Accounting for a leasing agreement in 1s 8.3. Accounting info

Your company has already entered into a lease agreement and you have questions about how to reflect the lease in the accounting? In this article you can find the necessary information and examples accounting entries for various leasing transactions.

Accounting for transactions under a leasing agreement is regulated by Order of the Ministry of Finance of the Russian Federation No. 15 dated February 17, 1997.

Leasing entries depend on whose balance sheet reflects the leased property: the lessor or the lessee. The party on whose balance sheet the leased property is recorded must be specified in the lease agreement.

Accounting for leasing when reflecting property on the balance sheet of the lessor

payment schedule .

If the lease agreement provides for the reflection of the leased asset on the balance sheet of the lessor, the lessee shall reflect the leased property on the off-balance account 001 "Leased fixed assets".

The accrual of lease payments is reflected in the credit of account 76 "Settlements with different debtors and creditors" in correspondence with cost accounting accounts: 20, 23, 25, 26, 29 - when accounting for lease payments for property used in production activities, 44 - for property used in the activities of a trade organization, 91.2 - for property that used for non-production purposes.Further, for simplicity, in the examples of accounting for leasing, only postings for account 20 will be given.

Dt 001 - 1 000 000(accepted for accounting the subject of leasing at a cost without VAT)

Dt 60 - Kt 51 - 236 000(paid advance payment(initial payment) under a leasing agreement)

It should be borne in mind that the attribution to the costs of an advance under a leasing agreement (advance offset) may not be made immediately, but throughout the entire agreement. In the above payment schedule, the advance payment under the agreement is offset evenly (by 6,555.56 rubles) within 36 months.

Dt 20 - Kt 76 - 29 276.27(lease payment No. 1 accrued - 34,546 minus VAT - 5,269.73)

Dt 19 - Kt 76 - 5,269.73(VAT accrued on lease payment No. 1)

Dt 20 - Kt 60 - 5 555.56(part of the advance payment under the leasing agreement was offset - 6,555.56 minus VAT 1,000)

Dt 19 – Kt 60 – 1,000(VAT accrued on advance payment)

Dt 68 - Kt 19 - 6,269.73(VAT is presented to the budget)

Dt 76 - Kt 51 - 34 546(leasing payment No. 1 is listed)

The commission that is paid at the beginning of the leasing transaction (commission for the conclusion of the transaction) is attributed in accounting to the same expense accounts as the current leasing payments.

Postings for the repurchase of the subject of leasing

If there is a redemption price in the leasing agreement (this amount is absent in the given lease payment schedule, for example, let's take it equal to 1,180 rubles with VAT), the following entries are made in accounting:

Dt 08 – Kt 76 – 1 000(reflected are the costs of repurchasing the leased asset upon transfer of ownership to the lessee)

Dt 19 - Kt 76 - 180(VAT accrued upon redemption of the leased asset)

Dt 68 - Kt 19 - 180(VAT is presented to the budget)

Dt 76 - Kt 51 - 1 180(the amount of repurchase of the leased asset has been paid)

Dt 01 – Ct 08 – 1 000(accepted for accounting the subject of leasing as part of own fixed assets)

Accounting for leasing when reflecting property on the balance sheet of the lessee

The legislation governing the accounting of leasing does not contain unambiguous instructions on recording transactions under a leasing agreement if the lessee is the balance holder of the property.

At present, there is a practice of communication between lessees and leasing companies with auditors and inspection bodies, and a certain scheme of leasing transactions was formed.

Accounting for leasing when reflecting property on the balance sheet of the lessee

If, under the terms of the lease agreement, the property is recorded on the lessee's balance sheet, upon receipt of the leased asset in the lessee's accounting, the value of the property, net of VAT, is reflected in the debit of account 08 "Investments in non-current assets" in correspondence with the credit of account 76 "Settlements with various debtors and creditors".

When the subject of leasing is accepted for accounting as fixed assets, its value is debited from credit 08 of account to debit 01 of account "Fixed Assets".

The accrual of lease payments is reflected in the debit of account 76, subaccount, for example, "Settlements with the lessor" in correspondence with account 76, subaccount, for example, "Calculations on lease payments".

Depreciation on the subject of leasing is made by the lessee. The amount of depreciation of the leased asset is recognized as expenses for ordinary species activities and is reflected in the debit of account 20 "Main production" in correspondence with the credit of account 02 "Depreciation of fixed assets, depreciation sub-account of leased property.

Tax accounting for leasing when reflecting property on the balance sheet of the lessee

In the tax accounting of the lessee, the leased property is recognized as depreciable property.

The initial cost of the leased asset is determined as the amount of the lessor's expenses for its acquisition.

For income tax purposes monthly amount depreciation is determined based on the product of the initial cost of the leased asset and the depreciation rate, which is determined based on the term beneficial use leased property (taking into account the classification of fixed assets included in depreciation groups). In this case, the lessee has the right to apply to the depreciation rate increasing the coefficient up to 3. The specific size of the multiplying factor is determined by the lessee in the range from 1 to 3. This coefficient does not apply to leased property belonging to the first or third depreciation groups.

