1c 8.2 currency revaluation settlements with counterparties. Revaluation of foreign exchange balances

In the course of their activities, Russian organizations have the right to open bank accounts, including foreign currency ones, to acquire assets for foreign currency with the formation of debt obligations. However, tax and accounting records are carried out exclusively in local currency. Revaluation of foreign currency balances reflects the real financial condition of the company.

What is the revaluation of foreign exchange funds

Considering that Russian ruble- this is the only currency allowed in the accounting of organizations, the assessment of all operations must be carried out in rubles. The same applies to bank accounts, even if they are created for settlements in foreign currency... Also, revaluation currency funds carried out in the presence of the following operations:

- cash settlements in cash and non-cash forms;

- other monetary documents, whose face value is expressed in the currency of foreign countries;

- financial foreign exchange investments;

- debt of debtors and organizations to creditors expressed in foreign currency;

- foreign exchange investments in material values and other assets.

The revaluation of foreign currency balances is carried out in accordance with the norms of PBU 3/2006, which oblige to account for assets and liabilities denominated in foreign currencies according to certain rules. The frequency of recalculation depends on the type of asset. For example, banks are required to revalue foreign exchange funds on a daily basis according to the prevailing exchange rate. Other organizations are not required to carry out daily revaluation, it is enough to carry out such transactions at the end of the period in the accounting. Asset revision dates may coincide with the following events:

- carrying out operations;

- end of the period (last day of the month).

Currency revaluation in accounting

Considering that the value of the Russian ruble in relation to foreign currencies is constantly changing, revaluation leads to the appearance of such a phenomenon as exchange rate differences. As a result, enterprises have additional income in case of a positive result, or losses arise in case of negative exchange rates. The resulting differences are credited to account 91 and classified as other income or expenses, depending on the result.

What does the revaluation of foreign currency means of transactions create? Obtaining a positive exchange rate difference is recorded as follows: Дт 57 - Кт 91.1. Negative value for currency translation: Дт 91.2 - Кт 57.

An entity's purchase and revaluation of the transaction currency assumes the following:

- Dt 57 - Kt 51 - the cost of purchasing currency;

- Дт 52 - Кт 57 - replenishment of the foreign currency account;

- Dt 91.2 - CT 57 - fixing the resulting difference based on the results of the sale of foreign currency by the bank and current rate Central Bank;

- Dt 52 - CT 91.1 - identification of a positive exchange rate difference;

- Dt 91.2 - CT 52 - negative difference.

Implementation Money foreign countries assumes that the revaluation of a foreign currency account generates the following entries:

- Дт 57 - Кт 52 - currency debiting from the account;

- Дт 57 - Кт 91.1 - a positive exchange rate difference is formed;

- Dt 91.2 - CT 57 - the formation of a negative exchange rate difference;

- Дт 51 - Кт 57 - proceeds from the sale were received on the ruble account;

- Dt 91.2 - CT 57 - the difference between the bank rate when buying foreign currency and the current rate of the Central Bank was recorded.

Settlements in foreign currency with other parties are recalculated at the current exchange rate of the Central Bank on the day of the transaction:

- Дт 52 - Кт 62 - receipt of proceeds in foreign currency;

- Dt 52 - Kt 66, 67 - funds received as a foreign currency loan;

- Дт 52 - Кт 75, 76 - receiving funds from founders and other persons;

- Дт 60, 66, 67, 75, 76 - Кт 52 - foreign exchange funds were spent to pay off obligations.

If the entity owns some assets located abroad, they also need to be appraised at the end of the period. The parent enterprise is obliged to prepare reports in rubles.

Currency revaluation in tax accounting

When conducting tax accounting at the enterprise, the revaluation of foreign currency accounts and other assets is also important. The dates for performing actions are the same moments as in accounting - on the day of the transaction and at the end of the period.

The results of the translation of foreign currency assets include events:

- The appearance of a positive exchange rate difference. Increases the company's income and, accordingly, the taxable base when calculating income tax.

- The negative exchange rate difference is included in other expenses. Considered as non-operating costs in determining income tax.

For enterprises using the simplified tax system, there are slightly different rules for using the results of the revaluation of funds. The presence of positive differences in the conversion of the exchange rate affects the increase in the simplified tax. However, the costs received as a result of negative differences when converting currencies by organizations on the STS are not taken into account.

