The month does not close at 1s 8.3. How to close a quarter for a beginner accountant step by step instructions

How to force the closing of the month not to swear for past periods in 1C: Accounting 8.3 (version 3.0)

2018-11-02T12:29:21+00:00We are all familiar with such a wonderful routine operation as "Closing the month" in 1C: Accounting 8.3 (version 3.0).

And we have all been in a situation where you need to close the period, and the program starts to require you to rerun and close the previous period.

You start to close the previous period, and she again requires you to rerun the early periods.

And so on ad infinitum. If you rewire the old periods - the numbers are creeping, and the reporting has already been submitted. And the year is closed. This is a real nightmare for an accountant. What to do?

Making a backup

First of all, before closing the period - I strongly recommend make a backup bases. This will allow us to boldly resend the documents, knowing that in which case we can always return to the original state. About how to make a backup is written.

Reading mistakes carefully

Next moment. If we are going to do all the closures of the month, say, for 2013, first we need to cancel all the closures of the month for the year, and then sequentially, starting from January 2013, close the month after the closure of the month.

Farther. Carefully read the errors that the program writes. Skip surgery only as a last resort. Usually, it is enough to correctly set the parameters and correctly close the first month of the year, and then everything goes like clockwork. Take the time to deal with these mistakes once and forget about them forever.

But now, suppose we have already closed all the years until 2013 (or we generally transferred all the documents from old edition 2.0 in 1C 8.3) and we need to close 2013 without changing previous years. We begin to carry out the closing of January 2013, and the program swears - they say, repeat the closing of December 2012! Don't give in. Because if you start rewiring the closing of 2012, all the numbers will creep, and the year is already closed.

We deceive the program

In this case, it is correct to make 1C: Accounting 8.3 think that 2012 is closed correctly and nothing needs to be rewired there.

How to do it below in steps.

We clear the register "Irrelevant routine operations"

- Open the "All functions" menu item. About how to do it is written.

- Find the item "Registers of information" in the window that opens. Expand it to the plus.

- In the list of registers, find the item " Irrelevant routine operations"Open it.

- Remove all items from this window. Highlight one by one and press Delete or the delete button on the toolbar.

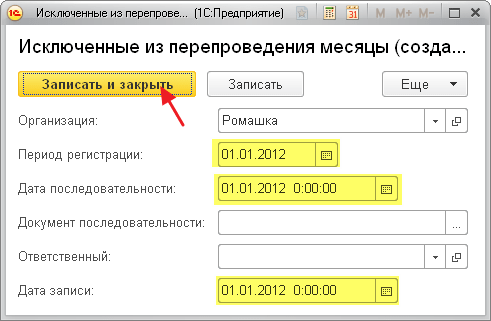

Set up the register "Months excluded from rerunning"

Attention! Newer versions of Enterprise Accounting (since version 3.0.63.20 for sure) no longer use the "Excluded from reposting months" register.

Now, right at the end of the month, you can click on the link "Reposting documents" and select the "Reposting is not required" option.

If the closing of the month still requires the re-posting of documents for the past year, open the "" menu again, find and open the information register in it " Months excluded from replay".

Your task is to create for each month of 2012 (I remind you that we are trying to close 2013, and 1C swears that we need to rewire 2012) a separate entry in this register (using the Create button):

Let's exclude January 2012 from reposting - the entry will be like this:

Click the "Save and close" button.

Then February 2012:

You should now be able to post the month-end closing for January 2013.

What other options are there?

Here I will describe stories from readers that they share when parsing the error of closing the month at home.

A reader from Bryansk writes:

We have been working in 1s 8.3 since 2016, and the company itself since 2013. Now I tried to remove the employment of employees from 2013, accepted them from 12/01/15 (I entered the balances of the salary). AND EVERYTHING WORKED)))) Hurray!

Ivan Vatumsky shares his case:

Users reposted documents in 2015, after which it was necessary to re-close 2015 again.

