Posting excessively transferred personal income tax to the shareholder's account. Return of personal income tax to the employee, postings and clarified references

Personal income tax or income tax from an individual is a fee that is paid by almost every Russian, if he is a taxpayer, has his own identification number assigned tax service. In addition to Russians, this tax is also removed from non-residents, but who have income from sources located within the Russian Federation.

Any enterprise, organization and even individual entrepreneur may be tax agents, that is, intermediaries between the state treasury and an individual, from whom it will be. The main functions of such agents include calculation, reporting, retention, and .

Such a scheme works if it is the tax agent that is the source of income for the main taxpayer. In other words, the company retains wages of their employees with personal income tax and transfers it to the budget.

Before the tax service, agents undertake to transfer this fee on the day the salary is issued (to the same day) and regardless of the form in which the money will be issued (in cash or by transfer to a bank card).

The amount of tax is calculated on an accrual basis, that is, from the first day of the reporting year to the last day of the current month and is withheld locally legal address agent, not tax payer.

Interest rates for calculating personal income tax

Personal income tax is heard more like income tax. Its most common rate is 13% of income, more often, of wages. But this is not the only amount for withholding this fee, there are also reduced and increased income tax rates.

- The tallest interest rate works when receiving a lottery win or cash prizes, in which case it reaches 35%.

- The personal income tax rate of 30% is applied to non-residents of the Russian Federation who receive income from a source located within Russia.

- Another inflated rate - 15%, is valid for non-residents of the Russian Federation who receive income as dividends from entrepreneurship in the country.

Postings for calculating personal income tax and transferring it to the budget

|

Wiring Description |

Posting amount |

A document base |

||

|

Withholding tax from wages individuals |

Amount of accrued tax |

|||

|

Transfer of personal income tax |

Amount of accrued tax |

Bank statement |

What to do with excessive withholding of personal income tax?

It also happens that the accounting department erroneously or due to lack of reliable information withheld an overestimated amount of tax from its employee. In what cases can an accountant make an adjustment:

- If the tax period (year) has not yet ended.

- The company still removes the increased personal income tax from the employee.

How to post a refund of excess income tax withheld:

|

Wiring Description |

Posting amount |

A document base |

||

|

Reflection of the return of the previously withheld overstated personal income tax |

Accounting certificate, income declaration for individuals |

|||

|

Payment of excess withheld income tax |

Bank statement |

In what cases is the company obliged to return the excessively withheld personal income tax to the employee? When can I limit my account? What documents to issue an accountant?

An overpayment of personal income tax may occur, in particular, due to an error in the calculation of the tax to be withheld from the employee’s income, that is, when the tax is withheld in larger amount than needed.

Excessively withheld personal income tax can be set off against future tax payments or returned to the employee. The choice of option depends on a number of circumstances.

When can I offset the excess withholding of personal income tax

An accountant of a company that is a tax agent can offset the amount of tax withheld from an employee against future payments:

— when the tax period (calendar year) is still running;

- the employee continues to receive from the company that has unduly withheld personal income tax from his income.

Offsetting the amount of excess tax withheld when calculating personal income tax for the current month

The tax period for personal income tax is a calendar year (Article 216 of the Tax Code of the Russian Federation). Personal income tax to be withheld is calculated on an accrual basis from the beginning of the year. When calculating the amount of tax for the current month, the amounts of tax withheld in previous months of the current month are taken into account. tax period(clause 3 of article 226 of the Tax Code of the Russian Federation):

Amount of personal income tax subject to Amount of personal income tax, Amount of personal income tax actually

withholding from salary = calculated - withheld from the beginning of the year

for the past month cumulatively from for the previous months

beginning of the year

That is, the offset is initially “built into” the procedure for calculating personal income tax.

Let's say that from the employee's salary accrued at the end of the past month, the tax was withheld in a larger amount than prescribed by the norms of the Tax Code.

For example, an accountant did not apply the standard tax deduction for a newborn child, because the happy father of the first child brought Required documents only after the 5th of the following month.

The amount of personal income tax calculated without applying a tax deduction turned out to be 182 rubles more. (1400 rubles x 13%).

In this situation, when calculation of personal income tax from the salary for the current month, the accountant will determine the personal income tax on the total income of the employee from the beginning of the year and will offset the amount of tax withheld up to this point (clause 3 of article 226 of the Tax Code of the Russian Federation). It is not necessary to inform the employee about the excessive withholding of personal income tax and require him to apply for a tax credit.

Note.The tax deduction for the first child is 1400 rubles. (Clause 4, Article 218 of the Tax Code of the Russian Federation).

Example 1. On April 25, 2014, the manager I.P. Rokotov had a son. The busy father brought a copy of the child's birth certificate to the accounting department on May 12, 2014.