The translation of foreign currency assets into Russian rubles affects the final financial results... In this case, it is necessary to adhere to the rate of the Central Bank in effect on the date of revaluation.

2017-05-20T12: 15: 02 + 00: 00Why do you need " Currency revaluation"? I am often asked this question by novice accountants, because they have not yet encountered currency transactions in practice and do not understand where this revaluation comes from, how it is calculated and whether it is needed. Let's deal with this once and for all using the example of 1C: Accounting 8.3. , revision 3.0. First, the revaluation occurs "by itself" when closing of the month.

Secondly, it only arises for organizations that have had currency transactions.

And that's why.

According to PBU 3/2006 on accounting for assets and liabilities, the value of which is expressed in foreign currency, we have:

The value of assets and liabilities denominated in foreign currency for accounting purposes and accounting statements to be converted into rubles.

The translation of the value is made at the date of the transaction in foreign currency, as well as at reporting date.

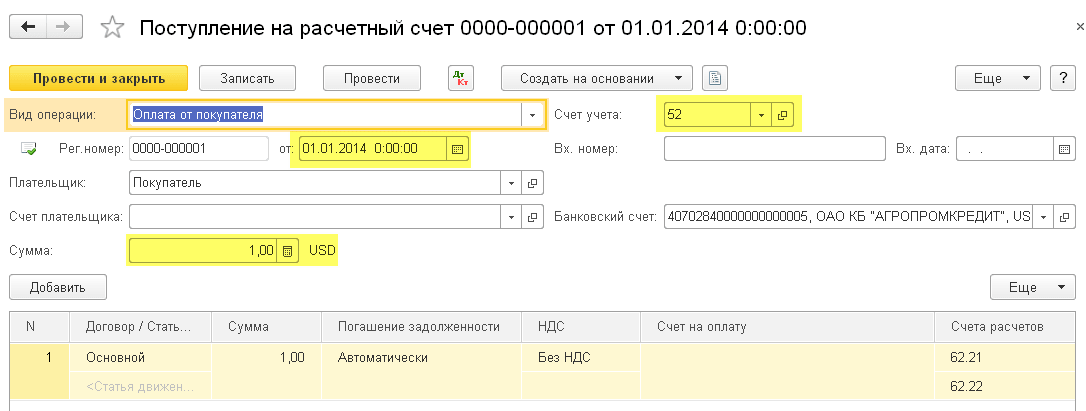

01.01.2014 the buyer transferred to our current account 1 dollar.

The wiring will be as follows:

D52 K62 1 USD (32.6587 rubles)

Please note that we recorded the transaction amount simultaneously in the transaction currency (1 dollar) and in rubles at the exchange rate on the date of the transaction (on January 1, 2014, the dollar exchange rate was exactly 32.6587 rubles).

It turns out that all foreign currency accounts keep their monetary indicators in two dimensions at once: in the account currency and in rubles (the main currency of the regulated accounting for Russia).

Thus, at the end of the day on 01/01/2014, the balance on account 52 will be 1 USD and at the same time 32.6587 rubles.

Everything is fine, but time goes by. The dollar exchange rate is changing. And already at the end of the month (01/31/2014) for one dollar they give 35.2448 rubles.

And, if we look at our balance on account 52 at the end of the month, we will see that despite the fact that the rate has changed there is still 1 USD and 32.6587 rubles. But we know that one dollar no longer corresponds to 32.6587 rubles, but 35.2448 rubles! Arose mismatch between the amount of the balance in dollars and the amount of the balance in rubles.

So, this very recalculation of the value of assets and liabilities in foreign currency for the reporting date (that is, monthly) was just invented in order to restore this correspondence between currency and rubles every time at the end of the month.

In this case, the revaluation for account 52 as of 01/31/2014 will look like this:

D52 K91.01 2.5861 rubles

Thus, we have revalued the ruble balance on account 52 by 2.5861 rubles from other income. It turns out that the course has grown over this month - hence the income for the organization. If the exchange rate fell, on the contrary, there would be other expenses.

So, after the revaluation, the debit balance on account 52 at the end of the day on 01/31/2014 will be 1 USD and at the same time 35.2448 rubles.