Then it turned out that in the operation "Closing the month" for the required period, not a single operation is displayed.

It turned out that the reason for this is in the information register "Input dates initial balances", which were installed just on 12/31/2015 and thereby instructed the program not to perform routine closing operations of the month.

Closing the year in 1C 8.2 - the final operation before compiling annual report. The last postings that you make for the year are entries for the reformation of the balance sheet, that is, the closing of the year. This process in 1C 8.2 is automated. The program independently makes the necessary records on the reformation. In this article, you will learn about closing the year in 1s 8.2 with step-by-step instructions.

Read in the article:

When closing the year in 1C 8.2, you need to perform a number of certain procedures. In particular, zero the balance on accounts 90 “Sales” and 91 “Other income and expenses”. After that, you can proceed to the reformation of the balance sheet and accounting for the profit or loss received during the reporting year. These procedures in the program are carried out in 5 steps.

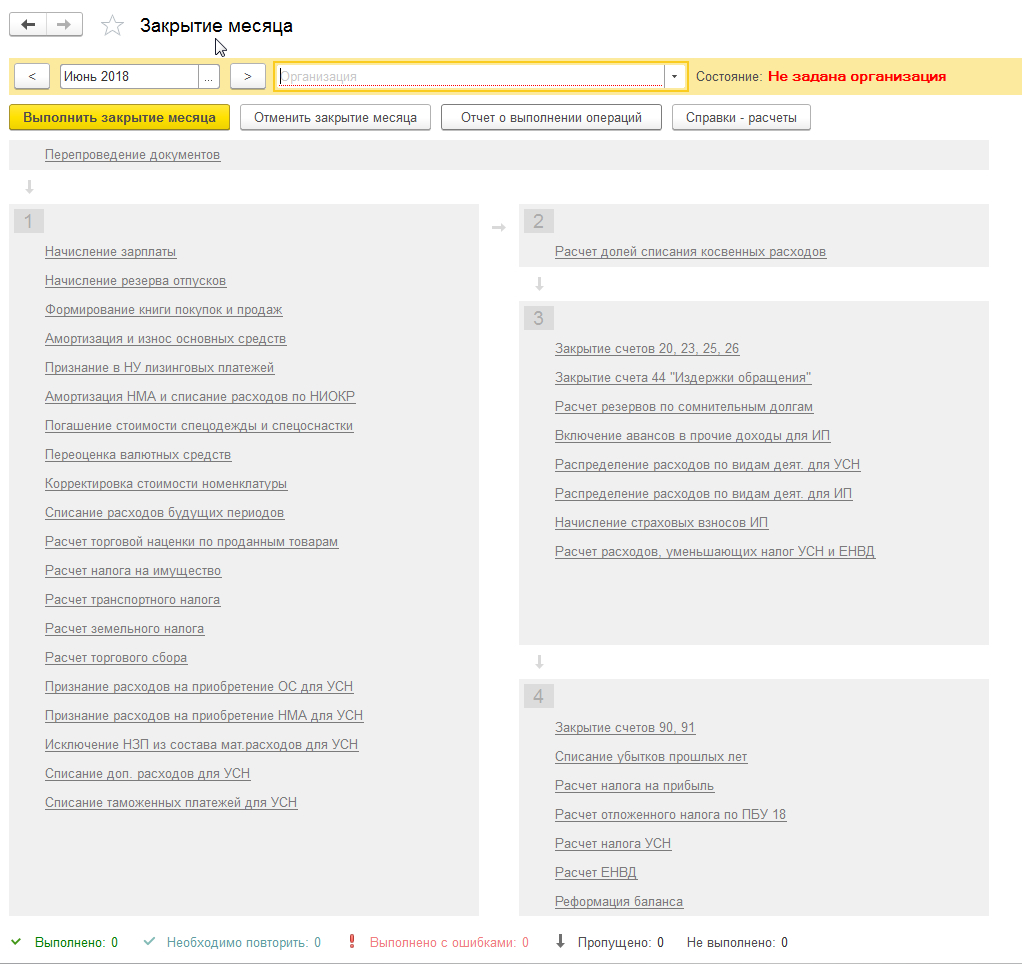

Step 1. Open the Month-End window

Open the section "Operations" (1) and select the link "Closing the month" (2). A special window "Closing the month" will open.

