Where in 1s is the revaluation of foreign exchange funds. Revaluation of Currency Funds: Transactions

Sometimes organizations need to buy or sell foreign currency. The situation can be a lot. For example, you import or export goods, send employees on business trips abroad, pay off a loan in foreign currency etc.

Current legislation obliges organizations to re-evaluate currency balances in rubles at the established rate. In the event of a foreign exchange difference in a positive direction for you, it is reflected as other income in the BU and as non-operating income in NU. The amount of the negative difference is accounted for in the same way, only for consumption.

In this article, we will look at an example of how currency conversion operations are performed in 1C 8.3 and consider their postings, namely, buying and selling currency.

Before you start working with currency, you need to configure the program.

In the event that a transfer between a foreign currency and a ruble account takes more than a day, you will need to use an intermediate 57 account.

From the "Main" section go to.

In the window that opens, find the item called "Account 57 is used" Transfers in transit "when moving money»And mark it with a flag. This add-on does not need to be enabled.

It is also recommended to check the installation of another add-on. In the "Administration" menu, select "Functionality". In the settings window that appears, open the “Calculations” tab and check if the checkbox is set on the “Calculations in currency and USD” item. We already had it installed by default.

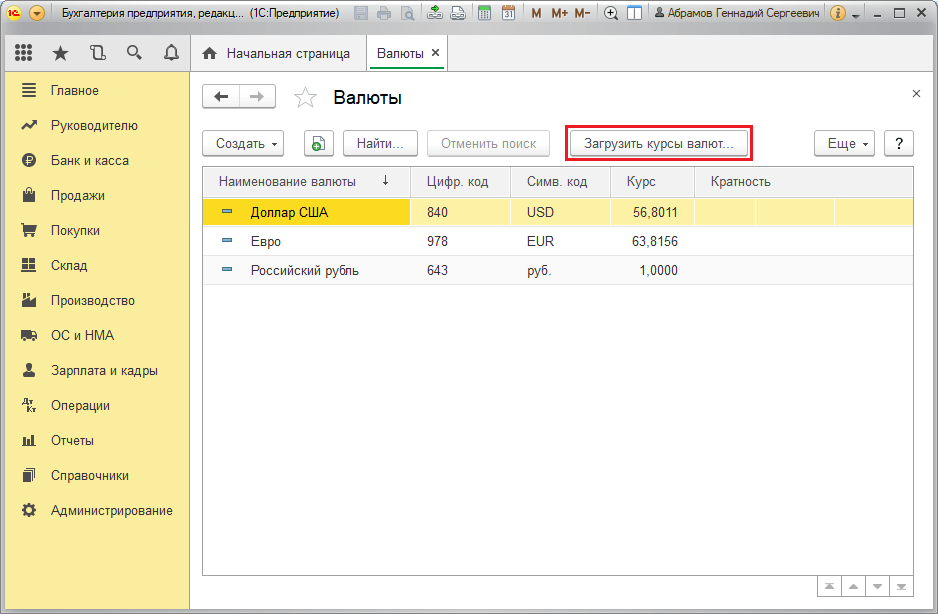

In the "References" section, select "Currencies".

You will see a list of all currencies added to the program with their rates. In this form, click on the button "Download currency rates ...".

The program will prompt you to select those foreign currencies for which you want to download the rates. Check the boxes and click on the Download and Close button. The default is the current date, but you can change it.

Now you can proceed directly to our example of selling and buying currency in 1C 8.3.

Sale of currency

Writing off foreign currency

Consider an example when our organization needs to sell $ 7,000 to Sberbank for rubles. Initially, 1C creates payment order and based on it. We will not consider the payment order itself, and we will immediately proceed to the debiting procedure, since it is this order that makes the necessary transactions.

Specify "Other settlements with counterparties" as the type of operation. The recipient in our case is PJSC Sberbank... We have already signed an agreement with him with settlements in USD. He is selected in the card of this document. The picture below shows the card of this contract.

We will also indicate in the write-off account 52 (Foreign exchange accounts) and settlement account 57.22 (Foreign currency sales). In addition, you must indicate your organization and bank account.

Let's post the document and consider its postings. You can see that not only the write-off itself was reflected, but also the exchange rate differences.

If the currency has changed its value since the last foreign exchange transaction, 1C will also add a posting to calculate the revaluation of currency balances (if revaluation is configured).

Receipt to the current account

After the bank receives $ 7000, he will transfer it to us in ruble terms. The program is taken into account by the document.

Receipt is filled in automatically after unloading from the client bank. Nevertheless, it is recommended to check the filled in details, especially the account and the amount.

The movements of this document are shown in the figure below.

Buying currency

In the case of buying currency in 1C 8.3, you need to perform the same actions as in the previous example.

In this situation, the write-off will have the form "Other settlements with the counterparty". In transactions for the purchase of currency, instead of 57.22, there will be 57.02 (Purchase of foreign currency). Receipt to the settlement account will be in the form of “Purchase of foreign currency”.

