How to keep personal income tax in 1s accounting 8.3. Checking the correctness of personal income tax calculation

We propose to consider the nuances of accruing and withholding personal income tax in the 1C 8.3 program. And how to properly prepare for reporting on forms 2-NDFL and 6-NDFL.

An important point is the setting in 1C "Registration in tax authority which is responsible for reporting to tax service. Go to the menu tab "Main" and select "Organizations".

We go to our organization, click "More" and in the drop-down list select the item "Registration with the tax authority":

The next important setting is "Salary Settings" in the "Salary and Human Resources" section.

Go to the "General settings" section and specify in the item "Accounting for settlements by wages and personnel records are kept” - “In this program” so that the relevant sections are available.

Here we go to the "personal income tax" tab, in which we indicate the procedure for applying standard deductions"Cumulative total during the tax period":

The rate of insurance premiums is “Organizations using DOS, except for agricultural producers”.

Accident contribution rate - indicate the rate in percentage terms.

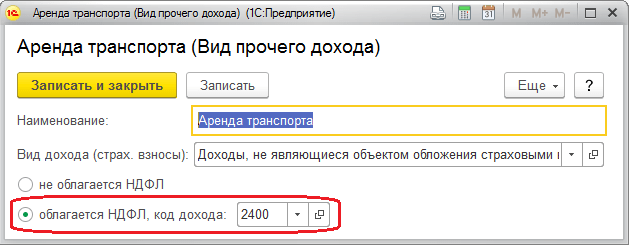

All accruals made are formed on the basis of the income code for individuals, which can be viewed in the built-in directory "Types personal income tax».

This directory can be corrected, for this we return to the "Salary Settings", expand the "Classifiers" section and follow the "Personal Income Tax" link:

After that, the window "Personal income tax calculation parameters" opens and go to the desired tab "Types of personal income tax":

For settings personal income tax for accruals and deductions in the "Payroll Settings" window, expand the "Payroll" section:

To start accounting for wages and personal income tax, the established parameters are enough. But do not forget to update the configuration to the current one.

Personal income tax is accrued and calculated for each actual income received on a monthly basis at the end of the reporting period (month) according to the documents “Payroll”, “Vacation”, “ Sick leave" other. Consider the document "Payroll".

The tax amounts for each employee will be reflected on the "Personal Income Tax" tab:

The same information can be viewed in the postings:

Based on the document, an entry is formed in the register “Accounting for income for personal income tax calculations» and the reporting forms are filled out:

Consumable cash warrant for the issuance of cash DS;

The document posting date will be the tax withholding date.

Let's pay attention to the document "Operation accounting for personal income tax". According to it, personal income tax is calculated from dividends, vacation pay and other material gain. To create a document, you need to go to the “Salary and Personnel” tab, the “Personal Income Tax” section and click the link “All documents on personal income tax”.

We get into the magazine. To create a new document, click "Create" and select the desired option from the drop-down list:

An entry in the register “Settlements of taxpayers with a personal income tax budget” generates almost every document that affects personal income tax.

Consider the example of the document "Write-off from the current account". Let's go to the tab "Salary and personnel" and open the item "Statements to the bank":

Let's create this document. And on the basis we will make a write-off from the account:

As well as register movements.

Today we will consider what - what tools and functionality the 1C program has for calculating personal income tax and its correct reflection in tax accounting.

The taxation procedure is entered when setting up the settlement type.

Fig.1

The code from Fig. 1 can be selected in the “Types of personal income tax income”, where each element is assigned a percentage of taxation and indicates whether it relates to wages.

The category of income allows you to clarify the date of its receipt in the statement that was originally indicated in settlement document. To specify the procedure for calculating the tax on the income of laid-off workers in the reference book of the same name, the calculation procedure is selected.

Fig.2

To indicate the option for calculating taxes for other incomes of individuals, the corresponding directories are also used.

Fig.3

You can designate the income code directly in the document field.

Fig.4

The deductions are stored in the "Types of personal income tax deductions".

Advance tax payments foreign citizens are fixed by the document of the same name "Advance payments for personal income tax". The statement on the legitimacy of the offset of the advance is located in "1C-Reporting".