Leasing payments minus the amount of depreciation on leased property are included in the costs associated with production and sale.

An example of accounting for leasing when reflecting property on the balance sheet of the lessee

Leasing transactions correspond to the property lease payment schedule located at the link

The lessee received a car under a leasing agreement, payment schedule parameters:

- term of the lease agreement – 3 years (36 months)

- total amount payments under the leasing agreement - 1,479,655.10 rubles, incl. VAT - 225,710.10 rubles

- advance payment (down payment) - 20%, 236,000 rubles, incl. VAT - 36,000 rubles

- car cost - 1,180,000 rubles, incl. VAT - 180,000 rubles

The estimated period of use of the leased property is four years (48 months). The car belongs to the third depreciation group(property with a useful life of 3 to 5 years). Depreciation is charged linear way.

Determine the amount of monthly depreciation in accounting. Because the value of the property (including the remuneration of the leasing company) is 1,253,945 rubles (1,479,655.10 - 225,710.10), the monthly depreciation will be 1,253,945: 48 = 26,123.85 rubles.

A passenger car belongs to the third depreciation group, therefore, in tax accounting a period of 48 months may be set. The monthly depreciation rate is 2.0833% (1: 48 months x 100%), the monthly depreciation amount is 1,000,000 x 2.0833% = 20,833.33 rubles.

In accordance with subparagraph 10 of paragraph 1 of article 264 of the Tax Code of the Russian Federation, the amount of the lease payment, monthly recognized as expenses for profit tax purposes, is 8,442.94 rubles (34,546 (leasing payment) - 5,269.73 (VAT as part of the lease payment) – 20,833.33 (monthly depreciation in tax accounting)).

The expense under the leasing agreement is formed monthly in accounting at the expense of depreciation (26,123.85 rubles), in tax accounting - at the expense of depreciation (20,833.33 rubles) and leasing payment (8,442.94 rubles), totaling 29,276 .27 rubles.

Because in accounting, the amount of expenses for 36 months (the term of the lease agreement) is less than in tax accounting, this leads to taxable temporary differences and deferred tax liabilities.

During the term of the leasing agreement, the lessee has a monthly taxable temporary difference in the amount of 3,152.42 rubles (29,276.27 - 26,123.85) and a corresponding deferred tax liability arises in the amount of 630.48 rubles (3,152.42 x 20% ).

Separately, it is necessary to say about advance payment ( down payment under contract). The following situations are possible:

1. When transferring property for leasing, the lessor provides an invoice for the full amount of the advance(in the given schedule of leasing payments - by 236,000 rubles). In this case, the entire amount of the advance payment of the advance payment, net of VAT, is recognized in tax accounting as expenses for profit tax purposes.

I would like to note that within the framework of a leasing agreement, services are provided throughout the entire agreement and the fiscal authorities have no reason to assess compliance with the criteria of paragraph 4, paragraph 2, Article 40 of the Tax Code of the Russian Federation on the comparability of leasing payments, because individual payments cannot be considered as separate transactions, and the price under the leasing agreement must be analyzed in aggregate for all payments of the agreement.

2. The advance payment under the leasing agreement shall be set off in equal installments during the entire leasing period. In this case, the creditable part of the advance payment is recognized as expenses in tax accounting for the purposes of taxation of profit.

In the given example of the lease payment schedule, it is assumed that the advance invoice is issued to the lessee when the property is leased, i.e. in tax accounting when transferring property to leasing, expenses in the amount of 200,000 rubles are reflected (advance payment, which is a leasing payment, depreciation is not deducted, because in the first month when transferring property to leasing, it is not yet accrued). This simultaneously creates a taxable temporary difference in the amount of 200,000 rubles and a corresponding deferred tax liability in the amount of 40,000 rubles (200,000 rubles x 20%).

At the end of the lease agreement, the lessee will continue to accrue depreciation monthly in accounting in the amount of 26,123.85 rubles. There will be no tax expense. This will result in a monthly decrease in deferred tax liabilities in the amount of RUB 5,224.77 (RUB 26,123.85 x 20%).

Thus, according to the results of the agreement, the total amount of deferred tax liabilities will be equal to zero:

40,000 (deferred tax liability on advance payment) + 22,697 (630.48 x 36 - deferred tax liability on current lease payments) - 62,697 (5,224.77 x 12 - reduction of deferred tax liabilities for 12 months of depreciation in accounting accounting after the end of the lease agreement).