Within the framework of this article, the main cases of the occurrence of exchange rate differences will be sanctified, as well as how to reflect the exchange rate differences in 1C 8.3.

According to clause 4 of PBU 3/2006, the value of assets and liabilities in foreign currency or c.u. for display in accounting and reporting is converted into rubles. The difference in the assessment that arose as a result of this is called the exchange rate.

According to paragraph 5 of PBU 3/2006, the conversion is carried out at the official exchange rate to the ruble, i.e. at the rate of the Central Bank of the Russian Federation or at another possible rate, if such a rate is established by agreement of the parties. Another rate by agreement of the parties may be, for example, the USD + 1% rate.

The funds are recalculated (in the bank, at the cash desk), as well as the cost of "accounts receivable" and "creditors" * in foreign currency, which is carried out according to such rules as:

- By the date of receipt or write-off of DC in currency / repayment of obligations;

- By the reporting date, i.e. on the last day of the month.

* Advances issued and received in this structure are not subject to revaluation.

The difference resulting from the recalculation will be reflected in accounting as other income or expenses (due to the fact that it is negative or positive) on 91 accounts. In the tax (income tax) it is reflected as non-operating income or expense on the same account, and it will not be reflected in the STS.

We set up the accounting of exchange rate differences in 1C 8.3

To set up exchange rate differences in 1C 8.3, first of all, you need to correctly set the details of the contract with the counterparty. In this case it comes on contracts denominated in foreign currency.

In 1C: Accounting 8.3, an agreement with a counterparty can be found at the "Contracts" link of the "Contractors" directory element or in the "Contracts" directory. Both guides are located in the "Guides - Purchases and Sales" section.

Figure 1 - Section "Contracts" of the directory element "Contractors"

Figure 2 - Directory "Contracts"

Consider two cases of concluding contracts in foreign currency.

If it is concluded with a resident, settlements can be made only in rubles, since in accordance with the Law of 10.12.2003 No. 173-FZ "On foreign exchange regulation and control" foreign exchange transactions between residents are prohibited.

In the 1C 8.3 program, the setting of a contract with a resident expressed in currency will look like this. In the section "Calculations" for the variable "Price in" the currency value will be set and the switch "Pay in" rubles will matter.

Figure 3 - Settings of an agreement with a resident

An agreement with a non-resident implies the possibility of mutual settlements in foreign currency, since in accordance with the Law of 10.12.2003 No. 173-FZ non-cash foreign exchange transactions between a resident and a non-resident can be carried out without restrictions.

In the 1C 8.3 program, the setting of a contract with a non-resident expressed in currency will look like this. In the section "Calculations" for the variable "Price in" and switch "Pay in" the currency value will be set.

Figure 4 - Settings of an agreement with a non-resident

If the details are configured correctly and the loaded courses are up-to-date *, all the data necessary for calculations will be filled in 1C documents automatically.

* Rates can be loaded in manual or auto-mode into the information register "Currency rates".

For manual loading, open the "Currencies" directory in the "Reference books / Bank and cash desk" section and click "Load currency rates".

Figure 5 - Directory "Currencies"

Add to new currency in the reference book you can click on the "Create - New" button or select the required one from the classifier using the "Create - By classifier" button.

Figure 6 - Adding currency from the classifier

For automatic loading, the settings of the scheduled task of the same name are performed.

Accounting for exchange rate differences in 1C 8.3

So, if the listed settings in the 1C program are performed correctly, then the exchange rate difference is reflected automatically:

- By date of operation, by means of the document that registers this operation. For example, through the documents “Receipt / write-off from the current account”, “Sale / receipt of goods”.

- At the end of the month by means of "Revaluation of foreign exchange funds", which is automatically launched in the "Close of the month" procedure.

Reflection of exchange rate differences in 1C 8.3

Example # 1. In terms of purchasing goods under a contract in foreign currency

In our example, under a contract with a supplier, the goods were shipped before payment. This event was recorded through the Goods Receipt document.

Figure 7 - Contract with the supplier

Figure 7 - Contract with the supplier

The rate in "Goods receipt" was filled in automatically from the information register "Currency rates".

Figure 8 - "Receipt of goods"

Figure 8 - "Receipt of goods"

Figure 9 - Transactions on "Goods receipt"

Figure 9 - Transactions on "Goods receipt"

The payment was made a few days later than the shipment and was registered in the program using the document "Write-off from bank account". The currency rate in it was filled in automatically from the “Currency Rates” register, the “Amount” variable contains the value of the withdrawal amount in rubles, the “Settlement amount” variable contains the value of the withdrawal amount in foreign currency. The currency rate on the date of payment is filled in the "Settlement rate" variable.

Figure 10 - Document "Write-off from bank account"

Figure 10 - Document "Write-off from bank account"

The posting on the exchange rate difference in this case was displayed by the document "Write-off from the settlement account", since the creditors' value was recalculated at the date of settlement of the liability, i.e. on the date of payment.