Taxable income of an employee in 2014 and the amount of personal income tax

| Month of 2014 | Amount of income | Amount of deductions | Taxable base | Amount of personal income tax | |||||

| per month | cumulative since the beginning of the year | per month | cumulative since the beginning of the year | subject to withholding | actually withheld | ||||

| cumulative since the beginning of the year | per month | cumulative since the beginning of the year | per month | ||||||

| January | 22 000 | 22 000 | 0 | 0 | 22 000 | 2860 | 2860 | 2860 | 2860 |

| February | 22 000 | 44 000 | 0 | 0 | 44 000 | 5720 | 2860 | 5720 | 2860 |

| March | 22 000 | 66 000 | 0 | 0 | 66 000 | 8580 | 2860 | 8580 | 2860 |

| April | 22000 | 88 000 | 1400 | 1400 | 86 600 | 11 258 | 2678 | 11 440 | 2860 |

| May | 22000 | 110 000 | 1400 | 2800 | 107200 | 13 936 | 2678 | 13 936 | 2496 |

Solution. Calculation of personal income tax before the submission of documents for a child deduction

For the period January-April 2014, the amount of the employee's income, calculated on an accrual basis from the beginning of the year, amounted to 88,000 rubles.

In the absence of documents on the birth of a child, the accountant calculated the amount of personal income tax without taking into account child deduction.

Since the beginning of the year, the total amount of actually withheld tax amounted to 11,440 rubles. (88,000 rubles x 13%).

Recalculation of personal income tax after receiving documents for a child deduction

After receiving from I.P. Rokotov’s application for the provision of a child deduction and a copy of the child’s birth certificate, the accountant determined that amount of personal income tax, subject to deduction from the employee's salary for January-April 2014, should have amounted to 11,258 rubles. [(88,000 rubles - 1,400 rubles) x 13%].

Consequently, for the period January-April 2014, the accountant withheld personal income tax from the employee's income by 182 rubles more. (11,440 rubles - 11,258 rubles).

The tax period is not over yet, the employee continues to work in the same company, his income will be taxed at the same rate of 13%.

No special action overpayment of personal income tax in the amount of 182 rubles. accountant does not need to do. It will be automatically offset when calculating personal income tax for May.

After the recalculation, the excessively withheld amount of personal income tax can be seen in the debit of account 68 of the sub-account "Calculations for personal income tax".

Calculation of personal income tax from salary for May

Personal income tax is calculated on an accrual basis from the beginning of the year.

To calculate the amount of tax to be withheld from wages for May, the accountant will determine for the period January-May 2014:

- the amount of income - 1,10,000 rubles;

- the amount of deductions - 2800 rubles. (1400 rubles x 2 months);

- the amount of taxable income - 107,200 rubles. (1,10,000 rubles - 2,800 rubles);

— total amount Personal income tax subject to withholding - 13,936 rubles. (107,200 rubles x 13%).

The amount of personal income tax to be withheld from wages for May is equal to the difference between the calculated amount of tax for the period January-May 2014 (13,936 rubles) and the amount of personal income tax actually withheld for the period January-April 2014 (11,440 rubles) (n 3 article 226 of the Tax Code of the Russian Federation).

The amount of personal income tax to be deducted from the salary for May will be 2496 rubles. (13,936 rubles - 11,440 rubles).

In accounting, after the transfer of personal income tax for May, there will no longer be a debit balance on account 68 of the subaccount “Calculations for personal income tax” (provided that personal income tax calculations for other employees were carried out correctly), since the excessively withheld amount of tax was offset when calculating personal income tax for May.

The amount of personal income tax from the salary for May, if the employee submitted documents on time

If the employee submitted an application for the deduction and supporting documents on time, the accountant calculated personal income tax from the salary for April, taking into account the deduction.

Then the personal income tax for the period January-April would have amounted to 11,258 rubles. [(88,000 rubles - 1,400 rubles) x 13%]. And the personal income tax to be withheld from the salary for May would be equal to 2678 rubles. (13,936 rubles - 11,258 rubles). That is more by 182 rubles. (2678 rubles - 2496 rubles).

If there are documents necessary for the application of a tax deduction, excessive withholding personal income tax would not have happened.

Personal income tax offset if the employee's tax status has changed

Let's consider such a situation. At the beginning of 2014, your employee was not yet a Russian tax resident.

When calculating personal income tax, the accountant applied the rate of 30% (clause 3, article 224 of the Tax Code of the Russian Federation).

After a few months, the employee acquired the status tax resident RF. In this case, the amount of personal income tax withheld from his income, calculated at a rate of 30%, must be recalculated at a rate of 13% using standard tax deductions.