In the registers of accounting for personal income tax in 1C 8.3, settlement documents are fixed the tax base and calculated tax, which is determined on the date of actual receipt of income.

The tax from all kinds of benefits, vacation and other inter-settlement payments in the documents is displayed immediately on the planned date of payment.

The actual receipt of income for types of calculation, in the income code of which is indicated “Corresponds to wages”, is dated by the last day of the month of accrual or the date of dismissal.

Fig.5

Income is fixed in "Accrual ...", "Awards", etc.

Fig.6

Fig.7

The tax withholding is dated from the date of payment entered on the payroll. The actual date of payment is also fixed by the documents “Confirmation of payment of income”, “Confirmation of salary transfer”.

When calculating the withholding, the basis document is filled out, according to which the amount of income is fixed, which is subsequently taken into account in line 130 in the 6-NDFL report.

For display in reports, the transferred tax is displayed in the payroll sheet when the attribute "Tax together with salary" or a separate form "Transfers to the budget" is indicated. In this case, the transfer period is determined by the type of income. The deadline is registered in the system during deduction and is used when compiling the 6-NDFL report.

For the analysis of personal income tax, there are the following reports:

- Monthly analytics;

- Register tax accounting for personal income tax;

- Consolidated 2-personal income tax.

If it is necessary to recalculate the tax in the ZUP for any reason, then use the document “Recalculation of personal income tax”, located in the “Taxes and contributions” menu. Here the tax is recalculated from the beginning of the tax period specified here.

Fig.8

To adjust the accounting for the type of tax in question, 1C ZUP uses a specialized document “Individual income tax accounting operation”. It allows you to edit tax registers:

- deductions, predst. upon notice to the NO;

- Provided standard and social deductions;

- Calculations of tax agents / taxpayers with the personal income tax budget;

- Accounting for income for the calculation of personal income tax.

If the tax is excessively withheld for the employee, then in the current period he will pay for it with a “minus”. In the event that for the current month his total amount for an employee is negative, he will not be withheld and will not be accepted as offset against future payments. In settlement personal income tax documents offset can be seen on the "Payout adjustments" tab. In the next period, the system will automatically reduce the withheld tax by the amount of the adjustment, but you can also return the tax using the "Refund".

The correct accounting of personal income tax in the system depends on the correctness of filling in the registration with the tax authority in the subdivision/organization card. Upon registration with the tax authority, relevant reports are collected in the ZUP. Based on the period for issuing income, the deadline date for the transfer is calculated, which is displayed in the registers during posting.

To correctly account for personal income tax in the 1C ZUP 8.3 (3.0) program, let's start with the basic settings.

Step 1. Accounting policy for personal income tax

Settings - Organizations (or Organization details) - Accounting policy:

Step 2. Personal income tax deductions

Section Taxes and contributions - Types of deductions for personal income tax:

The amount of deductions provided is stored in each type of deduction. If you notice that when calculating personal income tax, the wrong amount of the deduction is applied, then you can check it by opening the type of personal income tax deduction of interest:

In order for the amount of deductions in the 1C 8.3 ZUP database to comply with the law, it is necessary to maintain the working configuration in the current release, that is, update it regularly.

At the same time, the procedure for applying standard tax deductions, setting up personal income tax accounting parameters can be studied in the following video:

Step 3. Income subject to personal income tax

There are two ways to check which income in the 1C 8.3 ZUP program falls into the tax base and with which code:

- Open the accrual document (Settings - Accruals) tab Taxes, contributions, accounting:

- Open the list of accruals (Settings - Accruals) and use the button Setting up personal income tax, average earnings, etc.:

Step 4. Information about the taxpayer

Step 4. Information about the taxpayer

The following data is entered through the employee’s card using the link “Income tax”:

- Taxpayer status;

- Standard, property and social deductions;

- Notice of advance payments for patents;

- Income statement from previous employer:

Step 5. Registration with the tax authority

Organization like tax agent, submits reports on personal income tax at the place of registration of the organization or at the place of registration of separate divisions to the tax authority.

In the program 1C 8.3 Salary and personnel management, registration with the tax authority can be configured for the relevant types.