Step 2. Fill in the required fields

In the window that opens, fill in the "Organization" field (3) and indicate the last month of the year to be closed, for example, "December 2018" (4). In order for the closing procedure to be successful, all previous months, from January to November, must also be consecutively closed in a similar manner.

Step 3. Checking documents

To properly close the year in 1C 8.2, you need to take into account all the operations that were recorded in the program during the year based on primary documents. All documents must be included in the program in chronological order. If you have made corrections to documents, then accounting entries they need to be updated. To simplify this procedure in 1C 8.2 there is a special link "Control of the sequence of documents" (5).

- red - the sequence of documents included in the program is violated;

- green - the documents are correctly taken into account in the program.

If the link is red, then in the 1C program according to the documents you need to update accounting records. To do this, click on it. The Check Document Sequence window will open. In the window that opens, click the "Resend Documents" button (6):

After the accounting records for the documents are consistently updated by the 1C program, the link "Control of the sequence of documents" will turn green (7):

Step 4. Complete the closing of the year in 1C 8.2

To complete the operation to close the year, click "Close the month" (8).

1C 8.2 will independently create all the operations that are needed to close December and the year as a whole. Their list is in sections 1 - 4 of the "Closing the month" window. For example, it will write off the balances on accounts 20, 23, 25, 26 and 44, and also make the necessary postings on accounts 90 and 91. As a result, all operations in this window will be colored green. The closing of the year in 1C 8.2 is completed. The Month End window will look like this:

Step 5. Check the closing of the year in 1C 8.2 according to the balance sheet

The balance sheet reform provides for the closure of all sub-accounts to accounts 90, 91, 99. As of December 31, they should not have a debit or credit balance. It is better to check the correctness of closing balance sheets at the end of the year in 1C 8.2 using the balance sheet. At the end of the year, the balance on them should be zero. After closing the year and reforming the balance sheet, the statement may look like this:

Closing at the end of the month in accordance with the order of the Ministry of Finance of the Russian Federation dated 10/31/2000. No. 94n "On the approval of the Chart of Accounts" are subject to accounts 25 and 26, which should not have a balance at the end of the month.

Also, in accordance with the Instruction on the application of the chart of accounts, accounts 20, 23, 29, as well as accounts 90 Sales and 91 Other income and expenses are subject to closing at the end of the month.

In addition, at the end of the year, the accountant needs to prepare regulated reports. To do this, the balance sheet is reformed in December.

How to close the month in 1C 8.3

It is necessary to close the period in 1C 8.3 regularly and consistently. With the help of an assistant Closing of the month such as writing off deferred expenses, depreciation and other necessary operations for the correct distribution of income and expenses and the calculation of income tax. To launch the Monthly Closing Assistant in 1C 8.3, you need to open the Operations section:

Getting into the assistant for closing the month, first of all, you need to set the period - the month that will be closed:

If you switched to 1C 8.3 from another program or entered the balances manually, for example, you entered the balances on December 31, 2013, and accounting began in January 2014, then we select for closing the month in which the first accounting entries began.

Month closing can be done in two ways:

- Full automatic closing;

- Partial closure. In this case, it is necessary to perform one scheduled operation, or it is necessary to do all but one.

The sequence of closing the month in 1C 8.3

To perform this operation in 1C 8.3, after selecting the closing period, click on the Close month button, after which the 1C 8.3 program will perform the following actions:

- Reposting of documents, i.e. bringing to chronological order by time and dates;

- The presence of the document Payroll for the selected month is checked to reflect the amounts of wages and contributions on the expense accounts.