In such a situation, an overpayment of personal income tax is formed. It can be offset against withholding tax at a rate of 13% until the end of 2014. This is what it says:

- in the letter of the Ministry of Finance of Russia dated 03.10.2013 N 03-04-05 / 41061;

- letter of the Federal Tax Service of Russia dated September 16, 2013 N BS-2-11 / [email protected]

That is, when calculating personal income tax at a rate of 13% payable for the current month, the accountant will take into account the amount of tax already withheld for previous months at a rate of 30%.

In the event that the amount of tax withheld at a rate of 30% was not credited in full before the end of the calendar year, the employee may apply to tax office for the return of the remaining amount of excessively withheld personal income tax. The refund will be carried out only by the tax inspectorate (clause 1.1 of article 231 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia of 03.10.2013 N 03-04-05 / 41061, the Federal Tax Service of Russia of 16.09.2013 N BS-2-11 / [email protected]).

When the overpayment cannot be credited

Overpayment of personal income tax on dividends. The company paid dividends to the employee. Due to a technical failure in the program, instead of the 9% rate (clause 4 of article 224 of the Tax Code of the Russian Federation), the accountant applied the rate of 15% (clause 3 of article 224 of the Tax Code of the Russian Federation).

As a result, there was an overpayment of personal income tax. It cannot be set off against personal income tax payments from salaries, but can only be returned. This is explained as follows.

The amount of personal income tax from wages is determined separately from the amount of personal income tax from dividends. This follows from paragraph 1 of Article 225 of the Tax Code.

When calculating personal income tax on dividends and personal income tax on wages, different tax rates are applied (9% and 13%), two different tax bases are calculated (clause 2, article 210 of the Tax Code of the Russian Federation).

The calendar year has ended. The total amount of tax is calculated based on the results of the calendar year (clause 3, article 225 of the Tax Code of the Russian Federation).

If at the end of the year there is an overpayment, the accountant cannot set it off against future personal income tax deductions from the income of the next calendar year.

For example, personal income tax was excessively withheld from an employee's salary for 2013. This overpayment cannot be taken into account when calculating tax on income accrued in 2014. Since in 2014 the accountant determines tax base starting from January 1 (clause 3 of article 226 of the Tax Code of the Russian Federation).

The employee quit. Since, after the dismissal, the employee will cease to receive income from this organization, the offset becomes impossible.

When it cannot be credited, it can be returned. In all cases in which it is impossible to set off the excessively withheld personal income tax, it can be returned. You can make a return:

- a company in which an excessively withheld amount of personal income tax was formed. The return procedure is described below;

- tax office. To do this, after the end of the calendar year, the employee can submit a declaration in the form of 3-NDFL. It must be accompanied by a certificate in the form of 2-NDFL (in clause 5.6 of the certificate, the excess withheld amount of personal income tax will be reflected) and an application for a tax refund.

Note. You can apply for a refund of personal income tax within three years after the end of the year in which the tax was excessively withheld (clause 7 of article 78 of the Tax Code of the Russian Federation).

The procedure for the return of excess personal income tax withheld by a tax agent

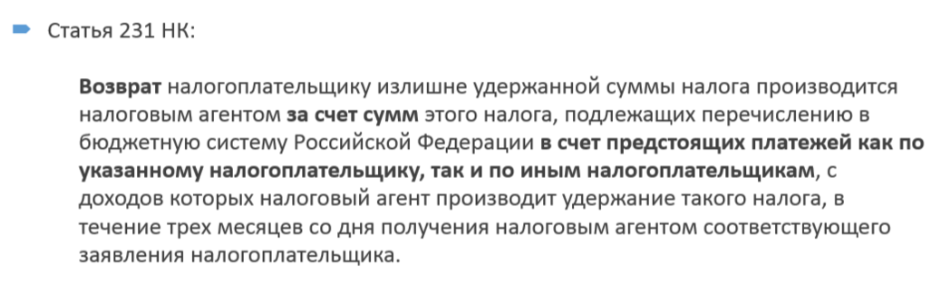

The procedure for the company to return excess withheld personal income tax is described in detail in paragraph 1 of Article 231 of the Tax Code.

Before proceeding with it, the accountant must record the fact of excessive withholding of personal income tax in the accounting statement. Sample 1 is shown on p. 48.

Notifying an employee of an overpayment

The accountant must inform the employee of the excess tax withholding within 10 days from the date of discovery of such a fact. You can do this in different ways:

— send a written notice (sample 2 is given on p. 49);

- supplement the accounting statement with a line on familiarizing the employee with the fact of identifying excessive withholding of personal income tax.

The employee will sign the notice or certificate. His signature will mean that he is familiar. If the employee has already left, the message can be sent by mail with acknowledgment of receipt.