Important! The subdivision must have the sign “This is a separate subdivision”:

If the organization needs to keep records by territory, then this functionality First you need to include in the accounting policy of the organization:

Then create a territory (Settings - Territories) and indicate in which IFTS it is registered:

Calculation of personal income tax in 1C ZUP 8.3 using an example

Personal income tax is calculated in 1C 8.3 ZUP 3.0 in documents such as Payroll and contributions, Vacation, Sick leave, etc. Consider the calculation of personal income tax on the example of accrual of vacation.

To do this, create a Vacation document:

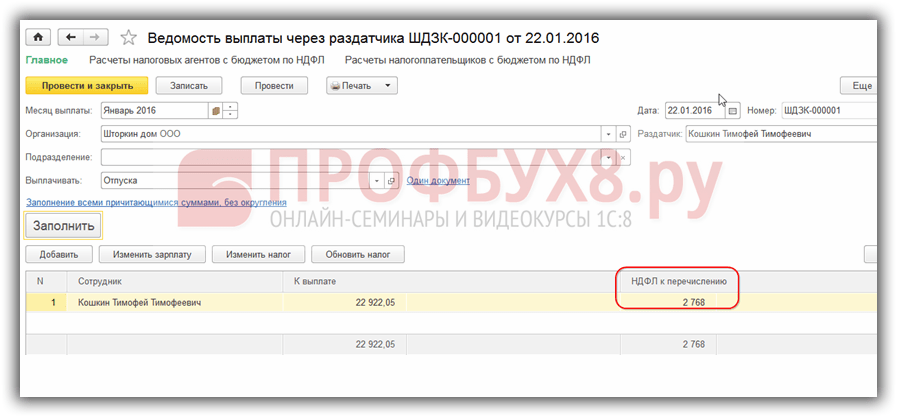

The document is the calculation of personal income tax. In our example of personal income tax amounted to 2,768.00 rubles.

How personal income tax reporting is generated in 1C 8.3 ZUP 3.0

When posting the Vacation document, an entry is made in the accumulation registers. Based on these registers, various personal income tax reports are generated, including the 2-personal income tax statement and the calculation of 6-personal income tax. These are the registers:

- Register “Accounting for income for the calculation of personal income tax”;

- Register “Calculations of taxpayers with the budget for personal income tax”;

- Register “Provided standard and social deductions (NDFL)”.

How to view entries in accumulation registers during accrual

You can see the entries made by the “Vacation” document in the navigation panel of the form. By default, the user does not see this panel.

Let's set it up. For this, being in open document, select Main Menu - View - Customize Form Navigation Bar:

The Customize Navigation Bar window opens. In the Available commands section, you must select the register by which you want to see the movements, that is, the records made by the 1C 8.3 ZUP program when posting the document. Then click the Add button.

For example, you need to see what entries were made in the register of taxpayer settlements with the personal income tax budget. For this:

- Select the register on the left Calculations of taxpayers with the budget for personal income tax;

- Click Add. A line from the Available Commands section goes to the Selected Commands section;

After such actions, you can see that a navigation bar has appeared in the Vacation document form, which always begins with the word “Main”, and then lists links to registers that will be added to the selected commands. In the example it looks like this:

By clicking on this command, you can see the entries made in the register:

You can return to the document form by clicking Main.

Similarly, any registers are added from the list of available commands in the form navigation settings for any documents. Just remember that for this setting the document must be open.

So, let's see what records on the movement of personal income tax in 1C 8.3 ZUP 3.0 were formed with the status of the Vacation document "Performed".

Accumulation register “Income accounting for personal income tax calculation”

This register contains information:

- on the amount of income in the context of income codes - comes from the calculation of the vacation received on the Accrued tab:

- date of receipt of income - is recorded in the register from the value of the requisite of the document Date of payment on the tab Main vacation:

- and the month of the tax period - from the Month variable in the document header:

The information contained in this register corresponds to the calculated personal income tax. An entry in this register is formed with a “+” sign (incoming):

The amount of personal income tax is stored in the context:

- date of receipt of income - enters the register from the details of the date of receipt of income, which is in the details of the calculation of personal income tax:

- tax rates;

- registration with the IFTS - in our example, the IFTS is taken, in which the organization itself is registered.