But time goes by. And at the end of February for 1 dollar they already give 36.0501 rubles. This means that we again had a discrepancy between dollars and rubles on account 52, and at the same time there was other income due to the increase in the exchange rate for February.

The new revaluation will give the following postings:

D52 K91.01 RUB 0.8053

And the debit balance on account 52 at the end of the day on 02/28/2014 will be the same 1 USD and at the same time 36.0501 rubles.

And so we will overestimate indefinitely, as long as we have a non-zero remainder at 52 counts. Other foreign currency accounts are revalued in the same way.

Here is a brief theory of the revaluation of foreign exchange funds in accounting... Now let's see how this is all implemented in the program using the example of 1C: Accounting 8.3 (revision 3.0):

We load the exchange rates for 2014

Setting up a currency account (USD)

To do this, go to the "Main" -> "Organizations" section and open our organization there ():

In the organization card in the top panel, select the "Bank accounts" item:

In the list of accounts that opens, click the "Create" button and fill in the current account card as follows (account number and BIC are indicated as an example; be sure to select the account currency USD):

Click "Save and Close".

We make the receipt of funds from the buyer

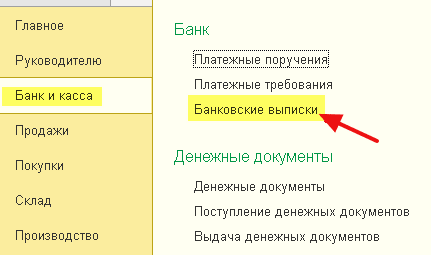

To do this, go to the "Bank and Cashier" section and select the "Bank statements" item () there:

Press the button "Receipt" and fill in bank statement as follows (receipt of $ 01 01/01/2014; from any counterparty under any contract; accounting account - 52; bank account - the one that we just created):

Click "Post and Close".

We look at the document transactions (the DtKt button in the statement journal):

We see that 1 dollar was capitalized on account 52 at the rate as of 01/01/2014 (about how to view exchange rates for a specific date in 1C: Accounting).

Closing the month for January

We go to the "Operations" section and select the "Close of the month" item () there:

Select the period January 2014 and click "Perform month closing".

Then we find the item "Revaluation of foreign exchange funds", click on it and select "Show transactions":

Here is our exchange rate difference of 2.58 rubles:

Let's go back to the close of the month for January 2014 and find the "Help-Calculations" button there. Click on it and select the item "Revaluation of foreign exchange funds":

The program will generate a report with calculations for the revaluation of foreign exchange funds:

Do the month close for February in the same way to make sure our preliminary calculations match the behavior of the program.

We are great, that's all

If this does not help, then it is very likely that the account for which you expect the calculation of the exchange rate difference is entered in your list of accounts with a special revaluation procedure.

Dt 52.2 Current foreign currency account 3000 US dollars x 23 rubles.

Кт 52.1 Transit currency account 75 kopecks. == RUB 71,250

On account 52.1, an exchange rate difference arose in the amount (23 rubles 75 kopecks - 23 rubles) x 9000 USD = 6750 rubles.

Dt 52-1

Kt 80, subaccount "Exchange rate differences" 6750 rubles.

3. The ruble proceeds from the obligatory sale of foreign currency are credited to the settlement account of the organization (6,000 US dollars x 23 rubles 50 kopecks = 141,000 rubles)

Dt 51 Current account

Kt 48 Sale of other assets 141,000 rubles.

Written off to the cost of sales of the sold soum of foreign currency at the exchange rate of the Central Bank of the Russian Federation on the day of sale

Dt 48 Sale of other assets USD 6,000 x RUB 24 = 144,000 rubles.

CT 57 Transfers on the way

The financial result from the mandatory sale of a part of foreign exchange earnings is determined

Dt 3000 rub. (144,000 - 141,000)

The financial result is the difference between the exchange rate (selling rate) and the rate The central bank RF at the date of sale.

On account 57 “Transfers on the way” there was an exchange rate difference in the amount (24 rubles - 23 rubles 75 kopecks) x 6000 US dollars = 1500 rubles.

It arose due to the difference between the exchange rate of the Central Bank of the Russian Federation on the date of sale and on the date of deposit of currency subject to mandatory sale.