In the opinion of specialists from the main financial department, it is better to coordinate with the taxpayer in advance the procedure for sending the specified message (letter of the Ministry of Finance of Russia dated May 16, 2011 N 03-04-06 / 6-112).

The employee writes a return request

The basis for the return of excessively withheld personal income tax is the application of the employee (clause 1 of article 231 of the Tax Code of the Russian Federation). As in all documents related to the calculation of personal income tax, we advise, in order to avoid the claims of the inspectors, to ask the employee to indicate in the text of the application:

- passport data;

- address of registration;

- TIN (if any).

In the application, the employee indicates the number of the bank account to which the company's accountant will transfer the tax. Sample 3 is shown on p. 50.

From the date of receipt of the application from the employee, the period in which the company must return the tax will be counted.

Return period and source of funds for return

The refund is made within three months from the date of receipt of the application from the employee for the return of the excess withheld personal income tax. The tax is returned by reducing the amount of personal income tax to be transferred to the budget in the future, both from the income of this employee and from the income of other employees.

In case of delay, interest is charged for each calendar day of violation of the deadline based on the refinancing rate of the Central Bank of the Russian Federation that was in force on the days of the violation (paragraph 5, clause 1, article 231 of the Tax Code of the Russian Federation).

When a company applies to the tax office

After receiving an application from the employee for the return of personal income tax, the accountant needs to assess whether the company has the opportunity to return the tax within three months at the expense of personal income tax payable to the budget from the income of other employees (paragraph 2 of the letter of the Ministry of Finance of Russia dated May 16, 2011 N 03-04- 06/6-112).

If the amount of tax to be transferred to the budget is not enough to make a refund within three months, the company can apply to the tax office for a refund of the missing amount. This takes 10 days from the date the employee submitted the return application.

The accountant sends to the tax office:

— an application on behalf of the company for the return of the overdeducted amount;

- an extract from the register tax accounting for the relevant tax period;

- documents confirming the excessive withholding and transfer of the amount of tax to the budget system of the Russian Federation.

The tax inspectorate will return the amount of personal income tax in the manner prescribed by Article 78 of the Tax Code.

Before receipt of this payment, the accountant has the right to return the money at the expense of own funds companies (clause 1, article 231 of the Tax Code of the Russian Federation).

The tax agent is obliged to transfer the excess withheld amount of personal income tax to the bank account of the employee.

Note. It is impossible to return excessively withheld personal income tax in cash (paragraph 4, clause 1, article 231 of the Tax Code of the Russian Federation).

When the return of personal income tax is carried out by the tax agent

The year has not ended, but the employment contract with the employee has been terminated. In this case, the tax agent can return the excess withheld personal income tax, however, subject to the following conditions:

- the fact of excessive withholding of personal income tax was revealed before the end of the tax period in which it occurred and the employee was fired;

- the refund procedure was launched before the end of this tax period.

The absence of an employment relationship is not in this case an obstacle to the return of excessively withheld personal income tax.

The letter of the Ministry of Finance of Russia dated July 2, 2012 N 03-04-06 / 6-193 states that the termination of labor relations between the taxpayer and the organization - the source of payment of income from which the tax is excessively withheld, as well as the period in which the refund of the excessively withheld tax is made , does not affect the procedure for applying the norms of Article 231 of the Tax Code.

Example 2. Salary of the manager of Vesna LLC I.V. Tsvetochkina - 18,000 rubles. For January-March 2014, she received a salary of 54,000 rubles. and issued material assistance for the holiday of March 8 - 3000 rubles.

The worker has a 9-year-old child. I.V. Tsvetochkina wrote an application for a child deduction. Its amount for the period from January to March 2014 amounted to 4200 rubles, personal income tax withheld in the amount of 6864 rubles. On March 31, 2014, the employee quit.

On April 30, 2014, the accountant discovered that an error had occurred. When calculating the tax, material assistance was included in the taxable base - paragraph 28 of Article 217 of the Tax Code was not applied, stating that material assistance in the amount of not more than 4,000 rubles. not subject to income tax. It is necessary to return personal income tax I.V. Tsvetochkina.

Solution. The accountant prepared the accounting statement. See sample below.

Sample 1. Accounting certificate

Accounting reference N 17

April 30, 2014 accountant O.V. Bubnova revealed the fact of excessive withholding of personal income tax from the income of manager I.V. Tsvetochkina for January-March 2014.

In the taxable base for personal income tax, material assistance in the amount of 3,000 rubles was mistakenly included. For January-March 2014, the employee's income amounted to 54,000 rubles, the amount of standard tax deductions was 4,200 rubles, personal income tax withheld and transferred was 6,864 rubles. After recalculation, the amount of personal income tax to be withheld for the period from January 1 to March 31, 2014 is 6474 rubles. The amount of overtax withheld amounted to 390 rubles. (6864 rubles - 6474 rubles).