Transactions upon receipt of the object of leasing

Dt 60 - Kt 51 - 236 000(advance paid under the lease agreement)

Dt 08 - Kt 76 (Settlements with the lessor) - 1,253,945(reflected the debt under the leasing agreement without VAT)

Dt 19 - Kt 76 (Settlements with the lessor) - 225,710.10(reflected VAT under the lease agreement)

Dt 01 – Ct 08 – 1 253 945(a car received under a leasing agreement is accepted for accounting)

Dt 76 - Kt 60 - 236 000(advance paid at the conclusion of the lease agreement)

Dt 68 (Income tax) - Kt 77 - 40,000

Dt 68 (VAT) - Ct 19 - 36,000(VAT is presented on advance payment)

Postings on current lease payments

Dt 20 - Kt 02 - 26 123.85

Dt 76 (Settlements with the lessor) - Kt 76 (Settlements on lease payments) - 34,546(reduced debt on leasing by the amount of the lease payment)

Dt 76 "Settlements for lease payments" - Kt 51 - 34,546(lease payment listed)

Dt 68 (VAT) - Kt 19 - 5,269.73(VAT is presented on the current lease payment)

Dt 68 (Income tax) - Kt 77 - 630.48(reflected deferred tax liability)

Postings at the end of the lease agreement

Dt 01 (Own fixed assets) – Kt 01 (Fixed assets received under leasing) – 1,253,945(reflected the receipt of the car in the property)

Dt 02 (Depreciation of leasing property) - Kt 02 (Depreciation of own fixed assets) - 940,458.60(reflected accrued depreciation on the car)

Postings within 12 months after the end of the lease agreement

Dt 20 - Kt 02 (Depreciation of own fixed assets) - 26,123.85(depreciation accrued on the car)

Dt 77 - Kt 68 (Income tax) - 5,224.77(reflecting a decrease in deferred tax liability)

There is also a method in which the initial cost of the leased asset in accounting is equal to the cost of purchasing a car from the lessor, i.e. matches the value in the tax accounting. In this case, on account 76, when the property is accepted for accounting, only the debt at the cost of the property is reflected.

The accrual of lease payments is carried out monthly on the credit of account 20 in correspondence with account 76 in the amount of the difference between the accrued depreciation and the amount of the monthly lease payment.

Choosing the most reasonable option for reflecting leased property on the balance sheet of the lessor or lessee, as well as agreeing with the leasing company on the optimal scheme for reflecting lease payments, is a very difficult task that requires good knowledge specifics of accounting leasing operations and features of wording in the leasing agreement and primary documents.

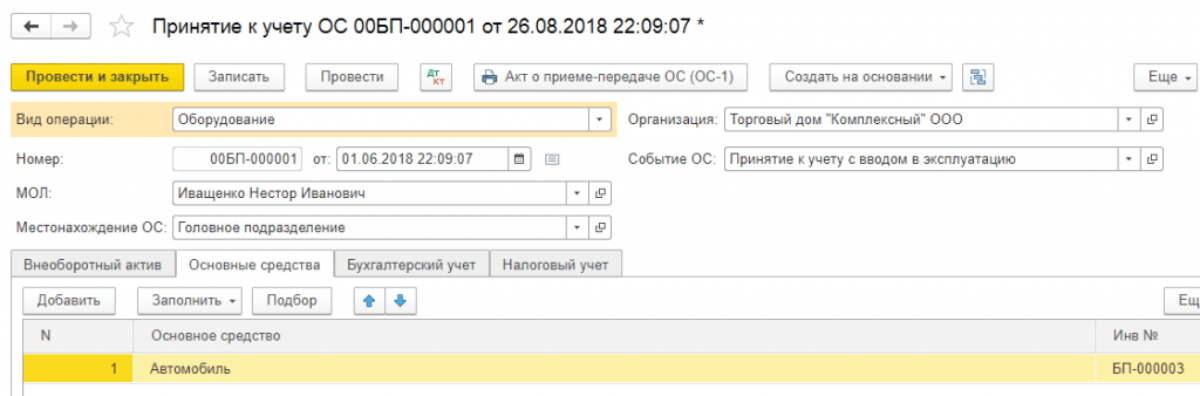

To do this, in the same section, select "Acceptance for OS accounting". Click the "Create" button and fill out the document:

- indicate that we accept the equipment for accounting with commissioning;

- indicate the materially responsible person (MOL);

- indicate the location of the main asset.

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on new version 1C ZUP 3.0;

- A good course on 1C Trade Management 11.

- type of operation - equipment;

- method of receipt - under a leasing agreement;

- then select the counterparty, contract and equipment from the "Nomenclature" directory.

On the "Fixed Assets" tab, we indicate the property already from the "Fixed Assets" directory.