For the amount of the exchange rate difference in accounting, a posting is made:

CT 80, subaccount "Exchange differences". 1500 rbl

According to the aforementioned Instruction of the Central Bank of the Russian Federation of June 29, 1992 No. 7 (subject to subsequent amendments and additions), organizations can also voluntarily sell from a transit currency account in excess of the amounts subject to mandatory sale.

Thus, the obligatory sale is made only from the transit currency account of the organization, and the voluntary sale is made both from the current and from the transit currency account.

SALES OF EXPORT PRODUCTS UNDER THE AGREEMENT OF THE COMMISSION WITH THE RUSSIAN INTERMEDIARY

In its term paper I will only consider the accounting with the principal.

1.Under a commission agreement, an export consignment of goods was shipped to be sent to the address of a foreign buyer:

Dt 45.1 subaccount "Goods shipped for export"

CT 40.1 Finished products export RUB 100,000

2. Paid overhead costs in rubles:

Dt 43.1

CT 51RUB 40,000

3. After the goods have been shipped to the address of the foreign buyer from the por-ga or from the border railway point, the intermediary must notify the supplier of this.

According to the Instruction of the Ministry of Finance of the Russian Federation "On the procedure for filling out the forms of annual financial statements", approved by Order of the Ministry of Finance of the Russian Federation No. 97 dated November 12, 1996 (durable document), the implementation of the following is reflected as of the date of receipt of the notification:

Dt 62.2 Settlements with commission agents USD 9,000 х 22

for the supplied export goods rub. 50 kopecks (the rate of the Central Bank of the Russian Federation on the date of receipt

CT 46.1 Sale of export goods, notifications) = 202500 rubles. works, services

At the same time, the amount of expenses paid by the commission agent in foreign currency and the commission are charged to the expenses of the principal; by this amount, the debt of the commission agent to the commissioner is reduced ($ 1000 - overhead costs and $ 800 - commission to the intermediary):

Dt 43.2 1800 USD x 22 rubles. 50 kopecks = RUB 40,500

The cost of the shipped goods and the costs of its sale are written off to the sale:

Dt 46.1

Kt 45.1 100 000 rubles.

Dt 46.1

CT 43.1 RUB 40,000

Dt 46.1

CT 43.2 40 500 rubles.

The financial result from the implementation is determined:

Dt 46.1

Kt 80 22,000 rubles.

4.a) The rest of the foreign exchange earnings is transferred by the commission agent to the consignor's foreign exchange account in transit:

Dt 52.1 7200 USD at the exchange rate of the Central Bank of the Russian Federation

CT62.2 on the date of enrollment

A compulsory sale is issued. Mandatory Sale 7,200 x 0.75 = $ 5,400. $ 1,800 is credited to the current foreign currency account.

Dt 57 5400 USD at the exchange rate of the Central Bank of the Russian Federation

CT 52.1 on the date of withdrawal

CT 52.1 on the date of transfer

Dt 51 Ruble proceeds from

CT 48 compulsory sale

Kt 57 at the exchange rate of the Central Bank of the Russian Federation on the date of sale

or Financial result from

Dt 48 compulsory sale

Dt57

CT80

or Exchange rate difference

Dt80

b) The compulsory sale was drawn up by a commission agent:

Dt 52.2 1800 USD at the exchange rate of the Central Bank of the Russian Federation

CT 62.2 on the date of enrollment

Dt 51 Ruble proceeds

Kt 48 per sold currency

Dt 48 Ruble equivalent of sold currency

CT 62.2 at the exchange rate of the Central Bank of the Russian Federation on the date of sale

or Financial result from a mandatory sale

Exchange rate difference on account 62.2 "Settlements with commission agents for delivered export goods":

Dt 62.2

CT80 or

CT 62.2

Bank commission for compulsory sale is written off to the debit of account 48, but does not reduce taxable profit.

It should be noted that in accordance with the "Law on VAT" exporters have a privilege to pay this tax in the amount of 100% of the value of exported goods (works, services).

4. ACCOUNTING OF IMPORT OPERATIONS

ACCOUNTING OF IMPORT OPERATIONS UNDER A DIRECT CONTRACT BETWEEN A RUSSIAN BUYER AND A FOREIGN SUPPLIER OF IMPORTED GOODS

In this section, the term "imported goods" means any material values that, when imported into the territory of the Russian Federation, cross its border without an obligation to re-export.