The following entry must be made in the accounting records:

Debit 70 Credit 68 sub-account "Settlements with the budget for personal income tax"

— 390 rubles. - the excess withheld amount of personal income tax has been reversed.

About the fact of overholding personal income tax the agent must inform the former employee. Chief Accountant A.A. Vetrova compiled an official letter, registered it in the journal of outgoing correspondence and sent it to I.V. Tsvetochkina letter by mail with acknowledgment of receipt. See a sample letter below.

Sample 2. Notification of an employee about excessive withholding of personal income tax

Limited Liability Company "Spring"

Notification

on the discovery of the fact of excessive withholding of personal income tax

Dear Irina Vyacheslavovna!

We notify you that from your income for January-March 2014, the amount of personal income tax in the amount of 390 rubles was excessively withheld.

In accordance with paragraph 1 of Article 231 of the Tax Code Russian Federation You have the right to apply in writing for a refund of the excess withheld amount of personal income tax.

In the application, please indicate the details of the bank account to which Vesna LLC will transfer the overdeducted amount of personal income tax.

We notify you that in the absence of an application, Vesna LLC will not be able to refund the excess withheld personal income tax. But at the end of 2014, you have the right to apply to the tax office at the place of residence with tax return in the form 3-NDFL and an application for the return of excessively withheld personal income tax.

Chief Accountant Vetrova A.A. Vetrova

I have read this notice and received one copy.

Tsvetochkina I.V. Tsvetochkina

The former employee returned the second copy of the notice with a signature on its receipt and sent an application for a tax refund.

Sample 3. Application for the return of excessively withheld personal income tax

To accounting to CEO Vesna LLC to Travkin G.B.

make a refund from Tsvetochkina I.V., registered

Travkin 04/30/2014 at the address: 141282, Moscow region,

Ivanteevka, st. Sadovaya, d. 15 apt. 3,

passport series 96 081 N 124789,

issued by the Federal Migration Service for the Moscow Region

Ivanteevka 10/15/2012, TIN 509300004156

Statement

In accordance with paragraph 1 of Article 231 of the Tax Code of the Russian Federation, I ask you to return to me the overdeducted amount of personal income tax in the amount of 390 rubles. to my card 4276 3800 9517 5301, issued by Sberbank using the details:

account 30301 810 038006003805 in Sberbank of Russia JSC Moscow,

c/s 30101 810 4000000000225, BIC 044525225

Tsvetochkina I.V. Tsvetochkina

The accountant transferred the excessively withheld tax to the former employee on June 11, 2014, made the following entry in accounting:

Debit 70 Credit 51

— 390 rubles. - excessively withheld personal income tax is transferred.

After this entry of account balances 70 and 68 in relation to I.V. There will be no flower.

Since the tax was returned in June, the accountant reduced the personal income tax payment for June by 390 rubles. (paragraph 3, clause 1, article 231 of the Tax Code of the Russian Federation).

If a company applies for a refund of personal income tax to the tax office, the receipt of funds from the budget must be documented by the entry: Debit 51 Credit 68 sub-account "Calculations for personal income tax", and the transfer of excessively withheld personal income tax to the employee - in the usual manner by posting: Debit 70 Credit 51.

Consider the solution to the problem of returning personal income tax based on the application of the employee.

After studying the material you will learn:

- how to register the return of personal income tax to an employee at his request in the 1C: ZUP 3 program;

- what amount of personal income tax to transfer to the budget after the return of the tax to the employee and how to reflect this in the 1C: ZUP 3 program;

- how the amount of personal income tax refund is reflected in the reports: 2-personal income tax, 6-personal income tax, the Register of tax accounting for personal income tax.

Regulatory regulation and stages of personal income tax return

To solve the problem, it is first necessary to consider the normative regulation of the return of personal income tax. The procedure for the return of personal income tax to the taxpayer is described in Art. 231 of the Tax Code of the Russian Federation.

Steps for VAT return:

- excessively withheld personal income tax;

- notify the employee within 10 working days;

- the employee must write a statement;

- within 3 months, the organization must return personal income tax;

- the return of personal income tax is made strictly to the employee's bank account, i.e. You can not return personal income tax through the cashier.

Registration of property deduction and recalculation of personal income tax

The property deduction for an employee is registered in the program by a document Notice to the HO of the right to deduct (Taxes and Contributions - Application for Deductions - Notice to DOs of Eligibility for Deductions).

It states:

When calculating wages for March 2017 in the document Payroll and contributions recalculation of personal income tax from the beginning of the year.