Accounting for leasing on the balance sheet of the lessee in 1s 8.3 and an example of postings

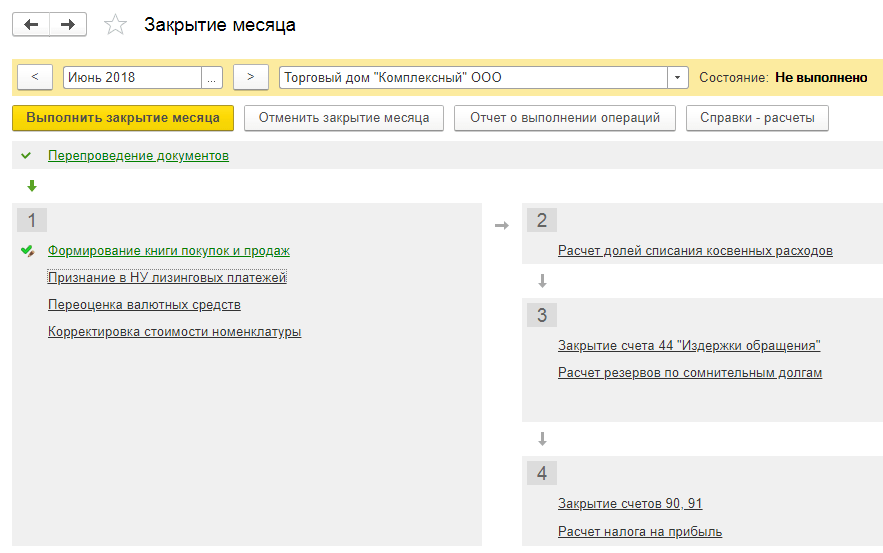

Depreciation calculation Calculation of depreciation in 1C for a leasing object must be registered only if the object is defined on the lessee's balance sheet. Depreciation, as well as recognition in NU of lease payments in 1C 8.3, are formed by the routine operation Depreciation and depreciation of fixed assets, and also by the operation Recognition of lease payments in NU at the end of the month, respectively (Operations - Closing of the month): Important! Depreciation is charged in the next month after acceptance for accounting. Operation movements Depreciation and depreciation of fixed assets: Recognition in tax accounting of leasing payments: The depreciation statement can be formed in the fixed assets and intangible assets tabs - hereinafter the Fixed assets depreciation statement: Step 5.

The status of settlements with the lessor The status of settlements with the lessor in 1C 8.3 can be viewed using the Account Analysis report.

Leasing in "1s: accounting 8"

In fact, this is a fixed asset card. Information for depreciation is located on the "Accounting" tab. Here we fill in the following fields:

- account: 01.03

- accounting procedure: depreciation

- Next, we indicate in what order depreciation will be charged

This example is filled out as follows: On the tab "Tax accounting", as a rule, the same parameters are indicated. Now the document can be posted. It should be noted that the data entered when the fixed asset was taken into account are automatically reflected in its card: How to reflect the monthly lease payment The lease payment in the program is reflected in the receipt document in the "Purchases" menu.

Accounting for leasing at the lessee

Important

The tabular part can be filled in using the Fill button: In the Accounting section, fixed assets accounting accounts are set. In the Tax Accounting section, the procedure for including the redemption price and accrual parameters are set: In the movements of the document Redemption of the object of leasing, the redemption of property, as well as depreciation and transfer of ownership rights, are reflected. Do not forget to register the invoice received using the Register button.

At our master class “Rent and Leasing: the complexities of accounting and taxation” you can study this topic in more detail. Including the position of the lessee is considered:

- The property is recorded on the balance sheet of the lessee in 1C.

Accounting for leasing on the balance sheet of the lessee in 1s 8.3 step by step

In this article, we will consider an example where a third-party organization (lessor) acquires ownership of a Steepline 4SL03 CNC lathe and transfers it to us for use for a long time. During this period, we will pay the lessor this cost together with interest. At the end of the term, the machine will become our property.

Content

- 1 Leasing

- 2 Accounting for a fixed asset

- 3 Monthly lease payments

- 4 Equipment depreciation

Leasing First of all, we need to reflect in the program the receipt of the Steepline 4SL03 CNC lathe, which the lessor purchases for us. This operation must be performed through the document "Receipt in leasing". You can find it in the "OS and NMA" menu.

Accounting info

On the first tab of the document, we indicate the method of receipt of fixed assets - under a leasing agreement. As the equipment itself, we will choose our Steepline 4SL03 CNC machine. The division and warehouse are also indicated here. The account in our example will be 08.04.2.

On the next tab - equipment, it is enough to indicate the main tool itself, which is located in the directory of the same name. Inv. number will be set automatically. We will not describe in detail the creation of filling in the OS directory. You shouldn't have any problems with this. Next, let's move on to the next tab - "Accounting".

Correctly filling in the data contained on it is very important, because you will set up not only the BU, but also how depreciation will be calculated. Account in our case 01.03. We also indicated that we will accrue depreciation in a linear way (in equal installments). Depreciation will take place on account 02.03.