Accumulation register “Provided standard and social deductions (personal income tax)”

Entries in this register indicate that the employee is entitled to deductions and they were provided to him by this document:

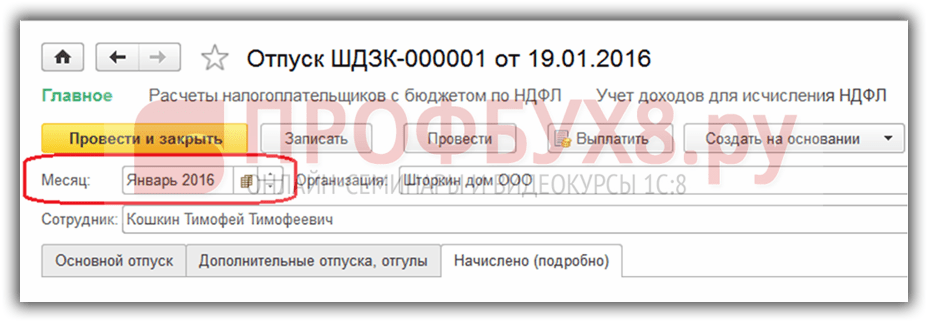

What you need to pay attention to when conducting the document “Vacation” for the correct accounting of personal income tax is props “Document date”(in our example, 01/19/2016) As can be seen from the illustrations, this date passes through all the listed registers as the “Period” attribute.

How is personal income tax withheld upon payment

In our example, the payment of wages is made through the distributor, so for this we will create the document Statement of payment through the distributor:

- Choose the month of payment - January 2016;

- The date of the document must correspond to the date of payment, for example, it is 01/22/2016;

- We indicate that we pay vacation;

- By the link “Not selected”, we choose which vacation we pay;

- We finish by pressing Select:

When filling out the document, 1C ZUP 3.0 automatically sets the amount To be paid and the amount of personal income tax to be transferred:

If you slightly change the data in the document, for example, change the date of the document, then the picture will be completely different - in the tabular part, personal income tax is not filled in for the transfer:

The question arises: Why is personal income tax not filled in for the transfer? It turns out that the date of the document is very important, that is, the date when the payment is formed. Personal income tax, which arose when calculating the vacation, was formed on the date of 01/19/2016. and, accordingly, it cannot be listed earlier than this date, that is, it is simply not yet in the 1C ZUP 8.3 database. Entries from personal income tax data appear in all registers only from 01/19/2016.

How to view entries in accumulation registers upon payment

The document that forms the payment also moves through the registers associated with personal income tax.

Accumulation register “Settlements of taxpayers with the personal income tax budget”

The record that the payment forms is formed in the register with the sign “-” (expense) and such personal income tax is considered to be withheld.

The amount of personal income tax withheld is stored in the context of:

- dates of receipt of income - this is the date of receipt of income, which can be viewed in the details of the calculation of personal income tax of the Vacation document itself;

- tax rates;

- registration with the IFTS.

It is the data on withheld tax that then fall into the reporting on 6-personal income tax:

Accumulation register “Calculations of tax agents with the personal income tax budget”

We see that two entries were made in this register:

- + (“arrival”) - personal income tax withheld;

- – (“expense”) – listed personal income tax:

Since 2011, a number of changes made to Chapter 23 of the Tax Code of the Russian Federation have come into force. federal law dated July 27, 2010 No. 229-FZ. In particular, starting from 2011, keep records of personal income tax agents are prescribed in the tax accounting registers, the forms of which are proposed to be developed independently. In the program "1C: Payroll and HR 8" (release 2.5.32), the tax register form has already been implemented. O new form and changes related to the accounting and calculation of personal income tax, says E.A. Gryanina, independent consultant.

paragraph 1 of Article 230 of the Tax Code of the Russian Federation

The amount of tax calculated

Amount of tax withheld

The amount of tax transferred

.

In register Calculations of tax agents with the personal income tax budget Coming Consumption Transfer of personal income tax to the budget.

List of documents Transfer of personal income tax to the budget of the Russian Federation can be called from the menu Taxes and contributions -> Transfer of personal income tax to the budget of the Russian Federation taxes, paragraph Transfer of personal income tax to the budget of the Russian Federation(see fig. 1).