On the tab personal income tax reflects the amounts actually provided property deduction for 10,000 rubles. for 3 months and personal income tax is recalculated for January and February 2017 at -1,300 rubles:

On the tab Payout Adjustment the amounts of personal income tax to be returned are reflected:

According to the amounts on this tab, you can track the occurrence of excessively withheld personal income tax, which must be reported to the employee.

Return of personal income tax

You can check the amount to be returned using the service Analysis of personal income tax return (Salary - Service - Analysis of personal income tax to be returned):

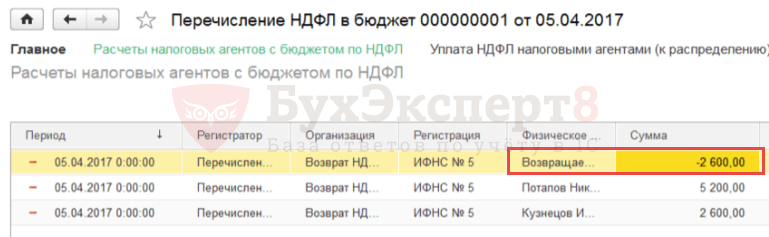

To register a refundable amount of personal income tax, an employee needs to create a document Return of personal income tax (Taxes and contributions - Personal income tax refund).

In field Month select the month in which the personal income tax refund will be reflected. By button Update refundable amounts the amount is automatically loaded - 2,600 rubles. with the date of receipt of income - 28.02.2017:

The refund payment can be made together with the salary payment.

Transfer of personal income tax to the budget in the month of the tax refund

In the month when the tax refund occurred, the amount of personal income tax transferred by the organization to the budget is reduced by the amount of the returned personal income tax.

For this, the document Statement to the bank must uncheck The tax is listed along with the salary :

As a result, when conducting Vedomosti information will be recorded on the amounts paid to the employee and personal income tax withheld.

In order to reflect the fact of tax transfer in the program, it is necessary to create a document Transfer of personal income tax to the budget (Taxes and contributions - Personal income tax transfers to the budget).

When conducting a document Transfer of personal income tax to the budget in the accumulation register, a negative transfer will be written off for the employee for whom the return was made, and for the rest of the employees they will be registered as the transferred amounts exactly deducted from them:

Clarification of the date of receipt of income in the document "Return of personal income tax"

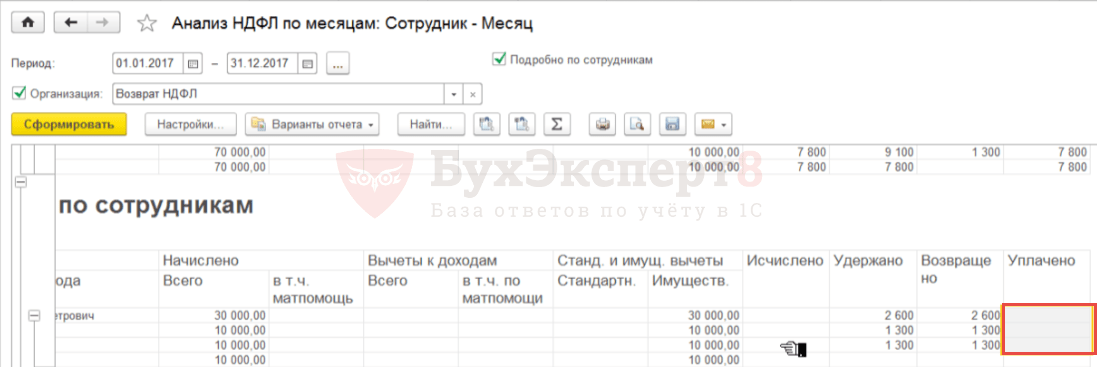

To check the correctness of the reflection of information on the return of personal income tax and its transfer, you can generate a report Personal income tax analysis by months (Taxes and contributions - Reports on taxes and contributions - Personal income tax analysis by months) grouped by Employee and Month of the tax period.

In general, the amount of personal income tax paid for the employee Returnable I.P. - zero, but there is a positive and negative amount for January and February, respectively:

It turns out that in the program:

- for January 2017: personal income tax withheld but not returned was recorded. Remaining amount of tax paid;

- for February 2017: personal income tax withheld and excessively returned was recorded. There is a negative amount of tax paid.

If necessary, to:

- the amount of returned personal income tax corresponded to the amount of tax withheld not only as a whole for the period, but also for each month;

- the amount of personal income tax paid became zero not only in general for the period, but also for each month,

then you need to manually correct the information in the document Return of personal income tax , breaking the total amount of 2 600 RUB. (automatically included in February) for two periods: January and February, 1,300 rubles each:

After that, you need to update the tax information in the document Statement to the bank by pressing the corresponding button Update Tax .