How to reflect leasing in 1s 8.3 with the lessee

Payment of advance payments The client-bank is not used. A payment order in 1C 8.3 is created in the tabs Bank and cash desk - further Money orders and on the basis of it we register the document Write-off from the current account in 1C. On the payment order:

- The type of operation must be specified Payment to the supplier;

- The amount is indicated in full with the redemption price. The distribution of this amount will be in postings 1C;

- Check the Paid checkbox;

- Write-off from the current account is registered using the Enter the document write-off from the current account:

- The object is defined on the lessor's balance sheet - 05;

- The object is defined on the lessee's balance sheet - 07.2.

Set the Debt repayment to By document.

Accounting for leasing in 1s 8.3 on the balance sheet of the lessee - postings and examples

Attention

How to make operations with leasing in the program 1C 8.3 Accounting? Consider an example of accounting for leasing in 1C Accounting 8.3, when fixed assets are on the balance sheet of the lessee. Receipt in leasing equipment First, let's do the receipt of property. Let's go to the menu "Fundamental Property and Intangible Assets", then in the "Receipt of Fixed Assets" section, select "Receipt in Leasing".

To create a new document, click the "Create" button in the window that opens. A new document window will open. First, let's fill in the header of the document. Let's put it there:

- organization

- counterparty

- contract with a counterparty

- the settlement account is indicated 76.07.1

We will indicate what equipment we receive, quantity and price.

In the latest releases of 1C 8.3, the “Leasing Service” operation was added to it: An example of postings for leasing services in 1C Accounting looks like this: Also in the 1C 8.3 program, in the “OS and Intangible Assets” section, a document has appeared that allows you to change the reflection of expenses on leasing payments : Calculation of depreciation of equipment In our case, the equipment is on the balance sheet of our company, so the decrease in its initial cost occurs due to depreciation. Depreciation in 1C is calculated at the end of the month by the routine procedure "Closing the month". Do not forget to restore the sequence of documents before performing the operation (repost them since the last corrected document).

Receipt of equipment in leasing in 1s 8 3 on the balance of the lessor

In the latest releases of 1C 8.3, the “Leasing Service” operation was added to it: An example of postings for leasing services in 1C Accounting looks like this: payments: Calculation of equipment depreciation In this case, the equipment is on the balance sheet of our company, so the decrease in its initial cost occurs due to depreciation. Depreciation in 1C is calculated at the end of the month by the routine procedure "Closing the month". Do not forget to restore the sequence of documents before performing the operation (repost them since the last corrected document).

The concept of leasing appeared in our country relatively recently. This is a kind of lending to an enterprise when it purchases fixed assets. The objects of leasing can be: equipment, facilities, enterprises, transport, etc. In fact, leasing is a long-term lease of property with the subsequent acquisition of its ownership.

Purchase on lease and registration

In order to account for leasing on the lessee's balance sheet, the 1C 8.3 program provides for a special document "Receipt in leasing", which can be found in "OS and NMA-Receipt of OS".

Fig.1

Inside the document, we draw attention to the fact that the accounting account is 76.07.1. We will also enter data on the purchased equipment into the tabular part. We indicate the accounting account 08.04.2 * - "Acquisition of OS".

*Does not work on account 08.04.2 release 3.0.66.60.

Fig.2

We carry it out and check the accounting entries.

- In the type of operation - equipment (in our example);

- Number / date - fill in the date, the number is entered automatically;

- MOL (responsible person) - we select and appoint an employee of the organization;

- In the location, indicate where the equipment will be used;

- OS event - in accordance with our task, we indicate what will be registered and put into operation.

After that, we fill in the tabs that are below, the first of them is Non-current asset. We fill in the following information:

- under a lease agreement;

- Counterparty - lessor;

- Agreement – we indicate our leasing agreement;

- Equipment is the subject of leasing;

- Warehouse – specify the warehouse where our equipment will be stored;

- The account with us is 08.04.2 “Purchase of OS”.

Fig.4

The OS tab is filled from the directory of the same name, where we must create a new position. Press "+" and proceed to filling out the directory.

Fig.5

Fill in the following fields in the opened form:

- Accounting group - vehicles;

- Name - we have "Car";

- Included in the group - OS.

Fig.6

Click "Save and Close". New position appeared in the directory, so feel free to continue filling in the tab by selecting our new fixed asset from the list, inventory number assigned automatically.

Fig.7

Filling in data for accounting purposes is carried out in the tab of the same name for the following fields:

- Account - 01.03 Leased property;

- Order - from the list "Depreciation";

- Method - Linear;

- In the accrual account, we put 02.03 "Depreciation of leased property";

- In the display of expenses, we set the debit of which account the depreciation will be reflected. We have - 20.01 "OS".

- In the term, we indicate how many years we plan to depreciate this equipment, in our example 10 years x 12 months, we get 120 months.

Fig.8

On the next tab, fill in the data for the tax in the following fields:

- In order of inclusion in the composition of expenses - Accrual of depreciation;

- Initial cost - indicates the amount of expenses without VAT of the lessor for the purchase of equipment. This information can be found in the lease agreement;

- In the way of displaying the costs of leasing payments, we set "Depreciation" (account 20.01);

- Monthly - 10 years x 12 months. That is, it turns out that the equipment is planned to be depreciated for 120 months.

