Annual balance form 1. Balance sheet: form, filling out

New form "Balance sheet" officially approved by the document Appendix No. 1 to the Order of the Ministry of Finance of the Russian Federation of 02.07.2010 No. 66n (as amended by the Orders of the Ministry of Finance of Russia of 05.10.2011 No. 124n, of 04.06.2015 No. 57n).

Learn more about applying the Balance Sheet form:

- The procedure for filling out the balance sheet in a general form. Example

Indication of the number of the corresponding explanation to the balance sheet (if explanatory note). ... indicating the number of the corresponding explanation to the balance sheet (if an explanatory note is being drawn up). ... contributions of comrades). Line 1310 of the balance sheet reflects the amount authorized capital firms... entered data. Example. Filling in the balance sheet of an LLC registered in 2015 ... based on the available data, the accountant compiled balance sheet for 2015 to...

- The procedure for completing the balance sheet in a simplified form. Example

On financial results. The procedure for filling out the balance sheet in a simplified form Start filling out ... rubles. In the simplified form of the balance sheet, there are significantly fewer sections and indicators ... to explain the procedure for the formation of indicators of the balance sheet and financial statement ... that are not disclosed by the indicators of the balance sheet and income statement ... it is better to fix in the accounting policy. Example. Completing the balance sheet of an LLC registered in ...

- Company reorganization: we draw up a deed of transfer and a balance sheet (part 2)

When compiling deed of transfer and balance sheet during the reorganization of the company? The order of formation ... for small businesses, consists of: balance sheet; statement of financial results; report... on the use of funds received. How to draw up a balance sheet The final financial statements of reorganized companies that ... form a merger (accession) into the opening balance sheet of a company resulting from the reorganization ...

- Company reorganization: drawing up a deed of transfer and balance sheet (part 1)

When drawing up a deed of transfer and balance sheet during the reorganization of a company? What... when drawing up a deed of transfer and a balance sheet for a company reorganization? Reorganization... service. The general principle for the formation of financial statements during the reorganization of a company is given ... in the Guidelines for the formation of financial statements during the reorganization ... the indicators of the transfer act and the final financial statements of the reorganized company do not match ...

- Audit of the annual financial statements of organizations for 2018

Determine the details of the indicators for the items of the balance sheet, income statement, report ... depreciation. According to PBU 4/99, the balance sheet must include numerical indicators in ... values. An intangible asset is reflected in the balance sheet at cost minus the amount ... the asset is disclosed in the notes to the balance sheet and the income statement ... the organization usually consists of a balance sheet, a report on the intended use of funds ...

- What to look for when preparing annual financial statements for 2017

It is known that the annual accounting (financial) statements consist of a balance sheet, a report on ... methods of maintaining accounting, including simplified accounting (financial) statements - a balance sheet and a report ... all active-passive accounts in the balance sheet should reflect a "detailed" balance. ... on a loan is reflected in the balance sheet as a short-term liability, ... they are exclusively in accounting practice. For example, the indicators of the balance sheet and the report on ...

- Renting Cows: Accounting

In relation to a specific accounting object, a method of accounting is selected from the methods ... established by law Russian Federation on accounting, federal and (or) ... 73); - methodological recommendations"On the accounting of fixed assets in agricultural ... "On the approval of the Chart of Accounts for accounting for the financial and economic activities of enterprises ...) Recognition is the process of inclusion in the balance sheet or income statement and ...

- Events after the reporting date: how to reflect and how to disclose in financial statements

Disclosed in the notes to the balance sheet and the financial statement... except credit organizations) Russian accounting legislation regulates the procedure for recording ... disclosed in the notes to the balance sheet and the financial statement ... disclosed in the notes to the balance sheet and the income statement ... actual cost goods. In the balance sheet, inventories are reflected in ... disclosure in the notes to the balance sheet and the statement of financial ...

- Accounting and tax accounting in an organization that has a branch

Indicated in the Unified State Register of Legal Entities. Accounting Separate balance In the current regulatory ... balances). It follows from this rule that branches do not form separate accounting ... statements and do not draw up a separate balance sheet. This means that ... the organization's policy "accounting methods chosen by the organization with ... branches allocated to a separate balance sheet maintain accounting independently, but in ... are transferred to its balance sheet. In the accounting of the branch there will be ...