The exchange rate difference is equal to 702 752.79 - 706 446.64 \u003d | -3 693.85 | \u003d 3 693.85 rubles. The resulting value coincides with the value in the exchange rate difference posting Dt 91.02 - Kt 60.31 in the document "Write-off from the current account". Thus, the negative exchange rate difference was reflected in account 91.02 “Other expenses”.

Figure 11 - Postings on the document "Write-off from the bank account"

Figure 11 - Postings on the document "Write-off from the bank account"

Example # 2. In terms of currency trading

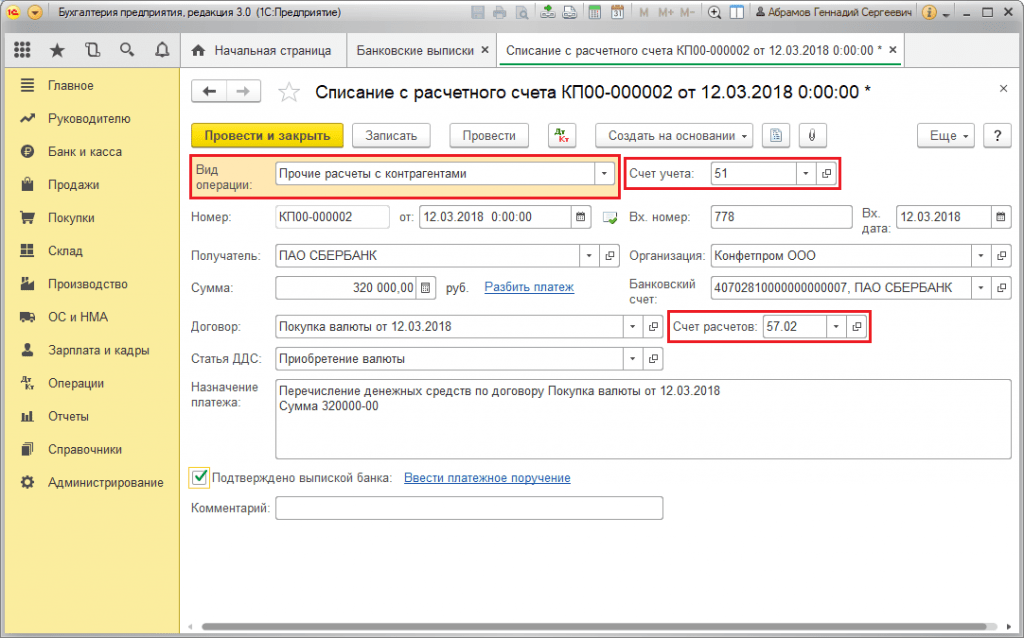

As part of the operation buying currency the transfer of DS to the bank is carried out through the document "Write-off from the settlement account" (type "Other settlements with counterparties"). The "Accounting account" variable contains account 51 "Settlement accounts", and "Settlement account" - 57.02 "Purchase of foreign currency".

Figure 12 - Transfer of funds to the bank for the purchase of currency from the document "Write-off from bank account"

Figure 12 - Transfer of funds to the bank for the purchase of currency from the document "Write-off from bank account"

Figure 13 - Transactions "Write-off from the bank account"

Figure 13 - Transactions "Write-off from the bank account"

For crediting the purchased currency to the account (respectively, foreign currency) comes from "Receipt to account" with the operational type "Foreign currency acquisition". The line "Accounting account" contains account 52 "Currency accounts", and "Settlement account" - 57.02 "Purchase of foreign currency". "Bank rate" contains the exchange rate set by the bank for the purchase of currency. The Central Bank rate is filled in by an automatic machine in the requisite of the same name on the date of the operation. To display the difference, "Reflect the difference in exchange rates as part of expenses" is activated.

Figure 14 - Crediting the purchased currency to the foreign currency account through the "Receipt to the bank account"

Figure 14 - Crediting the purchased currency to the foreign currency account through the "Receipt to the bank account"

The DS in the amount of 312,406.05 rubles is credited at the exchange rate of the Central Bank and is displayed by transactions Dt 52 - Kt 57.02 "Purchase of foreign currency".

Here, the exchange rate difference occurs as a result of recalculating the DS on the date of receipt, therefore, it is displayed in the "Receipt to settlement account".

The exchange rate difference is equal to 312 406.05 - 315 700.00 \u003d | -3 293.95 | \u003d 3 293.95 rubles. The resulting value coincides with the value in the exchange rate difference posting Dt 91.02 - Kt 57.02 in the document “Receipt to the current account”.

Thus, the negative exchange rate difference was reflected in account 91.02 “Other expenses”. Posting exchange rate difference in 1C:

Figure 15 - Posting on the exchange rate difference when buying currency in the document "Receipt on account"

Figure 15 - Posting on the exchange rate difference when buying currency in the document "Receipt on account"

The sum of 320,000.00 rubles transferred for the purchase of foreign currency was more than the amount spent 315,700.00. Therefore, the balance of funds in the amount of 320,000.00 - 315,700.00 \u003d 4,300 rubles must be credited to the ruble account by means of the document “Receipt to the current account” with the transaction type “Other receipt”.