Fig.9

We post the document and with the DtKt button we control the postings: Dt 01 - Kt 08 “The OS object is accepted for accounting”.

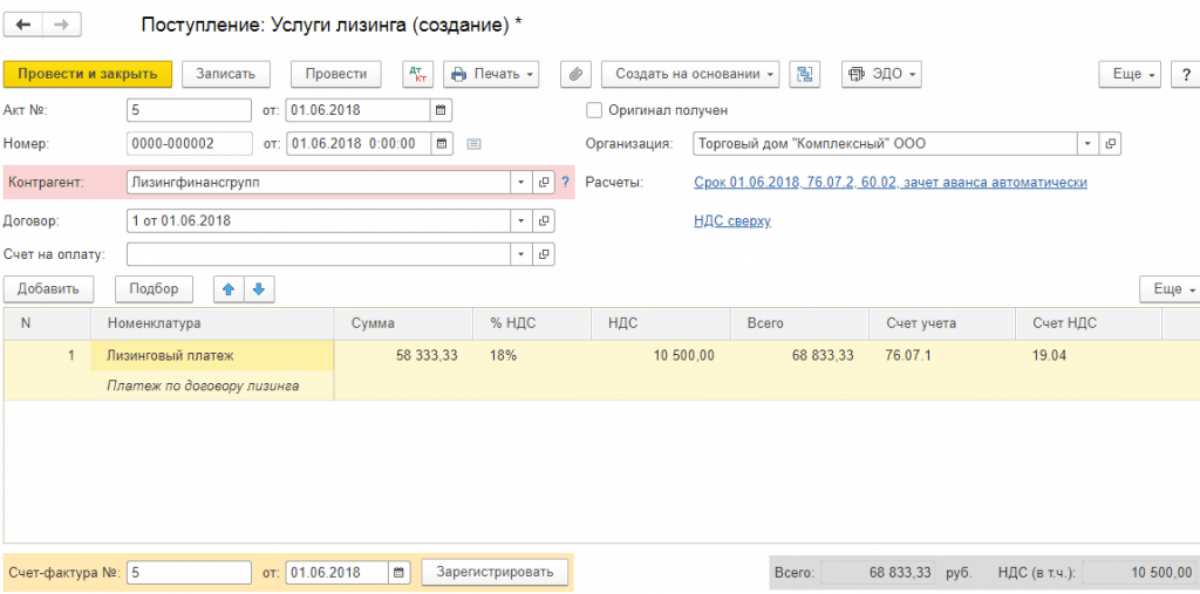

The lessor will issue a monthly invoice for leasing services. To reflect these services in the 1C 8.3 program, "Receipt (acts, invoices)" is used, which is located in the "Purchases" menu.

Fig.10

When creating a receipt, indicate "Leasing Services".

Fig.11

We begin to fill out the document, be sure to indicate the number and date of the act received from the lessor, the details of the leasing agreement, as well as the organizations of the lessor and the lessee. In the "Nomenclature" we indicate the "Leasing payment", in the "Amount" - the amount from the act (invoice) of the lessor. Fill in the number and date of the invoice, click the "Register" button.

Fig.12

Also, please note that our account for accounting for settlements with the counterparty is 76.07.2, and for advances - 60.02.

Fig.13

These receipts are filled, select Post. Entries on expenses for leasing services are formed in accounting records and accounting records. We press DtKt and check the generated wiring.

Fig.14

In accounting, leasing payments are not included in expenses, but are accounted for as a debit 76.07.1 Lease obligations. The cost of leased equipment is taken into account under the credit of this account. Thus, after making all lease payments under the lease agreement, account 76.07.1 will be closed.

Although the equipment acquired on lease is not the property of the organization, it still needs to be registered and depreciated accordingly. This is done through routine operation closing of the month in "Operations - Closing the period".

Fig.15

In conclusion, it is important to pay attention to the fact that for leasing operations there is a difference between accounting and tax accounting, since in the latter, leasing costs are taken into account minus tax depreciation. The 1C 8.3 program will automatically calculate depreciation and leasing costs, and also reflect the difference between accounting and tax accounting. To do this, in 1C 8.3 you need to correctly compose Accounting policy enterprises.

Consider an example of accounting for leasing in 1C Accounting 8.3, when fixed assets are on the balance sheet of the lessee.

Let's do the property acquisition first. Let's go to the "OS and intangible assets" menu, then in the "" section, select "Leasing". To create a new document, click the "Create" button in the window that opens. A new document window will open.

First, let's fill in the header of the document. Let's put it there:

- organization;

- counterparty;

- contract with a counterparty;

- the account of settlements is indicated 76.07.1 .