- Features of the presentation of financial statements in 2018

The subject includes: indicators reflected in the balance sheet, statement of financial results of activities ..., provision is made for the formation of reserves, are reflected in the balance sheet of reporting entities minus the indicated ... acts regulating accounting and preparation of accounting (financial) statements. Balance sheet. Provisions n ... that assets and liabilities in the balance sheet are presented with a division into long-term ...

- The discrepancy between the indicators of tax and accounting reporting under the simplified taxation system: how to explain with the tax?

Accounted for on a cash basis. Accounting (financial) reporting. The annual financial statements are prepared in accordance with ... as a general rule, it consists of a balance sheet, a statement of financial results and ... accounting methods, including simplified accounting (financial) statements, then the following may be of interest to the balance sheet, report ... accounting indicators. Let's start with the balance sheet. In this case...

- Financial statements - 2017: recommendations of the Ministry of Finance

The balance of other balance sheet items for the earliest presented in ... Regulations on accounting and financial reporting in the Russian ... adjustments are reflected in accounting and financial statements as changes ... adjustments are reflected in accounting and financial statements as changes ... indicators may be presented in the balance sheet or financial statement ... by disclosure in the notes to the balance sheet and financial statement ...

- The owners of the premises demand accounting documents from the Criminal Code: is it legal?

accounting accounts, Bank statements and payment orders for the year. Balance for ... accounts, bank statements and payment orders for the year. Balance... including: information on annual financial statements; balance sheet and appendices to it; information... art. 5 of the Accounting Law). Accounting - the formation of a documented systematized ... activity should be included in the financial statements. Financial statements must be accurate...

- New in accounting reporting in 2019

Year. New requirements for financial statements Accounting statements until 2019 ... for the annual publication (disclosure) of financial statements. For untimely reporting ... the report is an independent form of financial statements and may have ... accounts 76.14 in the balance sheet On the new account 76. ... In the financial statements, the account will be reflected in the asset balance line ... exceptions. For example, companies whose annual financial statements contain information, ...

- The order of reflection in the notes to the balance sheet and to the statement of financial results of short-term deposits accounted for as part of the financial investments of the organization

... (numerical indicators), which should contain the balance sheet of the organization. So, assets accounted for under... Order N 66n explanations to the balance sheet and income statement... .1 section 3 of the explanations to the balance sheet and income statement... materials: - Encyclopedia of decisions. Explanations to the balance sheet "Financial investments"; - An encyclopedia of... solutions. Interrelation of indicators of the Balance Sheet and Explanations to the Balance Sheet and the Statement of Financial ...

Everything legal entities are required to submit financial statements, moreover, this documentation is submitted both to the tax structure and to the statistical authority. Reporting must include specialized forms of documents 1 and 2, as well as a report on all changes that occur with capital, and a specialized report on the movement cash flows at the enterprise. A prerequisite is the compilation auditor's report, which reflects the reliability of all accounting reports.

It should be noted that individual entrepreneurs do not submit such reports, and certain entrepreneurs who are small business entities can use a simplified reporting option. In a simplified form, only the financial results of indicators are submitted. In fact, the document is drawn up without certain details. There are also applications that form the provision of more advanced data. These applications are filled with the most significant indicators, without which it will be impossible to carry out analytical actions on the operation of the enterprise.

Any entrepreneurial activity accepts the need to generate various reports, on the basis of which the analysis process is carried out internal state enterprises, and state structures have the opportunity to assess the correctness of the calculation of taxes, etc. The correctness of the preparation of these documents depends on a detailed study of all the nuances of the structure of preparation. Successful business also depends on the results obtained, correctly conducted analysis, on the basis of which the company has the opportunity to properly allocate funds for a more intensive development of its activities.

In paragraph 5 of part 1 of Art. 23 tax legislation it is determined that all types of reports must be submitted in two versions, and it is established reporting period- year. If the company draws up and calculates interim reports, they can also be submitted to the tax authority and the statistics department. In this article, we will talk about how financial statements are drawn up in accordance with established forms, taking into account all the nuances, and we will reveal the essence of the correct preparation of all mandatory lines of documents.

Balance- the most significant document that actually characterizes all the features of the organization's activities for a clearly defined period of time. Based on the balance sheet, you can determine the current position of the enterprise.

In this balance, a kind of separation of assets, as well as liabilities, is carried out. Moreover, the division is carried out depending on the maturity or circulation on the basis of the terms for which certain obligations or assets were issued. The division is carried out for the short term (insignificant period of time) and the long term. All assets, as well as liabilities, are considered short-term if the duration of the operating cycle is not more than a year. If the term is more than a year, then in this case a long-term perspective or obligations is formed.