Operation currency sales is carried out in a similar way:

- The transfer of funds to the bank from the foreign currency account is registered in the “Write-off from the bank account” with the type “Other settlements with counterparties”. The "Accounting account" variable contains account 52 "Currency accounts", "Settlement account" - 57.22 "Foreign currency sales".

- DS crediting from the sale of foreign currency to the ruble account is carried out through the "Receipt to the current account" with the operation type "Receipts from the sale of foreign currency". "Accounting account" and "Settlement account" contain accounts 51 and 57.22, respectively.

Example # 3. In terms of recalculation on the final day of the month

Within the routine operation "Revaluation of foreign exchange funds" the document is automatically launched in the "Month-end closing" procedure located in "Operations / Period-end closing" or in "Operations / Period-end closing / Regular transactions".

Figure 16 - Procedure "Close of the month"

Figure 16 - Procedure "Close of the month"

When performing the routine operation "Revaluation of foreign currency funds", the value of the balances is converted into rubles for all accounts with the sign currency accounting at the rate of the Central Bank of the Russian Federation in the Currencies reference book. In case of revaluation of foreign currency funds, the balance in foreign currency shall be considered unchanged.

Figure 17 - Transactions of revaluation of foreign exchange funds

Figure 17 - Transactions of revaluation of foreign exchange funds

The balances in the regulated accounting currency (rubles) are calculated at the rate indicated in the Currencies reference book at the time of the revaluation, therefore, before the operation, you should make sure that the current exchange rates of the currencies are set on the required date of the reporting period (the final day of the month).

Domestic entrepreneurs have access to business using monetary units of other states. But all operations carried out, from cash disbursements to non-cash bank transfersare strictly regulated by the laws of the Russian Federation. The article below analyzes the revaluation of currency balances and the nuances of the revaluation, notes the features of calculations and accounting for exchange rate differences.

The essence of the revaluation of currency balances

The revaluation of the balances of foreign exchange funds of companies means the procedure for converting them into domestic monetary units (RUB) at the official exchange rate of the Central Bank on the day of the revaluation.

It is carried out by:

- on the date of registration accounting statements (last number of the quarter);

- as the foreign exchange quotation fluctuates;

- on the date of transfer money supply from accounts or its crediting.

The revaluation process affects:

- currency mass at the cash desk of the company;

- funds on accounts;

- payment documentation;

- financial investments.

Important! The exchange rate difference is calculated as the deviation between the previous estimate in RUB and the new value determined on the revision day.

Revaluation of foreign currency balances upon purchase

The acquisition of foreign currency by companies is necessary for business development, for example, in order to import goods. In accounting, the following postings should be formed:

| Debit | Credit | A comment |

| 57 | 51 | To purchase foreign currency funds are transferred |

| 52 (1-3) | 57 | Foreign currency is credited to the special account |

| 10 | 57 | Reflection of the revaluation of foreign exchange balances (the difference between the rates of the Central Bank and purchases) |

| 91.2 | 57 | Banking commission accounting |

| 51 | 57 | Crediting unused amounts |

In the case when foreign currency is purchased not for carrying out import operations, the following should be recorded in accounting:

Further reflected financial results from the performed operation:

- When the Central Bank rate is less in relation to the purchase rate, the difference (exchange rate) is taken into account as a component of costs:

Dt 91.2 Kt 57

The amount reduces the company's profit.

- Operating income appears provided that the Central Bank quotation exceeds the purchase rate:

Dt 57 Kt 91.1

The company's profit is growing.

Example 1.Mattiola bought $ 4500. The purpose of acquiring foreign currency is to pay employees traveling abroad travel allowances.

The bank received 265.5 thousand RUB.

The bank purchased $ at the rate of 57.3 rubles / dollar. He wrote off a commission for the operation:

(265,500/4500 - 57.3) 4500 \u003d 7,650 rubles.

The revaluation of foreign currency balances should be done as follows:

| Debit | Credit | Amount, thousand rubles | Description |

| 57 | 51 | 265,50 | Money for the purchase of foreign currency is listed |

| 52.1 (2-3) | 57 | 255.60 (4500 56.8) | Crediting the purchased foreign currency to the transit account |

| 91.2 | 57 | 7,650 | Commission of the bank |

| 91.2 | 57 | 2,250 ((57.3-56.8) 4500) | The exchange rate difference is noted |

The company has the right to send the purchased currency to:

- Payment for contracts concluded with foreign counterparties:

Dt 60 Kt 52 (1-3)

- Financing business travel expenses abroad. The currency received by the company at the cash desk is reflected as follows:

Dt 50 Kt 52 (1-3)

- Repayment of loans received in foreign currency:

Dt 66 Kt 52 (1-3)

Important! When buying foreign currency, it is necessary to take into account the resulting exchange rate difference.