When recording operations for the import of goods, it is necessary, firstly, to put the imported goods on the balance sheet in a timely manner, and secondly, to correctly form the actual cost of the imported goods on the accounting accounts, which will be its cost in case of further use - writing off to production or implementation.

The goods must be put on the balance sheet from the moment of transfer of ownership of it to the importer. In accordance with the PBU, it is the date of transfer of ownership to the importer that is the date of the operation for the import of goods. On this date, you need to take the rate of the Central Bank of Russia to convert the amount of foreign currency into rubles, in which the value of the goods is expressed.

The date of the transfer of ownership from the seller to the buyer should be indicated in the contract, since there is no international law on this issue, and the existing international practice, according to which the moment of transfer of ownership of goods is considered the seller's fulfillment of his delivery obligations, is not a convincing argument in disagreement with the inspectors.

Economic sciences / 7.Accounting and audit

Ph.D. Demyanenko E.Yu.

Rostov State University of Economics (RINH), Russia

Differences in the revaluation of foreign currency balance sheet items under RAS and IFRS

In accordance with the requirements of Federal Law No. 402-FZ "On Accounting", organizations maintain accounting records in foreign currency Russian Federation- rubles. But in cases where foreign partners act as counterparties, companies cannot do without currency transactions... Currency transactions between residents and non-residents are carried out without restrictions, and their conduct is regulated Federal law No. 173-FZ “On currency regulation and currency control”.

The main document defining the principles of reflecting transactions in foreign currency in accounting is PBU 3/2006 "Accounting for assets and liabilities, the value of which is expressed in foreign currency".

The procedure for determining and recording exchange differences is set out in IAS 21 “The Effect of Changes exchange rates". This standard applies:

- when accounting for transactions and balance sheet balances in foreign currency, with the exception of transactions and balances with derivative financial instruments (regulated by IAS 39 “ Financial instruments: reflection and evaluation ");

- when recalculating results economic activity and financial condition foreign organizations that are included in the financial statements of a company that prepares these statements using the consolidation method, proportionate consolidation or equity participation;

- when translating the results of operations and financial condition of the company into the presentation currency.

Note that the scope of PBU 3/2006 is significantly narrower than the scope of IAS 21, since it only applies to individual reporting organizations and only when converting operations into Russian rubles.

Restating the cost of an asset or liability for purposes accounting is made at the official rate of foreign currency to the ruble, established by the Bank of Russia, or at another rate established by law or by agreement of the parties (terms of the agreement).

The first ruble measurement of an asset or liability arises on translation of its cost at the date of receipt.

Subsequent ruble valuations are formed when recalculating its value as the exchange rate changes at the reporting date or at the date of the obligation fulfillment.

The need to recalculate assets and liabilities into rubles from the point of view of RAS 3/2006 is in no way linked to the specifics of the organization's economic activities. In fact, PBU 3/2006 says that the functional currency for all Russian organizations is the Russian ruble.

IAS 21 does not specify which rate should be used when translating assets and liabilities. Whereas PBU 3/2006 establishes that in the general case (if the parties have not agreed on a special settlement rate), the recalculation is carried out using the rate of the Central Bank of the Russian Federation.

Also, IAS 21 allows the use of the average rate for a certain period, if it has not been subject to significant fluctuations. An average weekly or monthly rate can be used for all foreign currency transactions carried out in this period. However, in the event of significant fluctuations in exchange rates, the use of the average rate for the period seems inappropriate. When revaluing at the reporting date, if there are more than one exchange rate, the one at which the transaction could have been calculated at the revaluation date is used. If the possibility of exchange between two currencies is temporarily unavailable, the first subsequent rate at which the exchange can be made is used as the exchange rate.

When forming a new ruble valuation of an asset or a liability denominated in foreign currency, exchange rate differences arise.

The exchange rate difference is understood as the difference between the ruble valuation of an asset or liability, the value of which is expressed in foreign currency, at the date of fulfillment of payment obligations or at the reporting date of this reporting period and the ruble valuation of the same asset or liability as of the date of its acceptance for accounting in reporting period or as of the reporting date of the previous reporting period (clause 3 of PBU 3/2006).

The definition of exchange differences in IAS 21 is broader. So, in accordance with it, the exchange rate difference is the difference arising from the conversion of the same number of units of one currency into another currency at different exchange rates.