All the data that is entered into this balance sheet is able to reveal the nuances of the development of the enterprise, the organization's specialists, on the basis of the balance sheet, analyze the activity, it should also be said that this reporting option is submitted to the tax authority and to the statistical department.

The legislator establishes a clearly developed form of the document, which was adopted by Order of the Ministry of Finance of Russia dated 02.07.2010 No. 66n. At the same time, it is established that when drawing up a balance sheet, the organization has the right to independently determine all indicators, taking into account the importance of certain parameters.

The balance sheet in form 1 contains two main parts:

- Assets;

- Passive;

The asset section provides data on all the resources that the organization has. The next section provides information on the issue of creation - the emergence of assets. The peculiarity of this balance sheet is that a kind of equality of the totals for liabilities and assets is formed. This structure is due to the fact that the principle of double entry has been formed.

Compilation instructions:

- The first asset block contains two sections. It contains data on non-current and current assets. The remaining parameters of the value of these assets must be carried out on line 1110. At the same time, it is this parameter that allows you to analyze the activities of the enterprise, allows you to determine that the object has the ability to bring economic parameters benefits in the future, or already brings this benefit, and the object is aimed at the long-term perspective of its work. As for current assets, in this case we are talking on fixing data on the value of inventories. The data is reflected in line 1210. This includes the cost of raw materials, as well as materials, all costs that determine work in progress. The cost of goods and products that are actually purchased and are in stock, etc.;

- The liabilities are divided into three sections. Each section includes the need detailed description data. Capital and reserves - a section that includes all data relating to the capital of the authorized type, as well as the shares of investors. Long-term liabilities are a reflection of all borrowed funds and credit obligations. In fact, this section reflects information that can reveal the negative balance of the enterprise, taking into account the long-term perspective. Short-term liabilities are an indication of the amount of borrowed or credit funds that will be returned during the year.

All elements of liabilities and assets are considered balance sheet items. All asset items are able to reveal the essence of those resources that are available to the enterprise and can be used as an element of development, the value of assets is also determined. Liability articles are able to reveal all the data on the sources of resource formation. In fact, data on borrowed and credit funds, which allows you to determine the effectiveness of such actions and the prospects for the development of the enterprise.

- All data that is reflected in the balance sheet accounting type must certainly correspond to the data that were carried out in other balance sheets at the end of the reporting period (end of the year). In case of reorganization, this fact is taken into account;

- It is not allowed to form an offset between the articles of liabilities and assets, between losses and profits. At the same time, the legislator provides for the possibility of such a set-off, while drawing up additional application;

- All items on assets should actually be confirmed by documents reflecting the inventory, calculations, liabilities, etc.

The standard form of the document is approved by law. Nevertheless, it must be borne in mind that the information that is entered into the document is determined precisely by the management of the enterprise, taking into account its significance. For example, minimum credit obligations for an insignificant period may not be reflected in the reporting documents. But when it comes to a loan that is issued for several years, then such data must certainly be reflected in the report.

The enterprise has the right to be based on form 1, but to create a form of its own sample. However, one must be guided general rules and requirements for the preparation of financial statements.

The need to indicate the following mandatory details in the balance sheet has been established:

- The date is determined when the balance sheet preparation process is carried out and the date of the reporting period for which this reporting documentation is compiled and provided;

- It establishes the need to indicate the full name of the organization, and the legislator requires that the specified name correspond to the data specified in the statutory documents;

- You also need to indicate the tax payer number, as well as the main codes of the enterprise. It is necessary to indicate the classification of OKOPF and OKFS. The units of measurement that are used in the process of compiling the document are indicated, and it is also provided legal address enterprises;

- The date the document was actually sent to the appropriate authorities.

All sum parameters of balance sheet items should be provided in thousands of rubles, respectively, decimal places are not indicated. If the company has a more significant turnover, then the data can be provided in millions. All amounts of certain assets may be presented as a total, subject to the disclosures in the notes accompanying the balance sheet. But, such actions are carried out if the indicators are not important, and they can be generalized.