Rice. one

In the header of the document Transfer of personal income tax to the budget of the Russian Federation

In the tabular section Employees Fill in -> Individuals

Fill -> Tax Amounts

When conducting a document Transfer of personal income tax to the budget of the Russian Federation Calculations of tax agents with the personal income tax budget.

Accounting for the transferred amounts of personal income tax for each taxpayer

The form of the tax register for personal income tax is not regulated by law, however, the new wording of paragraph 1 of Article 230 of the Tax Code of the Russian Federation lists information that must be contained in tax register. The composition of this information is expanded in comparison with the data of the 1-NDFL form, which was previously used. In particular, now tax agents need to additionally take into account the amounts actually transferred for each individual personal income tax indicating the date of transfer and details of the payment document. This amount will also need to be indicated in the information on the income of individuals in the form 2-NDFL for 2011. Thus, since 2011, tax agents need to take into account three amounts of tax for each individual:

The amount of tax calculated- how much tax was charged to be withheld from the income of an individual;

Amount of tax withheld- how much tax was actually withheld when paying income to an individual;

The amount of tax transferred- how much tax was actually transferred to budget system.

To register the amounts of the transferred tax in the program "1C: Salary and Personnel Management 8" created new document Transfer of personal income tax to the budget of the Russian Federation. To account for the amounts to be transferred and actually transferred to the budget for each individual - a new accumulation register Calculations of tax agents with the personal income tax budget.

In register Calculations of tax agents with the personal income tax budget with a "+" sign (according to the type of movement Coming) reflects the amount of tax withheld from individuals, subject to transfer to the budget, with the sign "-" (by type of movement Consumption) - transferred amounts of tax. The balance of the register shows the amount of tax withheld from employees, but not yet transferred to the budget - it is this data that is used to automatic filling program document Transfer of personal income tax to the budget.

Please note that the date of the document and the date of payment must be no earlier than the first day of the month following the billing period.

After updating the version of the program, in the information base it is necessary to register the transfer of personal income tax in respect of all income received by taxpayers, starting from 01/01/2011. It is recommended to register the transfer of personal income tax upon payment.

List of documents Transfer of personal income tax to the budget of the Russian Federation can be called from the menu Taxes and contributions -> Transfer of personal income tax to the budget of the Russian Federation or from the program desktop: bookmark taxes, paragraph Transfer of personal income tax to the budget of the Russian Federation(see fig. 1).

Rice. one

The transfer of personal income tax is registered in the program separately for each month of the tax period, for each tax rate and OKATO + KPP code.

In the header of the document Transfer of personal income tax to the budget of the Russian Federation you should specify: the date of payment, the month of the tax period for which the tax was transferred, the details of the payment order for paying the tax, the tax rate, in case of separate subdivisions, specify the OKATO / KPP code, and enter the total amount of the tax transferred at this tax rate and code OKATO / checkpoint.

In the tabular section Employees- indicate how much tax was transferred for each specific taxpayer. The list of employees can be filled in automatically on command Fill in -> Individuals who received income. The list will include all individuals for whom the program has registered tax amounts for transfer. The amount for each individual will be calculated by proportional distribution of the total amount indicated in the header of the document. If necessary, the amounts in the tabular part can be adjusted manually. The total amount of tax for all taxpayers must match the amount indicated in the header of the document.

If the list of employees in the document is selected manually, then the command is used to distribute the total amount of tax among employees Fill -> Tax Amounts(allows you to fill in tax amounts without refilling the list of individuals).

When conducting a document Transfer of personal income tax to the budget of the Russian Federation the amounts of transferred tax for each individual indicated in the tabular part are recorded in the accumulation register Calculations of tax agents with the personal income tax budget.

The distribution is made in proportion to the amounts of tax to be transferred for each individual (the balance in the accumulation register Calculations of tax agents with the personal income tax budget). For example, if, for some reason, only 50% of the total withheld from employees is paid to the budget personal income tax amounts, then for each individual a transfer of half of the amount of tax withheld from him will be registered.

Register of tax accounting for personal income tax

To compile the tax accounting register for personal income tax, a new report has been added to the program Register of tax accounting for personal income tax. The report can be called using the submenu item of the same name Taxes and contributions or from a bookmark taxes desktop program.