As a result, in the accumulation register Calculations of tax agents with the personal income tax budget the negative transfer for the employee will be divided into 2 lines - for January and February:

In the report Personal income tax analysis by months the transferred personal income tax as a whole for the period and for each month will become zero. The amounts of returned and transferred personal income tax will coincide not only in general for the period, but also for each month:

Reflection of the return of personal income tax in the reports: 2-NDFL, 6-NDFL, Registers of tax accounting for personal income tax

Help 2-NDFL for transfer to the IFTS (Taxes and contributions - 2-NDFL for transfer to the IFTS) personal income tax refund is not reflected separately, the amount of the refund reduces the amount of tax withheld. Due to the decrease in the amount of tax transferred to the budget by the amount of personal income tax returned to the employee, the tax transferred before this operation is also reduced.

As a result, in the example under consideration, after registering the tax refund in the 2-NDFL certificate, the tax calculated, withheld and transferred will be equal to zero:

In the calculation of 6-NDFL for the 1st quarter of 2017, the amount of returned personal income tax will be reflected in line 090 of Section 1. Section 2 does not reflect the amount of personal income tax refund.

V ( Taxes and contributions - Reports on taxes and contributions - Tax accounting register for personal income tax) the operation of the return of personal income tax is reflected as follows:

In release 3.1.2.213 in Register of tax accounting for personal income tax column filled in incorrectly The amount of tax not withheld by the withholding agent , which reflects the amount of the returned personal income tax. This is a registered bug in the 1C: ZUP program, which will be fixed in the next releases.

The procedure for the return of overpaid personal income tax amounts

Remark 1

V tax code Russian Federation, namely, Article 231 defines the procedure for the return of an excessively withheld amount of personal income tax. The refund must be made by the withholding agent. In the event that there is no tax agent, the refund is carried out by the tax authority at the place of registration of the taxpayer.

Too much withholding of personal income tax from the taxpayer's income can be detected by both the taxpayer and the tax agent. In the event that the fact of an overpayment for personal income tax was discovered by a tax agent, then he is obliged to inform the employee about this. This must be done within ten days from the date when this fact was discovered.

The amount of personal income tax that was excessively withheld, in without fail is subject to return to the taxpayer employee on the basis of his written application.

It is also worth noting that the Tax Code does not indicate a clear form and method for informing an employee of the fact of excessive personal income tax withholding, as well as its amount. This suggests that this procedure can be carried out in an arbitrary form.

The refund of the amount of excess personal income tax withheld is carried out within three months, starting from the day of receipt, as the corresponding application of the taxpayer was received by the tax agent. The refund must be made at the expense of the amounts of this tax, which are payable to the budget against future payments, as per this taxpayer, and for other employees-taxpayers, from whose income the tax agent deducts this type of tax.

Remark 2

The transfer of overpaid amounts of personal income tax to an employee is carried out only in a non-cash form.

Very often there are situations when the amount of personal income tax that is subject to transfer to the budget is not enough to refund the tax to an employee in set time. In this case, the employer should apply for a tax refund to the tax office with an application for a refund of the excess tax withheld.

Reflection of the return of personal income tax in the program 1C: Accounting

In the event that a higher personal income tax was withheld from the employee, the program will report this. This can be seen by going to the document "Payroll". By opening this document and going to the "Personal Income Tax" tab, you can see negative tax amounts.

In the same document, on the “Payment adjustments” tab, the amount to be offset is given. This occurs if the amount of income tax with a minus sign is greater than the amount of tax accrued for the current period.

After this document is posted, a posting will be generated: Dt 70 Kt 68.01, and the amount of the posting will be negative.

This amount of tax is reflected in the form of debt of the organization, which does not increase the amount payable to the employee. Excessively withheld personal income tax is taken into account when calculating the employee's wages in the following periods and reduces the amount of the calculated tax.

If you need to return the excessively withheld amount of personal income tax, then you should draw up the document "Return of personal income tax".

In order to draw up this document, you need to go to the "Salary and personnel" section and select "All documents on personal income tax". By pressing the "Create" button, the document we need is selected, namely "Personal Income Tax Return".

This document must include:

- date of the document;

- Name of company;

- The month of the tax period in which the tax refund occurs;

- An employee who is receiving a refund of overtax withheld.

In this case, the tabular part of the document is filled in automatically after the required employee has been selected in the "Employee" field. The date of receipt of income, as well as the amount of tax to be refunded, will be automatically entered.

If necessary, you can update the amounts to be refunded by clicking the "Update refundable amounts" button, or you can add amounts manually by clicking the "Add" button.

The document itself "Personal income tax return" in the program 1C: Accounting does not generate postings. With its help, only the amount of the tax to be returned is formed, which will subsequently be reflected in the tax accounting registers for personal income tax.