First section: Non-current assets:

- These are certain works of science, programs, inventions, models, production secrets, and even business reputation. This includes all research expenses, which are reflected in account 04, and are indicated in the balance sheet in line 1120. Exploration assets are also indicated. These indicators should be reflected in lines 1130 and 1140;

- Fixed assets must be indicated in line 1150. In fact, the line reflects information about fixed assets, as original cost. These funds also include property received by the enterprise under a leasing agreement, as well as all objects that are without fail pass state registration ownership;

- A description of information about investments of a financial type is formed. A division is established into short-term investment options, if the period is not more than a year, as well as longer-term investments. To specify amounts long-term investments line 1170 is assigned. All investments that are invested in subsidiaries, the acquisition of shares, etc. are immediately reflected;

- There is a section - long-term assets, which are reflected in line 1190, data are generated if it is necessary to reflect long-term loans with a term of more than one year. There are also short-term investments that are held on line 1230;

- Deferred assets are indicated in line 1180, moreover, simplistic people do not fill out given line, but do not put a dash, but simply leave it empty. Line 1190 indicates data that relates to all other non-current assets.

Second section: negotiable assets:

- First of all, data on working stocks are indicated. An indication of the cost of all inventories that the enterprise has is formed. The data is reflected in line 1210. The indicator does not need to be decoded. But, if the inclusions in line 1210 are important, for example, the division into work in progress costs and raw material costs, then in this case it is necessary to decrypt the data;

- VAT is indicated, the data is indicated in line 1220. Simplifiers do not fill out this line, since they reflect input VAT on accounts 19, and in fact, VAT is not paid under this taxation system;

- Line 1230 defines the data accounts receivable. The line contains information about short-term debt obligations. Investments of a financial type are reflected in line 1240. The indicator determines the types of funds that were provided as a loan for a year (no more);

- A line is filled in with indicators of cash equivalents and cash. To fill in these lines, in fact, it will be necessary to sum up all cash equivalents - account balances, cash on accounts 50, 55, 52, 57. In line 1260, you can indicate all other current assets that could not be entered in another column of the document.

Third section: Capital and reserves:

- The data of the authorized capital are indicated in line 1310. The amount indicated in this line must clearly match the data that are fixed by the statutory documents;

- Be sure to indicate the data that reflect the presence of own shares, which in the course of activity were acquired by the organization from shareholders. Such data is entered in line 1320. In the event that treasury shares were bought back and then resold, they are considered an asset. This means that their data must be entered in line 1260;

- All other current assets are entered in line 1340. This shows the actual revaluation of all objects and those intangible assets that are held in the additional capital account;

- Additional capital without revaluation is reflected in line 1350. The indicator for this line is reflected only without the revaluation amount. This is followed by a line with reserve capitals, their balance is reflected in line 1360. A breakdown of all data on reserve capital required when some data is essential, very important for the analysis of the enterprise;

- Values are required uncovered loss. All undistributed profit options should be reflected in line 1370. And data on the amount of uncovered loss is also entered here. This amount is shown in brackets. Certain indicators of this loss or retained earnings can be deciphered in additional lines. In fact, it is possible to implement the provision of a more accurate financial result for profit and loss.

Fourth Section: Long-Term Commitments

An indication of borrowed funds is immediately formed. Line 1410 is filled in, in which data on the enterprise's debt for all long-term operations are entered. In fact, this reflects the data of credit and loan obligations, taking into account the fact that their execution will be carried out for more than one year. Profit tax payers are required to draw up line 1420;

All estimated liabilities are reflected in line 1430, it should also be noted that contingent liabilities and assets are not always reflected in the document, since the organization may not recognize these indicators in accounting;

All other liabilities are reflected in line 1450.

Fifth section: short-term liabilities

- All funds that were received by the organization for a short period of time are reflected in line 1510;

- total amount credit debt should be reflected in line 1520. If the amount of debt is significant, then it should not be generalized, but should be written taking into account significant loan obligations;

- Line 1530 is filled in if your company receives certain budget funds or amounts for targeted funding;

- A provision is included in line 1540, but only if the entity recognizes this use of the liability.

This reporting form, which in its composition contains information about expenses, incomes and results financial activities. The form is approved by law, it contains information about all the actions of the organization. By compiling this document, you can determine the rationality of the organization's activities, calculate profits, etc.

The form of this document forms the need to provide the following information:

- Indication of the period for which data is provided, as well as dates, provision of information about the organization, as well as an indication of units of measurement;

- The following is a table with reporting indicators. This is the number of explanations, data of indicators and specialized codes, as well as a column with the value of indicators for a clearly defined reporting period. And the same column with indicators that were provided last year.