Upon receipt of 1C 8.3 on the balance of the lessee, we make the following entries:

Registration of equipment and other property

After you have created the receipt of fixed assets, you need to take them into account. To do this, in the same section, select "".

Click the "Create" button and fill out the document:

- indicate that we accept equipment for accounting with;

- indicate the materially responsible person (MOL);

- indicate the location of the main asset.

Get 267 1C video lessons for free:

- type of operation - equipment;

- method of receipt - under a leasing agreement;

- then select the counterparty, contract and equipment from the "Nomenclature" directory.

On the "Fixed Assets" tab, we indicate the property already from the "Fixed Assets" directory. In fact, this is a fixed asset card.

Information for depreciation is located on the "Accounting" tab. Here we fill in the following fields:

- accounting account: 01.03;

- accounting procedure: ;

- Next, we indicate in what order depreciation will be charged.

I have it filled out like this:

On the tab "Tax accounting", as a rule, the same parameters are indicated.

Now the document can be posted. It should be noted that the data entered when accepting a fixed asset for accounting is automatically reflected in its card:

How to reflect the monthly lease payment

The leasing payment in the program is reflected in the receipt document in the "Purchases" menu. In the latest releases of 1C 8.3, the Leasing Service operation has been added to it:

An example of postings for leasing services in 1C Accounting looks like this:

Consider an example of accounting for leasing in 1C Accounting 8.3, when fixed assets are on the balance sheet of the lessee. Receipt in leasing equipment First, let's do the receipt of property. Let's go to the menu "Fundamental Property and Intangible Assets", then in the "Receipt of Fixed Assets" section, select "Receipt in Leasing". To create a new document, click the "Create" button in the window that opens. A new document window will open. First, let's fill in the header of the document. Let's put it there:

- organization;

- counterparty;

- contract with a counterparty;

- we indicate the settlement account on 76.07.1.

Next, fill in the "Equipment" tab. We will indicate what equipment we receive, quantity and price. Upon receipt of 1C 8.3 on the balance of the lessee, we make the following entries: Registration of equipment and other property After you have created the receipt of fixed assets, you must take them into account.

If you need to change the reflection of the costs of lease payments, or make adjustments to the accounting for depreciation, you can use the document "Parameters of fixed assets depreciation" from the menu "Intangible assets and intangible assets". Select the appropriate type of operation when creating a new document, depending on what goals you are pursuing.

Depreciation of equipment Despite the fact that the equipment was purchased on lease and does not yet belong to us, we still registered it with our company. In this regard, depreciation will be charged at the close of the month (monthly in this example).

This procedure is standard and in case of difficulties, you can refer to our other article, where everything is described in detail.

Accounting for leasing at the lessee

Closing of the month: Amortization and Recognition of Leasing Payments in Tax Accounting MENU: Operations \ Closing of the period \ Closing of the month. We are just holding the Closing of the month of MARCH 2015. Nothing special will happen.

Depreciation will begin to accrue only from next month after the asset is put into operation. Leasing payments will also begin to accrue from next month.

Everything will be only in April 2015. Therefore, we are holding the Closing of the Month of April 2015. And now the first depreciation calculation appears: The posting correspondence is clear.

Where did these numbers come from? By accounting our fixed asset "village" on 01 account in the amount of 3,240,000 rubles (document Acceptance for accounting of fixed assets). The useful life in accounting is 6 years = 72 months.

This means depreciation in accounting for one month: 3,240,000/72 = 45,000 rubles.

Posting of leased property to account 001

Important

Bookmark "Non-current asset": Here the main thing in the field "Receipt method" is to select the option "Under a leasing agreement"! This value was introduced into the program specifically to automate leasing operations. Previously, there was no such Method of OS Receipt in the program.

Attention

After selecting “Method of receipt” = “Under a leasing agreement”, the details “Counterparty” and “Agreement” will become available on the document form, which must also be filled out. We fill them with the data of our lessor. The remaining fields are filled in as usual.

Bookmark "Fixed assets": There is nothing special to note here. But just in case, you never know, we recall that when we create a new Main Tool (we call it “ Vehicle Received in Leasing (Subject of Leasing)”), then we fill in its data to the minimum.

Because the basic data for filling out the fixed asset card is taken from the document Taking into account fixed assets.

Accounting for leasing on the balance sheet of the lessee in 1s 8.3 and an example of postings

According to tax accounting, our fixed asset "village" on account 01 in the amount of 2,500,000 rubles (document Acceptance for accounting of fixed assets). The useful life in tax accounting is 6 years = 72 months. This means depreciation in tax accounting for one month: 2,500,000/72 = 34,722.22 (2) rubles. But we also have an increasing special coefficient of 3 - the object of leasing is depreciated very quickly for the purposes of tax accounting (document Acceptance for accounting of fixed assets \ tab Tax accounting).

depreciation in tax accounting for one month: (2,500,000 / 72) * 3 = 104,166.67 rubles.