Features of revaluation when selling currency

IN modern conditions organizations can sell from 0 to 25% of their foreign exchange earnings to the state. This process is reflected as follows:

Currency balances are revalued on the last day of the reporting period. Possible entries upon receipt:

- profit Dt 91 Kt 99

- loss Dt 99 Kt 91.9

Important! Unrealized proceeds in foreign currency are credited to the account:

Dt 52.1 Kt 52. (1, 2)

Down payments and exchange rate differences

The amounts of advance funds issued or received are subject to accounting at the rate that is current as of the date that corresponds to the moment the money supply is transferred or received.

When, for example, a raw material is bought on account of an advance payment previously paid, it is accounted for at the rate prevailing on the day the advance money was transferred.

Problems in accounting are possible if they are insufficient to fully cover the cost of the supplied raw materials. The value of the purchased product will be formed from two components:

- The advance amount, which is considered in accordance with the quotation on the date of its sending.

- Cost not covered in advance. It is calculated based on the current rate on the day the raw material is accepted for accounting.

The advance listed earlier is not subject to revaluation subsequently.

Features of the calculation in foreign currency for loans and borrowings

Loans received by companies are:

- Short-term (up to 12 months).

- Long-term (more than a year).

In the first case, accounts are used to account for them. 66, 66.21, 66.22, and transactions are reflected as follows:

In accounting for long-term loans in $, €, £, accounts are used. 67, 67.21, 67.22:

Accounting for loans in foreign currency is carried out in a similar way using accounts 66.23 and 67.23.

Calculation of exchange rate differences when buying fixed assets

When a company buys fixed assets, intangible assets in foreign currency under previously concluded contracts, their value is determined either at the rate of the Central Bank, or at another quotation agreed by the parties on the date the assets are included in the accounting. After a while, it is not recalculated.

Only payments due (if any) are subject to revaluation. Then there are exchange rate differences, positive or negative.

Example 2.The company purchased refrigeration equipment for $ 20 thousand. The rate of the Central Bank on the day of purchase: 57.4361. Payment was postponed for a month.

On the last day of the month, you should recalculate the payment debt. The Central Bank's quotation is 57.6587, which is higher than the previous one. The company incurs costs - for a complete settlement, it needs a larger amount of ruble mass in order to settle with the counterparty:

Exchange rate differences in tax accounting

Income received from the translation of foreign currency balances does not relate to profit from the sale of products. It is logical that it is not subject to VAT taxation.

The company carries out revaluation of foreign currency balances depending on the used method of accounting for values.

How exactly fluctuations in the currency quotes are reflected in VAT accounting is shown in the table:

Example No. 3. The goods worth € 12,000 were shipped on November 2 (rate 74.2256), and paid on November 26 (rate 75.1258). VAT at the rate of 18% must be paid in the following amount when using the method:

- accruals 160 327.30 (12 000 74.2 256 0.18)

- cash 162,271.72 (12,000 75.1258 0.18)

Exchange rate differences are taken into account in non-operating income (expenses) exactly as in accounting. This means that when they are positive, they are included in the amount subject to income tax.

Foreign exchange income under the simplified taxation system and OSNO

The simplified people freely open foreign currency accounts for settlements with foreign partners.

With the simplified taxation system, income and expenses in foreign currency are recalculated into RUB at the rate of the Central Bank used on the corresponding dates.

According to the Tax Code, simplified persons are not required to:

- revaluation of foreign currency balances due to changes in quotations;

- to carry out accounting of costs and incomes from such recalculation.

Therefore, unlike companies based on OSNO, for simplified people:

- no amounts arise in the form of positive (or negative) exchange rate differences.

- revenues and costs are set once - on the date of income or expenses.

The explanation of such features is the cash method, which is the basis of the simplified tax system.

Important! Foreign exchange earnings are subject to conversion into RUB at the exchange rate of the Central Bank valid on the day it is included in income. It is credited to a transit (not current) foreign currency account. Advances in foreign currency are included in income in the same way.

The company's expenses incurred due to foreign currency loans and credits include:

- interest that must be paid regularly;

- resulting from the revaluation of accrued %% exchange rate differences;

- minus differences between the quotes of the Central Bank and the domestic market that arise when purchasing foreign currency necessary for the timely execution of loan agreements;

Additional costs associated with the costs of surety agreements, insurance of credit risks, bank guarantees are also included in this list.

Rules for revaluation of foreign exchange balances

In order to revalue currency funds in accordance with the instructions, the following rules should be followed:

- Each transaction in foreign currency carried out with the participation of financial institutions must be entered into the daily balance sheet in rubles.

But for control and analysis, it is allowed to use accounting registers of transactions and software in foreign currency. The Bank provides its clients with bi-currency statements.