How is Form 2 compiled?

- Revenue data is indicated in line 2110. It is necessary to show all income data that relate to common species enterprise activities.

- In line 2120, you will need to indicate the cost of sales. In fact, the amount of expenses for all types of activities of the enterprise is indicated. For example, expenses that are formed on the basis of the production of products, the purchase of raw materials, the implementation certain works;

- In line 2100, you will need to indicate the gross result. This is ordinary profit data, excluding all management and selling expenses. To make a calculation this indicator, you need to deduct the amount of cost of sales from the amount of revenue. If a negative indicator is formed, it is indicated in brackets (parentheses are used);

- All commercial expenses that are generated at the enterprise are entered in line 2210, and administrative expenses are indicated in line 2220;

- In line 2200, an indication of data is generated in the form of profit or loss of the enterprise. The calculation is carried out by deducting commercial and administrative expenses from the amount of gross profit;

- All income that is received indirectly is reflected in line 2310, for example, an indication of dividends or the value of property. Income received from participation in other organizations is indicated in line 2310, and the interest that the enterprise receives on loans and securities are indicated in line 2320;

- The interest that the company will pay itself is indicated in line 2330, and other expenses in the next two lines;

- Line 2300 indicates income from taxation. This line shows accounting profit or a loss from the activities of the enterprise, but the current tax indicators should be reflected in line 2410.

Net profit should be reflected in line 2400. After compiling this table, provision is made background information. The results of the revaluation of non-current assets are indicated, and without taking into account net profit. Be sure to indicate the results of all operations that did not include net income. Provides data on the total financial result etc.

This form must be signed by the principal. Previously, the document was mandatory signed by the chief accountant, today, the document should not contain this requisite, but at the same time, the legislator does not prohibit the signing of the accountant on the document.

conclusions

The need for entrepreneurs and legal entities is the preparation of specialized accounting-type documentation. Certain IP documents are not compiled, the system for providing balance sheets for small businesses. Drawing up forms 1 and 2 has a lot of nuances. However, the legislator clearly developed the forms of documents, and provided instructions on the basis of which the process of filling out the documentation becomes simpler and faster.

Completing Form 2 is a simple process. The form is presented in the form of a table, where you just need to enter certain data about the activities of the enterprise. As for form 1, the structure of its compilation will be more complex, since there you need to specify a lot of different data to check tax structure, as well as for the statistical department. The forms of documents that must be submitted in accordance with the norms of the law can be found on the official website of the Federal Tax Service. It is here that you can find the actual forms that need to be filled out exactly at the current time.

Also on the network you can watch a lot of videos on the issue of compiling balance sheets, here is a video that will certainly help you in this matter.

Report No. 1 in all organizations is the balance sheet, since it is he who provides information about the company's assets and the size of the sources of these assets on reporting date, although entrepreneurs are allowed not to keep accounting and not to hand over the balance sheet. The form of the document is periodically reviewed and changed to legislative level. Learn more about this document and the features of its compilation.

Balance sheet for 2017

The form of the balance sheet for 2017, the form of which we will consider in this publication, is not so new. It was approved by order of the Ministry of Finance of the Russian Federation No. 66n dated July 2, 2010 and has been used since 2011.

An important change in the current year is the introduction of a new classifier OK 029-2014, and, as a result, a change in OKVED codes. Therefore, when compiling the balance sheet and submitting reports, companies will have to pay attention to the reflection of OKVED in the balance sheet for 2017 in accordance with the newly adopted collection. Although the replacement of codes is carried out automatically, it is better to first clarify information about OKVED with the tax authorities. It can be noted that only in this respect the form of the balance sheet for 2017 has undergone changes. The document can be downloaded below.

Balance sheet 2017: features

When filling out the form, the company itself details the indicators by article, taking into account the level of materiality of each. Submit to the regulatory authorities (IFTS and Statistical Office) financial statements relies on a form that provides line codes. We will present a sample of filling out the balance sheet for 2017 in this form.

The basis for the balance sheet is accounting registers, for example, a chess sheet, memorial orders, order magazines, a balance sheet or a general ledger.

Balance sheet form for 2017: how the document is structured

The balance sheet of the organization is a table, on the left side of which all the assets of the company are reflected, and on the right - the sources of these funds. Both of them must be equal, since the value of property cannot be more or less than the sources of its formation.

The left side is delimited into 2 sections, the first contains non-current assets, the second - current assets.