If the 1C 8.3 program does not have a Payroll document for the selected month, then the program creates a document at the end of the period. The amounts of accrued salaries are put down in accordance with the salaries of employees.

Also, when closing the month in 1C 8.3, the following is carried out:

Depending on the organizational and legal ownership, as well as the chosen taxation system, the set of routine operations in 1C 8.3 may differ, for example:

Or, for example:

At the end of the month closing, all scheduled operations on the screen will be highlighted in green:

And the status of the Month-end closing operation will be Executed:

If the closing of the month is not carried out in 1s 8.3

Such a result of closing the month is possible only if there are no accounting errors. If there are errors, then the 1C 8.3 program will not perform the operation and will highlight the operation in red in the assistant:

It will also give an informational message about where the error is and how to fix it:

After correcting the error, you must close the informational error message and click the Close Month button again. The 1C 8.3 program will continue to close the month from the operation in which there was an error:

In addition, when closing last month quarter (in our case, March), the 1C 8.3 program checks for the availability of VAT accounting documents, that is, the formation of a purchase book and a sales book:

Upon completion of each scheduled operation, we can look at the accounting entries or the document by which this operation was made (if possible), and also look at the reference-calculation for the operation. To do this, click on the required operation with the left mouse button and select the required detail:

In 1C 8.3, all reference calculations that can be generated at the end of the month can be seen using a special button in the upper right corner of the month closing assistant:

balance reformation

At the end of the year, when the month of December is closed in 1C 8.3, an additional operation Reformation of the balance sheet appears:

This operation closes accounts 90 and 91 to account 90.09 “Sales profit/loss” and 91.09 “Balance of other income/expenses”. Account 99 is written off to 90.09 and 91.09 and so on.

After the closing of the month, the result of the balance sheet reformation can be seen in the form of accounting entries:

If, for example, you need to perform the OS Depreciation operation right now from scheduled operations, then in the assistant you need to left-click on the desired operation in the assistant and select the Perform operation item:

At the end of the operation, 1C 8.3 will issue an informational message:

If you try to make an operation from the second or third block of the assistant, for example, calculating the reserve for doubtful debts, then the 1C 8.3 program will issue an informational message about the impossibility of performing the operation:

This is because in the Month Closing Assistant, the operations are arranged in such a way that the sequence of closing accounts is observed in accordance with PBU. The 1C 8.3 program will offer to perform all the necessary operations preceding the selected one.

If you do not want to perform all operations, but only the selected one, you can skip all previous scheduled operations:

Attention! To skip an operation means to refuse to perform this operation in the current month. The actual closure of accounts for this operation will not occur, which threatens with unreliable data in accounting.

To get correct and timely reporting for the month, it is necessary to carry out the “Closing of the month” procedure at the end of it in the 1C Accounting 8.3 program developed on the 1C Enterprise 8.3 platform.

The month-end sequence looks like this:

- It is necessary to collect the “Expenses of the current month” on the corresponding accounts (20/25/26/44), and “transfer” them to the “Expense sub-accounts” of accounts 90 and 91.

- As a result of the "carryover" of the amounts from the expense accounts (20/25/26/44), the ending balances in these accounts will be equal to zero.

Attention! For organizations (manufacturing, agricultural producers) whose production increases and affects several months, the account is not closed completely, i.e. the balance will not be zero. Here we also mention trading companies that take into account the transport costs for the delivery of goods to themselves on the 44th account.

- After moving the amounts from expense accounts to 90, we will calculate the ending balances for each - 90 and 91 account. That is, we must find the difference between Dt and Kt for 90 and 91 accounts, and transfer the resulting amount to 99. As a result, the final balances for 90 and 91 will also become zero.

As a result, when closing, we should not have any balances on our accounts (20/25/26/44), but accounts 90 and 91 should also be equal to zero.

How to close the month

A corresponding window will open, listing all the operations* that can be performed within our task. First, we define the “Organization” and designate the closing period we need.

* Closing is important to do gradually, following the sequence, otherwise errors cannot be avoided.