Which actually reflected in our tax accounting posting. But in addition to depreciation, in the Closing of the Month we have the operation "Recognition at NU of Leasing Payments".

And the entries for this operation are as follows: The text in the Contents of the entry reads as: "Adjustment of depreciation costs by the amount of excess over lease payments."

Leasing in "1s: accounting 8"

Depreciation in tax accounting is more than the monthly lease payment! And here the question arises: how do you order to understand Tax code RF?! If the depreciation were less than our monthly lease payment, what would be our NU expenses? First, depreciation. Secondly, the monthly lease payment minus depreciation. We add these two amounts: depreciation + monthly lease payment - depreciation = monthly lease payment. That is, the amount of the monthly lease payment would have gone into our expenses! But we have more depreciation than the monthly lease payment.

Why don't we take into account the entire amount of depreciation in expenses - after all, it is more than a monthly lease payment. And by the way, in ConsultantPlus, in the situation we are considering, this is exactly what is done.

And it's not bad: more amount expenses - less profit - less taxes.

How to conduct accounting of fixed assets (leasing) part 1 in 1s

In the "Settlements" attribute, the account for accounting for debts on lease payments is indicated - 76.07.2 (76.27.2, 76.37.2) 76.37.1) We remember that on account 76.07.1 - we hold the sum of all our rental obligations - A BIG AMOUNT! On account 76.07.2 - we take into account the debt on current lease (usually monthly) payments. This is a small amount if we pay it strictly according to the lease payment schedule, without delay.

Everything is filled almost automatically. It is only necessary to indicate the Number and date of the Act on lease payments. And do not forget to register the invoice at the bottom of the Goods and Services Receipt document.

Accounting for leasing on the balance sheet of the lessee in 1s 8.3 step by step

It turns out an interesting thing: all depreciation deductions are, as it were, the cost of the leased asset; all leasing payments are also the amount in the area of the cost of the leased asset. Depreciation charges are written off as expenses. If lease payments are also fully written off as expenses, then it turns out that we will write off almost twice the cost of the leased asset as expenses.

You can't live like this! Therefore, the lease payment is reduced by the amount depreciation charges. Then everything is fair: depreciation and lease payments in excess of the depreciation amount are taken as expenses.

Our monthly lease payment is 94,400 rubles, including VAT 14,400 rubles. That is, the monthly lease payment without VAT = 80,000 rubles. The amount of depreciation for tax accounting with us: 104,166.67 rubles.

On the first tab of the document, we indicate the method of receipt of fixed assets - under a leasing agreement. As the equipment itself, we will choose our Steepline 4SL03 CNC machine.

The division and warehouse are also indicated here. The account in our example will be 08.04.2. On the next tab - equipment, it is enough to indicate the main tool itself, which is located in the directory of the same name.

Inv. number will be set automatically. We will not describe in detail the creation of filling in the OS directory. You shouldn't have any problems with this. Next, let's move on to the next tab - "Accounting". Correctly filling in the data contained on it is very important, because you will set up not only the BU, but also how depreciation will be calculated. Account in our case 01.03. We also indicated that we will accrue depreciation in a linear way (in equal installments). Depreciation will take place on account 02.03.

How to register 001 account leasing equipment in 1s

You must specify original cost for purposes tax accounting, which is equal to the amount of expenses of the LESSOR (namely, the lessor, that is, that other party - not us!) for the acquisition of the leased asset. "Method of reflecting the costs of lease payments." As we remember, this is an account and analytics where expenses are written off. In this case, for the purposes of NU. We called the “Method of reflecting expenses on lease payments” “Lease payments”. From the inside, it looks like this: Bookmark " Depreciation premium”: We did not touch it in our example. Therefore, we will not look at it. The postings of the document "Acceptance for accounting of fixed assets" will be as follows: Let's comment on these postings.

To do this, in the same section, select "Acceptance for OS accounting". Click the "Create" button and fill out the document:

- indicate that we accept the equipment for accounting with commissioning;

- indicate the materially responsible person (MOL);

- indicate the location of the main asset.

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on the new version of 1C ZUP 3.0;

- A good course on 1C Trade Management 11.

- type of operation - equipment;

- method of receipt - under a leasing agreement;

- then select the counterparty, contract and equipment from the "Nomenclature" directory.

On the "Fixed Assets" tab, we indicate the property already from the "Fixed Assets" directory.

Posting of leased property to account 001 Good afternoon! I ask for help, I ran into a question, simple at first glance - at what cost to receive a leasing car on account 001, with or without VAT. normative documents There is no direct answer, the explanations in the literature contradict each other. We are the lessee, the car is on the lessor's balance sheet. Quote: Hello. The subject of leasing is reflected at the cost specified in the agreement

It is logical to accept in the amount indicated in this document, that is, in accordance with the leasing agreement itself. A similar position is contained in the Letter of the UMNS of the Russian Federation for the city of Moscow.