Also, IAS 21 contains definitions of concepts that are absent in PBU 3/2006 due to a narrower scope of application, as well as different accounting rules.

For example, the concept of a functional currency is used (from the point of view of PBU 3/2006, all transactions, assets and liabilities are subject to conversion into rubles). Functional currency is the currency used in the primary economic environment in which an entity operates. The main feature of a functional currency is its use by an organization in its main economic environment. Basic economic environment is the environment in which an entity generates and spends the bulk of its cash. In determining the functional currency, the following factors are taken into account: the currency that has a major influence on the selling prices of goods and services; the currency of the country, the market and legislation of which mainly determine the formation of prices for goods and services of the organization; currency, which mainly affects labor, material and other costs.

Additionally, the following factors can be taken into account: currency in which funds from the issue of debt and equity instruments are received; the currency in which proceeds from operating activities are usually accumulated. If, based on the above factors, the functional currency is not obvious, management of the entity, based on its own experience, determines the functional currency that most accurately represents the economic effects of the underlying transactions, events and operating conditions.

For example, if a Russian parent company has a subsidiary that is located in the United States, it manufactures and markets its products, and transactions with the parent company represent a minor proportion of the subsidiary's activities. In this case, since it is the US dollar that will have a significant impact on the selling price of products, labor, material and other costs associated with the provision of goods, it is he who will act as the functional currency of the subsidiary.

Exchange rate differences, in turn, are positive and negative.

According to clause 7 of PBU 9/99 "Income of the organization", the exchange rate difference is recognized as positive and is referred to other income:

- with an increase in the exchange rate in relation to assets (claims);

- when the exchange rate depreciates in relation to liabilities.

In accordance with clause 11 of PBU 10/99 "Expenses of the organization", the exchange rate difference is recognized as negative and is referred to other expenses:

- in case of a depreciation of the currency in relation to assets (claims);

- with an increase in the exchange rate in relation to liabilities.

To reflect the results of foreign exchange transactions in the accounting of the organization, they initially calculate their value in ruble terms, for this: the exchange rate of foreign currency against the ruble is determined as of the date of recalculation upon the fact of the transaction in foreign currency, namely at the moment of recognition of its results in accounting; the cost of a foreign exchange operation is formed in the ruble equivalent as the product of the value of an asset or liability, expressed in foreign currency, by its rate; records in the amount of the formed ruble value of the currency operation are posted to the accounting accounts.

The specified translation into rubles should be made at the date of the transaction in foreign currency, as well as at the reporting date. For the purpose of revaluation, accounting items denominated in foreign currency are divided into two groups:

1) monetary balance sheet items that combine cash on hand, in bank accounts, in settlements, as well as liabilities and securities, the circulation period of which is determined by the framework of the reporting year;

2) non-monetary balance sheet items, which are considered accounting items other than monetary items.

As a result of changes in the official exchange rate of foreign currency against the ruble used in the calculations, the exchange rate difference is recognized:

- as of the reporting date of the current period in relation to the date of the transaction on monetary items;

- as of the date of fulfillment of payment obligations in the reporting period and as of the previous reporting date for monetary items;

- at the previous reporting date and at the reporting date of the current period, when transactions in foreign currency were not carried out in this period;

- on the date of occurrence of obligations in accounting and on the date of fulfillment of obligations to pay them or on the reporting date in which these obligations were recalculated for the last time, as well as if they are recognized and settlements on them are made in the same reporting period.

The exchange difference is credited depending on the nature of the currency transaction:

1.Financial results for all current operations(clause 13 PBU 3/2006):

- Debit 50 "Cashier", etc. (52, 57, 58, 60, 62, 66, 67, 71, 86) Credit 91 subaccount 1 "Other income" - a positive exchange rate difference is reflected;

- Debit 91 subaccount 2 "Other expenses" Credit 50 "Cashier" and others (52, 57, 58, 60, 62, 66, 67, 71, 86) - negative exchange rate difference is reflected;

2. for additional capital on operations related to the formation of the authorized (share) capital (clause 14 of PBU 3/2006):

- Debit 75 "Settlements with founders" Credit 83 "Additional capital" - a positive exchange rate difference is reflected.

- Debit 83 "Additional capital" Credit 75 "Settlements with founders" - a negative exchange rate difference is reflected.