Depending on the policy/type of taxation applied by the firm, not every one of the above transactions will be active. At the same time, their set also determines the closing period - month, quarter or year.

Closing stages

1.Setting up an accounting policy

We select the organization for which we will close, and check the settings.

2.Processing "Closing the month"

After checking the setting for "Konfetprom LLC" and selecting the closing of the month "December 2016", we see that the tabular part will display the operations that will be carried out in the process of processing the "Closing of the month".

It can be done manually for each operation, but we must always remember that they are executed sequentially.

Select the operation for which we want to close, left-click on it, and then - "Run".

The closing was successful, each operation changed the font color to green and acquired a flag*.

*Please note that operations that have a pencil symbol were edited manually.

By clicking on the operation with the left mouse button, we can view its postings, edit, cancel the posting and / or skip it.

I stage of operations

Payroll- one of the few operations that the accountant forms independently. This line is automatically processed.

– this operation is needed to submit a quarterly VAT return. Postings, entries in special registers for the formation of books and declarations will be generated.

- a regulatory document will be created for the accrual / write-off of depreciation charges for expenses.

II stage

Formed Calculation of shares of write-off of indirect expenses.

Stage III

Formed Closing expense accounts(20/23/25/26/44) - the correctness of the data of this action directly affects the cost of production. It is very important to check the correctness of the closure!

IV stage

Closing 90 and 91 hours. generates and calculates income tax (in our example, this is an action to reform the balance sheet).

Month end error

For an error-free closing, we will pay special attention to the closing of cost accounts (20/23/25/26). The reason for a possible error may be hidden in entering incorrect information when creating documents.

On account 20 (Main production) and 23 (Auxiliary production), the following costs are taken into account:

- According to the salary of employees registered in production units;

- Depreciation of equipment and purchase costs, for example, machine tools, etc.

The main and main feature that unites these costs is belonging to a specific product, so they are called "direct". Production costs are distributed according to analytics by product groups - this is the main point for their correct distribution. Costs must have the same insights as the item group. At the same time, the division within it occurs at the planned cost, i.e. proportionally. If the analytics of any cost has nothing to do with any of the manufactured products, then this cost may “hang” in the department. This is the main reason for the error when closing account 20.

On accounts 25 (General production expenses) and 26 ( General running costs) indirect costs are taken into account. Since indirect costs are related to several types of products at the same time, they need to be distributed. Indirect costs include:

- Accounting for depreciation when using equipment for production different types products;

- The salary of employees not directly involved in production.

The case when, after the closing of the month at 44 h. (Distribution costs) there are balances, it can either mean that there were no transactions for the sale of goods, that is, there was no proceeds from trading operations as such, or the remains of transport expenses “hung” on it.

Platforms: 1C:Enterprise 8.3

Configurations: 1c accounting

Version: 3.0

2013-10-08

94391

It's no secret that the main difficulties with 1C begin as soon as the next one ends. reporting period. It is at this time that the lion's share of feverish searches for errors, delays after work, headaches and nervous breakdowns fall.

Most of the errors at the end of the month lie in the incorrect settings of the program, databases and, first of all, in the incorrect, often hastily set settings of the "Accounting policy". Although, it happens that the user is simply not familiar with 1C on "you", and quite sincerely does not see a causal relationship between the "flags" of the settings and the errors that "crawl out" after the operation "Closing the month".

One can understand the poor, always underachieving and overworked accountants - do they have free time to study thick volumes of textbooks with detailed description work in the program? So if you work as an accountant and want to safely survive the reporting period, then we advise you to learn a few simple tricks of “Closing the Month” right now.

We close every month

Novice 1C accountant users often do not realize that, unlike the usual tax period equal to a quarter or a year, the program works so that the reporting period here is equal to one month. Therefore, closing must be done monthly! In particular, expense accounts should not have balances at the end of each month. If you try to close at the end of the quarter, you will get errors and balances on those accounts where they should not be.

