

PIT is withheld from almost all personal incomes. This is directly a salary, vacation pay, material assistance, and so on.

Consider the step-by-step instructions on withholding personal income tax on the example of a payroll document in the program 1C ZUP 3.0.

Get 267 1C video lessons for free:

We go to the “Salary” menu, then click on the link in the ““. In the window of the list form, click the "Create" button and select "Payroll and Contributions." A window for entering data will open. Be sure to specify the month of calculation and the organization in which employees work. Naturally, the mandatory data are also the employees for whom the accrual takes place.

You can select employees one by one using the "Add" button, or you can use the "Fill" button. In this case, the tabular part of the document will be filled automatically by the employees of the selected organization. I’ll use this button. Organizations and employees are already listed in the demo database.

That's what I did:

We’ll go to the “PIT” tab and see if the program calculated it correctly for us and whether it calculated at all:

Check the retention calculation. Unfortunately, none of the employees are in the demo database. standard deductions at least for a child. But let’s leave it as it is, it will be easier for us to check the calculation, and, in addition, I have already described the deductions in previous articles. Believe me, they are all taken into account in the calculation correctly.

So what do we have? Salary of the employee Simutina Elena Frantsevna 55 000 rubles and personal income tax rate of 13%. There are no deductions. We will calculate 55,000 - 13% \u003d 7,150 rubles. The program counted correctly.

When the document is held, tax withholding will occur, that is, personal income tax data will go to the register tax accounting 1C 8.3. This deduction we will see in the statement to the cash register for. In the same statement, we indicate whether we have listed the tax or will do so later.

Transfer of personal income tax to the budget

To complete the transfer of personal income tax to the budget in 1C ZUP 8.3, you need to go to the "Payments" menu, click in the "See. also "link" PIT transfers to the budget ".

Press the “Create” button and first create the “Cash Register”:

The collection of tax on personal income is determined by the requirements of Art. 231 Tax code. Often, if you need to change the percentage or amount, questions arise, so we will answer here the main ones and talk about how to spend recalculation of personal income tax in 1C ZUP.

There are three main points you might need to spend in 1C ZUP 3 recalculation of personal income tax. We will tell you more about each of them.

Additional tax charge

The moment when the personal income tax is incorrectly calculated may occur in the following cases:

- common mistake related to extra deductions or an incorrectly indicated expense code;

- recalculation of wages for the previous period and increase in tax, respectively;

- an individual has lost the resident status regarding payment of taxes.

Recalculation of personal income tax in 1C 8.2 ZUP is made on the basis of familiarization of the employee with a certificate 2-NDFL.

Return excessively withdrawn personal income tax back

The reasons may be exactly the same as in the previous case. The message that the tax will be recalculated is sent to an individual by mail or transmitted in person. There is virtually no liability tax agent for the fact that there was no information regarding changes in the tax rate.

In order to refund excessively accrued tax, that is, to recalculate personal income tax in 1C 8.3 ZUP, you need to carry out the document created in the tab "Taxes and contributions":

After you have created such a document, you need to transfer the necessary amount money: Action - Based - Salary payable.

Often the tax deduction is due to the fact that the employee did not provide the data on the birth of his third child on time. In this case, you can use such an internal tool as the Assistant for editing the deduction for children, which is preinstalled in each licensed version of 1C.

We are sure that problems with conducting such operations in 1C should not arise. Unified forms and convenient help will help to cope even with the most difficult case.