IAS 21 does not provide for the reflection of exchange differences associated with settlements with founders on contributions to authorized capital as part of additional capital. These exchange differences are recognized in profit (loss) for the period in accordance with the generally established procedure.

PBU 3/2006 does not regulate the accounting for the foreign exchange component in relation to profit (loss) arising from non-monetary items. At the same time, due to the peculiarities of accounting in RAP, a foreign exchange component does not arise in relation to such transactions.

Foreign exchange differences on monetary items are recognized in profit or loss of the organization. When a gain or loss on a non-cash item is recognized directly in equity (for example, a gain or loss on revaluation of property, plant and equipment), any foreign currency component of that gain or such loss is recognized directly in equity. When a gain or loss on a non-cash item is recognized in profit or loss, any foreign currency component of that gain or that loss is recognized in profit or loss.

Note also that, unlike IAS 21, PBU 3/2006 requires separate disclosures in relation to exchange differences arising from transactions denominated in foreign currency but payable in rubles and exchange differences arising from transactions actually carried out in foreign currency. currency. PBU 3/2006 also requires disclosure of information on the exchange rate of the Central Bank of the Russian Federation as of the reporting date. IAS 21 requires additional disclosures when the presentation currency differs from the functional currency or when the entity uses another currency to present financial information.

Literature:

1. Regulation on accounting "Accounting for assets and liabilities, the value of which is expressed in foreign currency" (PBU 3/2006) (approved by order of the Ministry of Finance of the Russian Federation dated November 27, 2006 No. 154n, as amended on December 24, 2010 No. 186n).

2. Regulation on accounting "Income of the organization" (PBU 9/99) (approved by order of the Ministry of Finance of the Russian Federation dated 06.05.1999 No. 32n, as revised on 06.04.2015 No. 57n).

3. Regulations on accounting "Organization's expenses" (PBU 10/99) (approved by order of the Ministry of Finance of the Russian Federation dated 06.05.1999 No. 33n, as revised on 06.04.2015 No. 57n).

4. International standard financial statements(IAS) 21 "The Impact of Changes in Exchange Rates" (Appendix No. 13 to Order of the Ministry of Finance of the Russian Federation No. 160n dated November 25, 2011, as revised on August 26, 2015 No. 133n).

In principle, the actual goods purchased for foreign currency are accepted for accounting in the same way as goods purchased for rubles. But payments in foreign currency, which in this case take place, certainly have their own characteristics. Accounting for foreign exchange transactions in accounting is regulated by the Accounting Regulations “Accounting for Assets and Liabilities, the Value of which is Denominated in Foreign Currency” (PBU 3/2006), approved by order of the RF Ministry of Finance dated November 27, 2006 No. 154n. Changes concerning foreign exchange transactions, which came into force in 2007, introduced some inconsistencies between accounting and tax accounting, since since 2007 the concept of "sum differences" has been excluded from accounting, while in the Tax Code of the Russian Federation such a concept is still remains.

So, according to the requirements of the legislation, the value of all assets, expressed in foreign currency, including the value of inventories, "... for reflection in accounting and financial statements must be recalculated into rubles" (clause 4 of PBU 3/2006). Consequently, the law does not allow accounting in any currency other than Russian rubles. Liabilities denominated in foreign currency that arise from the purchasing organization to the supplier should be reflected in the accounting records in the ruble equivalent. The recalculation of the obligations arising from the purchasing organization to the supplier when purchasing goods for foreign currency (i.e. conversion) is carried out at the rate determined by the supply agreement (agreement of the parties). If the exchange rate is not fixed in the terms of the agreement, the conversion is carried out at the rate set by the Central Bank of the Russian Federation at the time the obligations arise. According to clauses 9 and 10 of PBU 3/2006, inventories (in our case, goods) are accepted for accounting in an estimate in rubles at the exchange rate in effect at the time of the transaction in foreign currency, and are not subject to further revaluation due to a change in the exchange rate. The situation is different with the obligation to pay for this product. The purchasing organization must recalculate its obligations (accounts payable to the supplier) at the date of fulfillment of the obligations or at the reporting date (whichever comes first). This is relevant in the case when settlements are carried out at the rate of the Central Bank of the Russian Federation or when the supply agreement for some reason establishes a “floating” rate of the settlement currency. If the exchange rate is determined by the agreement of the parties and is unchanged, the difference when recalculating the obligations, of course, will be equal to zero. The difference between the ruble value of the obligation, the value of which is expressed in foreign currency, as of the date of fulfillment of payment obligations or the reporting date of the reporting period, and the ruble value of the same obligation as of the date of its acceptance for accounting in the reporting period or the reporting date of the previous reporting period (last revaluation) is called the exchange rate difference. This difference is taken into account by the buyer on account 91 "Other income and expenses". If it is negative, that is, it is accounted for in the debit of account 91.2 "Other expenses", its amount is taken to expenses that reduce the taxable base for income tax (this applies to both accounting and tax accounting). A positive exchange rate difference is accounted for on the credit of account 91. 1 "Other income" as other income of the enterprise.