- A recalculation is required for all incoming foreign currency account balances. The exceptions are the amount of prepayment for goods (issued or received), advances for services or a set of works performed. To reflect them, you should use the balance accounts for accounting for mutual settlements, which are carried out on transactions with partners.

- In the event that analytical accounts are issued only in foreign currency, the balances of each reconciling balance sheet account are reflected in rubles at the Central Bank exchange rate simultaneously in:

- accounting registers;

- forms of analytical and synthetic accounting.

Popular questions

Question 1. Is included in taxable base for VAT exchange rate difference?

Answer: Exchange rate differences that inevitably appear when translating currency balances are recognized in tax accounting as non-operating income, and not from sales. Therefore, their amount is not included in the VAT base.

Question 2. Do I need to calculate in parallel with the exchange rate differences also the sum differences?

Answer: The concept of amount differences from the Tax Code was excluded back in 2015. All differences arising from the translation of currency balances are considered to be exchange rate differences.

Question 3. When does the exchange rate difference appear?

Answer: It is formed as a result of the revaluation of foreign exchange liabilities and assets at the date:

- Reporting;

- Repayment of the obligation.

Question 4. What is the most common and simplest exchange rate difference?

Answer: This includes the difference arising from the revaluation of foreign currency balances on the company's account.

Question 5. How to recalculate if the value of liabilities or assets is denominated in foreign currency, the rate of which is not provided by the Central Bank?

Answer: The quotation of the Central Bank of US $ to RUB and non-standard currency to the US dollar is used. Data can be taken into account information systemssuch as Bloomberg or Reuters.

During the development of economic ties with foreign companies, domestic entrepreneurs open accounts in foreign currency. Financial workers have to become closely acquainted with what is the revaluation of foreign exchange balances, exchange rate differences, and therefore, be able to correctly reflect them in accounting documents.

An organization may have accounts not only in rubles, but also in the currency of other states. Such accounts are opened when, due to the nature of its activity, the company needs to make settlements with foreign partners, purchase raw materials and materials for foreign currency, import others material values... The law does not impose restrictions on businessmen on opening such accounts.

However, since all financial obligations, as well as tax and accounting in the territory Russian Federation performed exclusively in national currency, due to exchange rate fluctuations, the readings of currency accounts change periodically, and these changes must be monitored and taken into account.

Consider the features of the revaluation of balances in foreign currency accounts of organizations, the subtleties of accounting and tax accounting for this operations.

Purpose of currency settlements

Banking operations with currency provide for the deposit or withdrawal of currency from accounts. These procedures are recorded in bank statements and settlement documents attached to them. It is on the basis of these documents that the accounting of currency funds in the dynamics of the organization's activities takes place.

Why a firm may need a foreign currency account:

- purchase of foreign currency by a resident from a resident (within the limits permitted by law);

- payments in foreign currency;

- currency transactions between a resident and a non-resident (purchase of currency and / or valuable papers, alienation, use as a means of payment);

- crossing of currency values \u200b\u200bof the border of the Russian Federation;

- repayment of a foreign currency loan;

- payment for business trips abroad;

- receipts from an account not opened in the Russian Federation.

The meaning of currency revaluation

It does not matter in the currency of which country the account is opened and transactions are performed. When performing accounting, it is necessary to be guided by the provisions of exclusively Russian legislation. This means that foreign currency for accounting must be recalculated in the ruble equivalent at current rate Of the Central Bank of the Russian Federation.

Thus, revaluation of foreign exchange balances- this is the periodic establishment of the ruble equivalent of currency funds on the organization's account at the rate of the Central Bank of the Russian Federation.

NOTE! The organization should map the rules for making revaluation of currency balances in its accounting policy in the form of an internal regulation.

Possible revaluation results

Due to exchange rate fluctuations, deviations will inevitably occur, which can be calculated by comparing the indicator of the previous revaluation with the last calculation performed. The result obtained in the form of a specific amount may turn out to be:

- positive - the exchange rate difference exceeds the previous indicator, which means that the company has generated additional income (accounting item "Other income");

- negative - due to exchange rate fluctuations, the company has lost a certain share of funds (reflected in "Other costs").

Time frame for revaluation

- on the day when the operation of depositing or withdrawing currency was performed;

- on the day when the accounting report is prepared;

- on the last day of each calendar month.

The exchange rate indicator of the Central Bank of the Russian Federation as of the indicated date is the basis for calculating the revaluation of the foreign currency balance on the organization's account.

Accounting for currency revaluation

To carry out accounting transactions related to currency movement, there is account 52 "Currency accounts", which has 2 sub-accounts for settlements within the country and abroad. Let's consider how the balance is formed for various operations with currency: we recall that they must be reflected exclusively in rubles.