The right side of the balance sheet is a liability divided into 3 parts, in which information about reserves, capital and liabilities is consistently recorded.

The procedure for filling out the balance sheet 2017: asset

Fill out the balance form start with the active part. For greater clarity, we offer a tabular version, which indicates in which line of the balance sheet which indicators should be reflected, as well as the rules for summing values:

|

Line code |

Account balances included |

|

|

Section I |

||

|

08 s / account of expenses for search work |

||

|

08 c / expense account of the MC for search work |

||

|

01, 08 s/account of accounting for fixed assets, the commissioning of which has not yet been carried out |

||

|

02 c / account “Depreciation of assets attributable to income. investments" |

||

|

59 c / account "Accounting for reserves for long-term obligations" |

||

|

amounts not included in the previous lines of the section |

||

|

1200: Section I total |

section line sum |

|

|

Section II |

||

|

41,15,16, 97, 10, 11, 43, 45, 20, 21, 23, 29, 44 |

||

|

62, 60, 68, 69, 70, 71, 73 (excluding interest-bearing loans), 75, 76 |

||

|

58, 55 c/account “Deposits”, 73 c/account “Payments on loans” |

||

|

50, 51, 52, 55, 57, 55 c/account "Deposit accounts" |

||

|

the value of assets not included in the listed lines of section II |

||

|

1200:Total for Section II |

section line sum |

|

|

1600: Total asset |

the sum of the results of sections I and II |

|

Filling in the balance sheet for 2017 on the lines of the passive part

|

Line code |

Account balances included |

|

|

Section III |

||

|

83 s/account "Reassessment of fixed assets and intangible assets" |

||

|

83 (except for revaluation of fixed assets and intangible assets) |

||

|

1300: Section III total |

sum of line values in Section III |

|

|

Section IV |

||

|

amounts not included in Section IV lines |

||

|

1400: Section IV total |

sum of lines of section IV |

|

|

Section V |

||

|

60, 62, 68, 69, 70, 71, 73, 75, 76 |

||

|

amounts not included in the previous lines of section V |

||

|

1500: Section V total |

sum of lines section V |

|

|

1700: Total liabilities |

sum of row values Sections III, IV and V |

|

If all balance lines are filled in correctly, the final results of pages 1600 and 1700 will be the same.

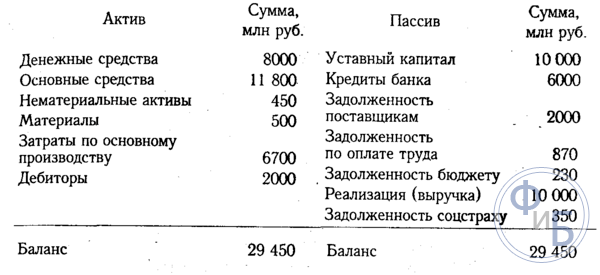

Enterprise balance sheet: completed example 2017

A sample of the balance sheet based on accounting data grouped in the balance sheet of Crocus LLC. To simplify the task, let's assume that the company is organized in 2017 and draws up a balance sheet for 2017 for the first time. The form of the balance sheet for 2017, a sample of which is presented, involves consideration of the results of the company's work for the reporting, past and previous past years. In our example, data for 2017:

account number

Balance

In accordance with the instructions for filling out the form indicated above, based on the credentials, we will fill in the balance sheet for 2017.

An important point in the design of this document is the observance of the mandatory rule of any balance - the equivalence of both parts. In our example, the balance lines were filled line by line as follows:

Account balance

D/t 04 – K/t 05

8700 – 3000 = 5700

D/t 01 – K/t 02

825000 – 443000 = 382000

D/t (10 + 41/2 + 41/3 + 44) – K/t 42

(50000 + 575000 + 33000 + 12500) – 120000 = 550500

D/t (62 + 71 +76)

15000 + 1900 + 40000 = 56900

D/t (50 + 51 + 52 +58)

10000 + 92000 + 7800 +5000 = 114800

K/t (60 + 68 + 69+ 70)

265000 + 57000 + 12000 + 30000 = 364000

The presented example demonstrates the decoding of the balance sheet items for 2017. A sample of filling in the lines shows the simplicity of this work, but it requires care. Drawing up a balance is unique in that errors are detected in the process of work by a mismatch between the values of the active and passive parts, which allows you to quickly correct the situation.

The balance sheet form 2017 (a form with numbered lines for ease of compilation) can be downloaded below.