April 2017

An overpayment may occur when submitting adjustment reports, and a real overpayment when the payment amount exceeds the calculation amount due to an error in the CCC or other errors. These situations can be prevented or corrected ... If the overpayment did not arise from personal income tax.

How to detect overpayment

The offset and refund of amounts of overpaid taxes, fees and fines is regulated by Art. 79 ch. 12 of the Tax Code of the Russian Federation. To identify overpayments, you need to analyze account 68 "Calculations for taxes and fees". Having formed an analysis of the account according to those indicated in Fig. 1 settings, you can see how a positive was formed. To do this, select the analysis of the account, then in the "Grouping" tab, check the box "By sub-accounts" and in the field "Types of payments to the budget (funds)".

Note that the Federal Tax Service prefer not to return the overpayment, which is more than three years old. Tax authorities count from the date of occurrence of the overpayment. If you go to court, it will be easier, since in this case the date of the overpayment will be the one on which you learned about the surplus - the date of receipt of the reconciliation act or certificate of calculations for taxes and fees (Resolution of the Supreme Arbitration Court of the Russian Federation dated April 13, 2010 No. 17372 / 09).

Therefore, it is advisable to reconcile settlements with the IFTS every quarter, an application for a desire to reconcile can be submitted to the regulatory authorities in writing or via telecommunication channels (Order of the Federal Tax Service dated 03.03.2015 No. ММВ-7-8 / [email protected]"On the approval of the forms of documents used tax authorities when offsetting and refunding amounts of overpaid (collected) taxes, fees, penalties, fines).

What to do in case of overpayment

If the amount of personal income tax was transferred to the budget in excess of the prescribed amount, then there will be no possibility to return this amount as personal income tax. After all, an organization or an individual entrepreneur in this case is a tax agent, and they do not pay for themselves, therefore, it will also not work to set off this amount against the arrears on other obligations ( payment of personal income tax at the expense of the employer is prohibited in accordance with paragraph 9 of Art. 226 of the Tax Code of the Russian Federation). To return the overpayment, you must write an application to the Federal Tax Service Inspectorate for the return of overpaid funds that are not personal income tax.

If the overpayment arose as a result of filing corrective reports, then the application must be submitted only after the submission of reports to the tax office or after receiving positive protocols when sent via telecommunication channels.

First you need to reconcile with the tax office, asking them for a reconciliation report and a certificate on the status of payments for taxes, fees and insurance premiums. After making sure that there really is an overpayment, write a statement in two copies. If, when creating a payment order, you enter the BCC manually, then there is a possibility of an error. To exclude it, you can use the "KBK Designer" (Fig. 2).

When you click on the list of payment details, a window with the KBK constructor will appear. By clicking on it, you can go to the menu and enter the necessary data in parts. A description of the tax/fee or penalty/penalty you are about to pay will appear below, which is an additional check.

Overpayment offset

You can also offset the overpayment for other taxes, penalties, fines. But here it must be borne in mind that the offset is made only within the framework of one level of the budget. It is impossible to transfer the positive balance of tax to the federal budget into a tax to the local budget. For example, overpayment land tax VAT arrears cannot be repaid, as well as in income tax overpayment on federal budget will not be offset against the debt to the regional budget.

If you have surplus interest or penalties, you can transfer them to pay off tax arrears.

To offset the overpayment for arrears, it is required to write an application in two copies "Application for offsetting the amount of overpaid tax (fee, penalty, fine)". The inspection will consider it within 10 working days.

Mutual settlements with funds are reflected in the account 69 "Calculations for social insurance and security". Similarly to the account, we check the data on account 69.

In case of excessive payment to the funds, applications of the form 23-FSS and 23-PFR should be written; applications for transfer - 22-PFR and 22-FSS, when clarifying the payment, a letter is written in free form. Applications should be submitted to the FIU and the FSS, after consideration, the funds will transfer information about the decision to the tax office, and return cash she will. When offsetting contributions, as well as when offsetting taxes, it is possible to transfer surpluses from one payment item to another, but a positive balance from the PFR cannot be taken into account for arrears in the FSS.

When returning an overpayment upon liquidation, an organization should apply for a refund of the surplus before closing the current account, and it should be borne in mind that the application may be considered within a month. According to paragraph 4 of Art. 49 of the Tax Code of the Russian Federation, the return of the IFTS is made only by organizations; if the company was liquidated, then its founder is not entitled to claim the declared amounts.

- The procedure and stages of developing a credit policy of an enterprise Development of a credit policy of an enterprise tutorial

- New buildings in the Moscow region with a marketing mortgage 5 percent mortgage

- Unbudgeted expenses and unfulfilled obligations Ways to calculate unforeseen costs

- How to check the financial solvency of the partner enterprise