Currency purchase transactions

Organizations can buy foreign currency for various purposes by crediting it to their foreign currency account. Moreover, in accounting entries the following entries will be made:

- debit 57 “Transfers”, credit 51 “Current account” - finance for the purchase of foreign currency is transferred from the organization's account;

- debit 52.1 "Currency accounts", credit 57 "Transfers in transit" - crediting the purchased currency to the company's special account;

- debit 10 "Materials", credit 57 "Transfers in transit" - a reflection of the result of the revaluation of the currency balance on the account (the difference between the exchange rate of the Central Bank of the Russian Federation and the purchase rate), as well as a separate entry - accounting for bank commission;

- debit 51 "Current account", credit 57 "Transfers in transit" - crediting of unused funds.

If the currency is not purchased for import settlements, then the posting is easier:

- debit 57 “Transfers”, credit 51 “Current account” - transfer of money for the purchase of currency;

- debit 52.1 "Currency accounts", credit 57 "Transfers in transit" - crediting funds to the transit account;

- debit 91.2 "Other expenses", credit 51 "Current account" - funds paid to the bank as remuneration.

On the last day of the month, the revaluation of currency balances is reflected:

- in case of profit - on debit 91.9, credit 99;

- in case of loss - on debit 99, credit 91.9.

Transactions when receiving currency from counterparties

If the firm has received currency as payment for goods or services from foreign partners, this money must be credited to the transit account (debit 52.1, credit 62).

IMPORTANT INFORMATION! The organization must sell 50% of the foreign exchange funds received in this way within the country. Violation of this requirement is fraught with a fine in the amount of unrealized currency.

Settlement transactions in currency

Having bought currency, the company can use it for the purposes permitted by law:

- pay obligations under foreign contracts (debit 60, credit 52.1);

- issue foreign travel allowances (debit 50, credit 52.1);

- repay foreign currency loans (debit 66, credit 52.1).

Realization of foreign exchange earnings

As mentioned above, half of the foreign exchange earnings must be sold on the domestic market, if within a week these funds have not gone to settlements with foreign partners. This should be reflected in the balance sheet as follows:

- debit 57, credit 52.1 - direction of foreign exchange funds for sale;

- debit 51, credit 91.1 - crediting the amounts received in foreign currency to the account;

- debit 91.1, credit 57 - writing off the realized currency funds;

- debit 91.2, credit 51 - accounting for sales expenses.

The unrealized part of the foreign exchange earnings is credited to the account by posting: debit 52.1, credit 52.1.2.

Tax accounting of revaluation of foreign currency balances

Even if income was generated as a result of the revaluation, it cannot be recognized as profit from the sale, therefore, it is not entitled to be taxed. It should be taken into account in non-operating income, which will slightly increase income tax and tax payments on the simplified tax system.

In the event of a loss (negative exchange rate difference), these funds must be attributed to non-operating costs, which again will affect income tax. In case of losses for taxpayers of the simplified taxation system, no changes will occur in the tax base (based on the letter of the Ministry of Finance of the Russian Federation dated July 25, 2012).

SO, the importance of accounting and tax accounting for the revaluation of foreign currency balances is due to the possibility of additional profit or loss in the organization at a certain date.

2017-05-20T12: 15: 02 + 00: 00Why do you need " Currency revaluation"? I am often asked this question by novice accountants, because they have not yet come across in practice with foreign exchange transactions and do not understand where this revaluation comes from, how it is calculated and whether it is necessary. Let's deal with this once and for all using the example of 1C: Accounting 8.3, revision 3.0. First, revaluation occurs "by itself" when closing of the month.

Secondly, it arises only for organizations that have had currency transactions.

And that's why.

According to PBU 3/2006 on the accounting of assets and liabilities, the value of which is expressed in foreign currency, we have:

The value of assets and liabilities, expressed in foreign currency, must be recalculated into rubles for reflection in accounting and financial statements.

The translation is performed at the date of the transaction in foreign currency, as well as at the reporting date.

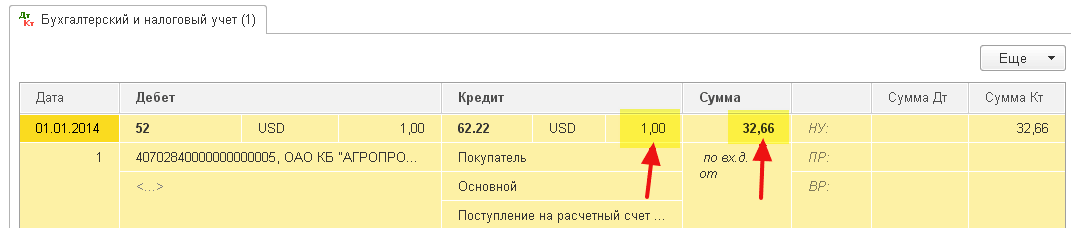

01.01.2014 the buyer transferred to our current account 1 dollar.

The wiring will be as follows:

D52 K62 1 USD (32.6587 rubles)

Please note that we recorded the transaction amount simultaneously in the transaction currency (1 dollar) and in rubles at the exchange rate on the date of the transaction (on January 1, 2014, the dollar exchange rate was exactly 32.6587 rubles).