Form 1 of the balance sheet is the main and, perhaps, the most important component of financial statements. She is judged on financial position organizations. All companies fill it out without exception. Therefore, every self-respecting accountant should know how the balance sheet is filled. In the article we will tell and show how to do it correctly.

The balance sheet of the enterprise - form 1 or 0710001?

The balance sheet was officially called Form 1 until 2011, while the reporting forms approved by order of the Ministry of Finance of the Russian Federation dated July 22, 2003 No. 67n were in effect.

In the order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n, which approved the accounting forms that are relevant now, the concept of “form 1” is not used. Now the forms are coded according to OKUD - All-Russian classifier management documentation (OK 011-93), approved by the Decree of the State Standard of Russia dated December 30, 1993 No. 299. And according to it, the balance sheet code is 0710001.

However, most of us continue to call the balance sheet in the old way - by tradition or for the sake of convenience. After all, any accountant understands what the one who requires form number 1 from him wants to get.

And read about the features of filling out a simplified balance sheet.

The balance sheet (F-1) consists of an asset and a liability, which include sections, each of which contains lines containing data on certain types of property or liabilities.

The asset includes 2 sections:

I. Non-current assets

It contains information about fixed assets, intangible assets, R&D, long-term financial investments, that is, about property that cannot be sold quickly.

II. current assets

These are the so-called short (easily marketable) assets: stocks, receivables with a maturity of up to 1 year, short-term financial investments, cash.

The liability has 3 sections:

III. Capital and reserves

It reflects information about the capital of the organization (authorized, reserve, additional) and retained earnings (uncovered loss).

IV. long term duties

These are obligations with a maturity of more than 12 months (loan, estimated, deferred).

V. Current liabilities

This section provides information on liabilities with a maturity of less than a year, including borrowed funds, accounts payable, estimated and other liabilities.

More about some of the nuances that require consideration when filling out individual lines balance, read this article .

Completing form 1 of the balance sheet in 2018-2019 (sample)

All balance sheet indicators are given for one of the dates:

- reporting date (on obligatory case this is December 31 of the reporting year);

- December 31 of the previous year;

- 31 December of the year preceding the previous one.

Balance lines are encoded. The code is taken from Appendix 4 to Order No. 66n. Given these codes, a sample form 1 of the balance sheet will look like this:

|

Explanations |

Name of indicator |

On ____ 20__ |

|||

|

I. NON-CURRENT ASSETS |

|||||

|

Intangible assets |

|||||

|

Research and development results |

|||||

|

Intangible search assets |

|||||

|

Tangible Exploration Assets |

|||||

|

fixed assets |

|||||

|

Profitable investments in material values |

|||||

|

Financial investments |

|||||

|

Deferred tax assets |

|||||

|

Other noncurrent assets |

|||||

|

Total for Section I |

|||||

|

II. CURRENT ASSETS |

|||||

|

Value added tax on acquired valuables |

|||||

|

Receivables |

|||||

|

Financial investments (excluding cash equivalents) |

|||||

|

Cash and cash equivalents |

|||||

|

Other current assets |

|||||

|

Total for Section II |

|||||

|

III. CAPITAL AND RESERVES |

|||||

|

Authorized capital (share capital, authorized fund, contributions of comrades) |

|||||

|

Own shares repurchased from shareholders |

|||||

|

Revaluation of non-current assets |

|||||

|

Additional capital (without revaluation) |

|||||

|

Reserve capital |

|||||

|

Retained earnings (uncovered loss) |

|||||

|

Total for Section III |

|||||

|

IV. LONG TERM DUTIES |

|||||

|

Borrowed funds |

|||||

|

Deferred tax liabilities |

|||||

|

Estimated liabilities |

|||||

|

Other liabilities |

|||||

|

Total for Section IV |

|||||

|

V. SHORT-TERM LIABILITIES |

|||||

|

Borrowed funds |

|||||

|

Accounts payable |

|||||

|

revenue of the future periods |

|||||

|

Estimated liabilities |

|||||

|

Other liabilities |

|||||

|

Section V total |

|||||

For a sample of filling out the balance sheet of the full form, created on specific numbers, see the article "The procedure for compiling the balance sheet (example)" .

Where can I download form 1 (F-1) of the balance sheet?

You can download form 1 of the balance sheet on the website of any of the legal reference systems. There are also examples and samples of filling out this document.