Closing expense accounts

If after the close of the month there was a balance on account 44 “Distribution costs”, this may mean one of two things - either the absence of sales of goods (revenue) from trading operations, or the balance of transportation costs.

If the first, then the entire debit turnover on the distribution costs account for the month will be unclosed, which means it is necessary to check whether all sales transactions are included in the database. If the write-off of distribution costs has not passed completely, then you need to check which particular cost items, as well as tax expenses, includes unwritten amounts. To do this, simply generate a balance sheet for account 44.01. If you see that transportation costs remain “hanging”, this means that you see the amounts of transportation costs proportionally tied to the goods remaining in the warehouse. If you think that this is not true or the transport costs are written off disproportionately, then it remains to check whether the “Cost Items” in the directory elements are correctly linked to the transport costs. If not, then correct, reschedule all documents and close the month again.

Cost accounts 20, 23, 25, 26

If you saw the balances “hanging” on the accounts of direct and indirect production costs, that is, on accounts 20, 23, 25, 26, then there will be a little more questions leading to a solution to the problem. The main question here is the following: are the “Accounting policies”, the reference books “Nomenclature group” and “Nomenclature”, “Cost items”, etc., agreed with each other, whether they are configured in accordance with the parameters of your enterprise.

Let us first consider what dangers lie in wait for us when closing indirect expense accounts. If the program informs you about an error during the “Closing of the month” operation, it means that you incorrectly filled in the “Methods of distribution of indirect costs” when setting up the “Accounting policy”. For example, if the indicator "Wages" is selected as the basis for the distribution of indirect costs, then the program will look for the amount of costs by type of costs "Wages" allocated to direct costs accounts 20 or 23. So, if the wages of production workers were originally assigned to account 25, then the Monthly Closing operation will simply not find the amounts to distribute, stop the month closing process and inform you of an error.

The second example of a common mistake, when for a long production cycle, "Output volume" is chosen as the basis for the distribution of costs. Then, if not a single unit of finished products is produced within a month, there will be no basis for the distribution of indirect costs. Draw conclusions and do not approach formally the choice of methods for allocating indirect costs.

Accounting policy settings. Output

Let us return to the issue of output (production) and the provision of services. Do not forget to set the "Product output" checkbox in the "Accounting policy". And then we will carefully and correctly answer the proposed questions.

The first question is whether there are any work-in-progress (ORP) amounts remaining in your business. This issue is directly related and regulated by the duration of the production cycle. The production cycle is less than a month, which means there is no refinery at the end of the month. A long cycle, when the production of a finished unit of goods can stretch for weeks, months and years, means that the balance will always be visible on account 20.01 after the close of the month.

The next question is whether your product is serial. That is, do you produce the same type of products (for example, furniture) or is it important for you to track financial results for each product separately (if, for example, you produce aircraft). If the products are serial, then the WIP balances with a single product group will have to be entered manually, using the “Inventory of WIP” document for this. It is these amounts that will become your account balance on 20.01, reflected at the end of the month.

This task can be simplified by introducing a separate element of the “Nomenclature groups” directory for each product of a long production cycle, establishing a correspondence between the “Nomenclature group” and the “Nomenclature” element. Here the rule laid down in the program will begin to work: if there is no output, then there is no write-off of costs from account 20.01. And you will no longer need to calculate the WIP balance and enter it in a separate document. In addition, when selling a product, you will be able to see income (revenue) and actual expenses related only to a specific product, that is, the financial result for it.

Direct or indirect?

The next question is which costs are direct and which are indirect. For correct work in the program, it is necessary to clearly separate direct costs from indirect ones. It is important to understand that the cost analytics on accounts 20.01 and 23 contain the “Nomenclature groups” subconto, but not on account 25. Therefore, “attribution to direct costs” in 1C means whether the amount of costs for items can be attributed to specific item groups. It is clear that for the correct closing of the month, it is necessary to carefully consider the maintenance of the "Nomenclature groups" directory. For example, if you need to strictly distribute wages on costs in the production of specific types of products, then payroll must be attributed to a specific nomenclature group. If this is not important, then it is more convenient to immediately attribute the salary to account 25, setting the appropriate rule for its distribution in the register.