Using this report, you can generate tax accounting registers for personal income tax for the selected taxable period immediately for all employees of the organization or only for the selected list of individuals.

The form of the tax accounting register for personal income tax, implemented in the program, fully complies with the requirements for the composition of information specified in paragraph 1 of article 230 of the Tax Code of the Russian Federation. Recall that in accordance with paragraph 1 of Article 230 of the Tax Code of the Russian Federation, the tax register must contain information that allows you to identify the taxpayer, the type of income paid to the taxpayer and the tax deductions provided in accordance with the established codes, the amount of income and the date of their payment, the status of the taxpayer, the dates of withholding and tax transfers to the budget system of the Russian Federation, details of the relevant payment document.

The Register includes 7 sections.

Section 1 contains information about the tax agent.

In section 2 - information about the taxpayer (recipient of income). In paragraph 2.9, in the form of a table, information is presented on tax status taxpayer. For designation, the same taxpayer status codes are used as for Form 2-NDFL: 1 - tax resident, 2 - non-resident, 3 - highly qualified foreign specialist.

Section 3 provides information about the right of the taxpayer to standard tax deductions. This information is filled in based on the data on deductions indicated for an individual in the form Data entry for personal income tax(see Fig. 2).

Rice. 2

Section 4 displays calculation information tax base and personal income tax. Section 4 is formed separately for each OKATO/KPP code. If during the tax period the employee worked and received income in various separate subdivisions, then the Register of this employee will contain several sections 4. Section 4 consists of several subsections.

Subsection Calculation of personal income tax at the rate of __% formed separately for each tax rate. In the subsection, by months of the tax period, codes and amounts of income received by the taxpayer, amounts of taxable income and calculated tax are given. For income taxed at a rate of 13%, an additional table is displayed with information on the tax deductions actually granted to the taxpayer.

In subsections Tax calculated, Withheld tax and Listed tax the amounts of calculated, withheld and transferred tax are given, respectively, by months of the tax period and tax rates. In a separate column, the date of the operation is noted: calculation, deduction, transfer of tax. For the amounts of the transferred tax, the details of the payment order are additionally displayed (see Fig. 3).

Rice. 3

Section 5 specifies total amounts tax deductions actually granted to the taxpayer in general for the tax period. Information is displayed in the context of OKATO / KPP codes and deduction codes.

Section 6 provides the total amounts of income and tax based on the results of the tax period in the context of OKATO / KPP codes and tax rates.

Section 7 indicates information on the submission of certificates of income of the taxpayer in the form 2-NDFL.

Change in the calculation of personal income tax associated with changes in the Tax Code of the Russian Federation

Since 2011, the procedure for calculating personal income tax for individual cases has changed.

According to the new in 2011, the tax is calculated in the event that an employee is provided with property deductions. The changes relate to the month from which the deduction begins to apply. In accordance with the new wording of Article 220 of the Tax Code of the Russian Federation, property tax deductions are provided for the employee's income received starting from the month the employee submits an application for such a deduction. Previously, the deduction was provided for income from the beginning of the tax period, regardless of the month in which the employee submitted the application. When calculating personal income tax in the month the application was submitted, the program recalculated the tax from the beginning of the year, and it was possible to return or offset the amount of tax on income for previous months. In 2011, tax recalculation for the months of 2011 preceding the month the employee submitted the application is not made.

In addition, the procedure for calculating tax when an employee acquires the status of a tax resident of the Russian Federation has changed. In accordance with the new wording of Article 231 of the Tax Code of the Russian Federation, the recalculation and refund of tax when a taxpayer acquires the status of a tax resident is carried out by the tax office. Previously, the tax agent could recalculate and return the tax in this case, so the program recalculated the tax at a rate of 13% for the entire tax period. In 2011, when an employee acquires the status of a tax resident of the Russian Federation, the tax from the beginning of the year is not recalculated, but begins to be calculated at a rate of 13% from the month the status was changed.

Examples of tax calculation for these cases are considered in the ITS reference book "Keeping personnel records and settlements with personnel in 1C programs".