Templates for all forms of financial statements are also available on the website of the Federal Tax Service of the Russian Federation in the "Tax and Accounting Reporting" section.

In addition, the form of the balance sheet (officially existing in 2 versions) can also be found on our website, in the material "Form of the balance sheet of the enterprise (download)".

Results

The preparation of the balance sheet is carried out on a form of a certain form, approved for this by the Ministry of Finance of Russia, and in compliance with certain rules for entering information into it. Forms and examples of filling out the balance can be found on the websites of legal reference systems, the website of the Federal Tax Service and on our website.

All legal entities are required by law to keep accounting records and, therefore, submit annual financial statements. The main document of such a report is form 1 "Balance sheet". You can download the form (word) and learn about the requirements for its preparation from this article.

As required Federal Law of December 6, 2011 No. 402, all organizations are required to keep records and generate financial (accounting) statements at the end of the year. The package, which at the end of the year must be submitted to Rosstat and the Federal Tax Service, and provided to the owners of the organization at their request throughout the year, also includes a balance sheet. Let's figure out what form you need to use to compile it, what features this report has, and also what an "asset" and "passive" are.

Balance sheet (form 1), form 2019

The balance sheet form valid for the report for 2017 was approved by order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n. It has not changed since the reporting date for 2011. In general, changes in financial statements contribute less frequently than to the tax, because the basic requirements and accounting indicators rarely change. It is necessary to hand over the balance sheet at the end of the year before March 31 of the year following the reporting one. In addition, the form is useful for compiling a report for founders, shareholders or, for example, a bank when obtaining a loan.

However, not all organizations should use it. For small businesses, a simplified reporting form is provided, which includes a significantly shortened balance sheet. The truncated form lacks many of the lines provided in the full version. In this case, explanations are required in both cases. They are not included in the report form and are compiled arbitrarily with the decoding of the necessary lines and indicators.

Assets and liabilities

Any balance sheet of an organization, both full and reduced, always consists of two equal parts:

- assets;

- passive.

It is because these two halves should be equal to each other that the document got its name.

The asset reflects:

- the cost of fixed assets of the organization;

- the value of other property belonging to it (materials, raw materials, goods, IBE, etc.);

- debt to the organization of counterparties (accounts);

- intangible values;

- cash in bank accounts and in circulation.

The liability reflects all the obligations of the company and attracted funds (loans, investments, deposits). It includes accounts payable and expenses. All data in the balance sheet is tightly linked to other accounting registers and the general ledger.

Form and procedure for filling

All organizations fill out a balance sheet with line codes, the form of which is approved by law. The document is quite simple and consists of a title part and five sections:

- Section I "Non-current assets", in which you should specify residual value fixed assets of the company, cost intangible assets, as well as long-term financial investments and other non-current assets.

- Section II "Current assets". Accounts containing information on commodity stocks are grouped here, and short-term balances must also be indicated here. financial investments, receivables and cash balances in cash and bank accounts.

- Section III "Capital and reserves" is intended to indicate information about the amounts of authorized and other capital, here you should also indicate the amount of retained earnings or uncovered loss.

- Section IV "Long-term liabilities" will tell about the amounts long-term loans and other obligations of the company.

- Section V "Current Liabilities" contains information on the amount of loans and borrowings received for a period of up to one year, and accounts payable.

The first two sections are the asset balance, and the rest are liabilities. You need to fill in the data based on the balance on the desired date from the general ledger. Some rows contain information on several accounts at once. An explanatory note is used to detail the data. The completed form looks like this:

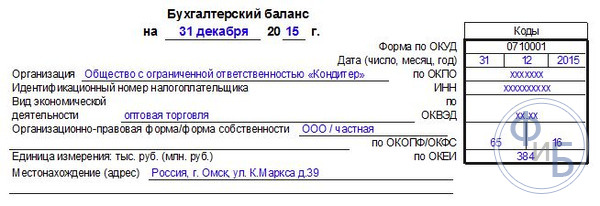

In the title part, we indicate the date on which the information is indicated, the name of the organization, the address, as well as all codes (TIN, OKPO). You should also indicate the legal form and type of activity in accordance with the new OKVED.

The balance in the annual report is indicated for three years:

- current;

- December 31 last year;

- December 31 of the year before last.

This is necessary for comparison. In addition, in the first column it is necessary to note the number of the paragraph of the explanations deciphering this line. If there are no explanations for the line, this field should be left blank.

The head of the organization signs the report and sets the date of its compilation.