Turns out that all foreign currency accounts keep their monetary indicators in two dimensions at once: in the account currency and in rubles (the main currency of the regulated accounting for Russia).

Thus, at the end of the day on 01/01/2014, the balance on account 52 will be 1 USD and at the same time 32.6587 rubles.

Everything is fine, but time goes by. The dollar exchange rate is changing. And now at the end of the month (01/31/2014) for one dollar they give 35.2448 rubles.

And, if we look at our 52-account balance at the end of the month, we will see that despite the fact that the rate has changed there is still 1 USD and 32.6587 rubles. But we know that one dollar no longer corresponds to 32.6587 rubles, but 35.2448 rubles! Emerged mismatch between the amount of the balance in dollars and the amount of the balance in rubles.

So, this very recalculation of the value of assets and liabilities in foreign currency into reporting date (that is, monthly) is just invented in order to restore this correspondence between the currency and the rubles every time at the end of the month.

In this case, the revaluation for account 52 as of 01/31/2014 will look like this:

D52 K91.01 2.5861 rubles

Thus, we have revalued the ruble balance on account 52 by 2.5861 rubles from other income. It turns out that the course has grown over this month - hence the income for the organization. If the exchange rate fell, on the contrary, there would be other expenses.

So, after revaluation, the debit balance on account 52 at the end of the day on 01/31/2014 will be 1 USD and at the same time 35.2448 rubles.

But time goes by. And at the end of February for 1 dollar they already give 36.0501 rubles. This means that we again had a discrepancy between dollars and rubles on account 52, and at the same time there was other income due to the increase in the exchange rate for February.

The new revaluation will give the following postings:

D52 K91.01 RUB 0.8053

And the debit balance on account 52 at the end of the day on 02/28/2014 will be the same 1 USD and at the same time 36.0501 rubles.

And so we will overestimate indefinitely, as long as we have a non-zero remainder at 52 counts. Other currency accounts are revalued in the same way.

Here is a brief theory of the revaluation of foreign exchange funds in accounting... Now let's see how this is all implemented in the program using the example of 1C: Accounting 8.3 (revision 3.0):

Loading currency rates for 2014

Setting up a currency account (USD)

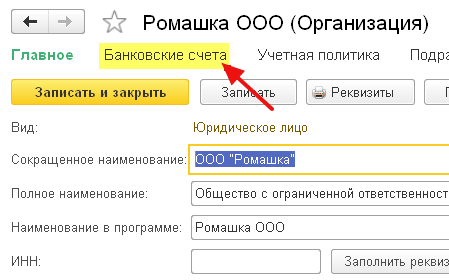

To do this, go to the "Main" -\u003e "Organizations" section and open our organization there ():

In the organization card in the top panel, select the "Bank accounts" item:

In the opened list of accounts, click the "Create" button and fill out the current account card as follows (account number and BIC are indicated as an example; be sure to select the account currency USD):

Click "Save and Close".

We make a receipt of funds from the buyer

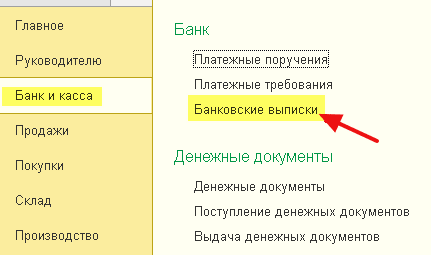

To do this, go to the "Bank and Cashier" section and select the "Bank statements" item () there:

Click the "Receipt" button and fill out the bank statement as follows (receipt of $ 01 01/01/2014; from any counterparty under any agreement; accounting account - 52; bank account - the one that we just created):

Click "Post and Close".

We look at the document transactions (the DtKt button in the statement journal):

We see that 1 dollar was capitalized on account 52 at the rate as of 01/01/2014 (about how to view exchange rates for a specific date in 1C: Accounting).

Closing the month for January

Go to the "Operations" section and select the "Close of the month" item () there:

Select the period January 2014 and click "Perform month closing".

Then we find the item "Revaluation of foreign exchange funds", click on it and select "Show transactions":

Here is our exchange rate difference of 2.58 rubles:

Let's go back to the close of the month for January 2014 and find the button "Help-calculations" there. Click it and select the item "Revaluation of foreign exchange funds":

The program will generate a report with calculations for the revaluation of foreign exchange funds:

Do the month close for February in the same way to make sure our estimates match the behavior of the program.

We are great, that's all

If this does not help, then it is very likely that the account on which you expect the calculation of the exchange rate difference is entered in your list of accounts with a special revaluation procedure.

- The Central Bank told about the new tariffs of the civil liability insurance What's new in the civil liability insurance from June 1

- What is sleep and who uses it What does sleep mean income

- Debit cards of "Sberbank of Russia": what does this concept mean, how to use, an overview of the offered by the bank

- Simplified taxation system What does it mean in accounting usn