Change in the calculation of personal income tax associated with the subsystem for calculating personal income tax

We note one more change in the program related to the subsystem for calculating personal income tax. The place where information about the tax status of an employee is entered has changed. Previously, the input was carried out in the form of entering data on the citizenship of an individual. Now the status of the taxpayer is indicated on a special page of the form Data entry for personal income tax(called from the individual data form by the button personal income tax, or from the field Status directory Employees) - see fig. 4.

In this article I want to consider the aspects of accrual and withholding personal income tax in 1C 8.3, as well as the preparation of reports in the forms 2-NDFL and 6-NDFL.

Setting up registration with the tax authority

The most important setting, without it it will not be possible to submit reports to regulatory authorities. Let's go to the directory "Organizations" (menu "Main" - "Organizations"). After selecting the desired organization, click the "More ..." button. From the drop-down list, select "Registration with the tax authorities":

You must carefully fill in all the details.

Setting up payroll accounting

These settings are made in the section "Salary and personnel" - "Salary settings".

Let's go to "General Settings" and indicate that accounting is kept in our program, and not in an external one, otherwise all sections related to personnel and salary accounting will not be available:

On the "personal income tax" tab, you need to indicate in what order standard deductions are applied:

On the "" tab, you need to indicate at what rate insurance premiums are calculated:

Any accruals individuals produced by income code. To do this, the program has a directory "Types of personal income tax". To view and, if necessary, correct the directory, you need to return to the "Salary Settings" window. Expand the "Classifiers" section and click on the "NDFL" link:

A window for setting the parameters for calculating personal income tax will open. On the corresponding tab is the mentioned reference book:

To set up personal income tax taxation for each type of accrual and deduction, you need to expand the "Payroll" section in the "Payroll Settings" window:

In most cases, these settings are enough to start accounting for wages and personal income tax. I will only note that the directories can be updated when updating the program configuration, depending on changes in legislation.

Accounting for personal income tax in 1C: accrual and deduction

Personal income tax is charged on each amount of actually received income separately for the period (month).

The amount of personal income tax is calculated and charged with documents such as "", "", "" and so on.

As an example, let's take the document "Payroll":

Get 267 1C video lessons for free:

On the tab "personal income tax" we see the calculated amount of tax. After posting the document, the following personal income tax transactions are created:

The document also creates entries in the register “Accounting for income for the calculation of personal income tax”, according to which reporting forms are subsequently filled out:

The actual tax withheld from the employee is reflected in the accounting when posting documents:

- The operation of accounting for personal income tax.

Unlike accrual, the tax withholding date is the date of the posted document.

Separately, you should consider the document "Individual income tax accounting operation". It is provided for the calculation of personal income tax from dividends, vacation pay and other material benefits.

The document is created in the "Salary and Personnel" menu in the "Personal Income Tax" section, the link "All documents on personal income tax". In the window with the list of documents, when you click the "Create" button, a drop-down list appears:

Almost all documents that in one way or another affect personal income tax create entries in the register “Taxpayer settlements with personal income tax budget”.

As an example, let's consider the formation of tax accounting register entries by the document "Write-off from the current account".

Let's add the document "" (menu "Salary and personnel" - link "Bills to the bank") and on its basis we will create a "Debit from the current account":

After conducting, let's see the postings and movements in the registers that the document generated:

Formation of reporting on personal income tax

Above, I described the main registers that are involved in the formation of the main personal income tax reports, namely:

In the window with the list of documents, click the create button and fill in the certificate for the employee:

The document does not generate postings and entries in registers, but is used only for printing.

- (section 2):

The report refers to regulated reporting. You can also go to its design from the "Personal Income Tax" section, the "Salary and Personnel" menu, or through the "Reports" menu, the "1C Reporting" section, "Regulated Reports".

An example of filling out the second section:

Checking withheld and accrued personal income tax

To check the correctness of the calculation and payment of tax to the budget, you can use "". It is located in the "Reports" menu, section - "Standard reports".

- Economic security of the Russian Federation Political economic security of the Russian Federation

- Antimonopoly policy, its goals and methods The main direction of the antimonopoly policy of the state is

- What reforms did Witte make briefly

- Okun's law and the theory of "full employment" of the population