Separately, general business expenses on account 26 are determined. It is also necessary to correctly set up their description in the “Accounting Policy” of the enterprise. If you want to see the “net” production cost of products, select the checkbox “General business needs are included in the cost of sales”, if not, then select the inclusion in the cost of products, works, services. And then be sure to set the method for distributing these costs and correctly select the base.

Here you can add the following. If you use the program "1C: Accounting 8" only for compiling tax and accounting reports, then the user's priority will be to close the month without errors. If you need real data about actual cost and financial result broken down by specific nomenclature and types of activity, then the approach to program settings should be more serious.

Simple or difficult?

The next question is about the complexity of production, about which functional units are included in the production process. Your production can be simple, complex or multi-part. In the case of a simple production, the above settings will be enough. If the production is complex, multi-part, when several departments can participate in the process, then it is necessary to establish how the semi-finished products transferred from one department to another for processing should be taken into account.

If the redistribution order is set manually, you need to track changes in the list of departments. In the month of the appearance of new branches in the organization, "Closing of the month" will stop the process and report that "the order of departments has not been established." This means that with each change, it is necessary to re-create the list of subdivisions participating in the technological chain. This is what creates the greatest difficulties in accounting, given the fact that financial results are formed on an accrual basis for the year, and their accounting requires costs, the analytics of which are divisions.

Services "for yourself"

An important issue is the possibility of providing services between own divisions. If yes, then you need to choose how to evaluate them. There are two possible options: by the volume (quantity) of services rendered, or by their planned cost. Here, the correct settings for the units of measurement of this service and the same planned cost are also important. It should be noted that the service unit cannot be expressed in pieces, which is always the same. For example, standard freight transport can be expressed in ton-kilometers. And the planned cost should be expressed in an economically justified amount, and not taken “from the ceiling”.

Another question is whether there are commercial expenses at the enterprise? They are essentially distribution costs, but associated with the sale of products. Accounting for these expenses is kept on account 44.02, the distribution of the amounts of these expenses is not provided for by the program. “Closing the month” they are fully debited to account 90.07.

Services "for others"

It's time to think about providing services (or doing work). Accounting for these activities uses the same cost accounts, the same settings as for production accounting. The main difference is that the result of the service is not material. Completion of the production process is finished products in the warehouse, and the completion of the process of providing the service is its implementation and signing of the act by the customer of the service.

For the correct reflection of services in the program, it is necessary to determine some positions. Will you take into account the units of services at the planned cost and use the document "Act on the provision of production services" for their implementation. Or the planned cost is not needed, and then your document for accounting for the service will be "Sales of goods and services", or - when there are many customers, and there is only one service - "Provision of services".

The second important position for determining the financial result of the services rendered is whether you take into account the result for individual works or orders? In this case, it is necessary to consider a strategy for filling out the "Nomenclature groups" directory.

In the ideal case, the "Closing of the month" operation generates a financial result - it takes into account revenue and costs. If the revenue is always there, then there will be no problems. It is only necessary to mark in the "Accounting Policy" in "Production Costs" the checkbox "Performance of work, provision of services to customers, taking into account revenue." However, if for some reason there was no revenue this month, in order to avoid problems with closing the month, you must correctly configure " Accounting policy”, taking into account the actual activity of your enterprise.

And the last thing that can be said about the services. If your company provides services of both a production nature and others, then you can choose the third of the proposed options. It will combine the above two options, but the write-off of costs taking into account revenue will only work for manufacturing services. The rest of the service costs will be written off even if there is no revenue, and in order to get the correct balance of work in progress, you will need to specify it explicitly.

"Closing the Month" will turn from a monthly headache into a real friend and assistant, but only if you take the time and effort to correctly configure the program.