For example, suppose an organization purchases a $ 1,000 item from a vendor. For recalculation, the rate of the Central Bank is used. The goods were accepted for accounting on the twentieth, when the dollar exchange rate was 26.78 rubles. Thus, the buyer has before the supplier accounts payable(in terms of) 26 780 rubles.

Payment for the goods has not been made by the end of the month (i.e., by the end of the reporting period). On the thirtieth day, on the last day of the month, the US dollar exchange rate was set by the Central Bank at 26.52 rubles. The accountant of the purchasing company made a revaluation of the liabilities, and at the end of the reporting period it amounted to 26,520 rubles. As a result, there was an exchange rate difference in the amount of 260 rubles. In accounting, it is reflected in the following entry:

Debit of account 60 "Settlements with suppliers and contractors",

Credit of subaccount 91.1 "Other income" - 260 rubles. - reflected the exchange rate difference at the end of the reporting period.

Payment for the item was made on the 7th next month when the US dollar exchange rate was set by the Central Bank 26.60 rubles. Consequently, at the time of fulfillment of obligations, the buyer's debt to the supplier amounted to 26,600 rubles. As a result of the revaluation, there was a negative exchange rate difference in the amount of 80 rubles. In accounting, this is reflected as follows:

Debit of subaccount 91.2 "Other expenses",

Credit account 62 "Settlements with buyers and customers" - 80 rubles. - the exchange rate difference at the time of fulfillment of obligations is reflected.

Thus, the buyer capitalized the purchased goods in the amount of 26,780 rubles, and paid the supplier in the amount of 26,600 rubles.

In addition, in order to pay for the goods in currency, the purchasing organization, in cases where it does not have its own currency or it is not enough, must buy the required amount. Currency is purchased at the exchange rate set by the bank. As a rule, this rate is higher than the one set by the Central Bank. Thus, the currency is acquired at a rate that exceeds the rate at which the payment will be made, and a difference arises in accounting again. Until 2007, this difference was called the sum difference. As we said above, at present this concept is excluded from accounting, but remained in the tax one. In accounting, we can accept this difference as exchange rate difference, since PBU 3/2006 does not provide for a rigid link between the concept of exchange rate difference and the rate of the Central Bank. Exchange rate, established by the bank selling currency, can be recognized as the rate established by agreement of the parties, that is, an agreement between the bank and the organization that purchases the currency. Thus, the financial result from the purchase of currency (that is, the difference between the amount for which the currency was purchased and the amount transferred to the supplier), the buyer can also be attributed to account 91. Suppose that on the seventh day of the buying organization to settle with the supplier it took $ 1000 to purchase. The exchange rate of the bank from which the currency was purchased was 26.70 rubles on that day. Thus, 1,000 US dollars was purchased by the buyer from the bank for 26,700 rubles, and settlements with the supplier in ruble terms amounted to 26,600 rubles. The negative financial result from the purchase of foreign currency amounted to 100 rubles. In accounting, this will be reflected in this way:

Debit account 57 "Transfers in transit",

Credit from account 51 "Settlement accounts" - 26,700 rubles. - money is transferred to purchase currency;

Debit of account 52 "Currency accounts",

Credit account 57 "Transfers on the way" - 26 600 rubles. - purchased currency for settlements with the supplier;

Debit of account 62 "Settlements with buyers and customers",

Credit of account 52 "Currency accounts" - 26 600 rubles. - the payment was transferred to the supplier;

Debit of account 91.2 "Other expenses",

Credit of account 57 "Transfers on the way" - 100 rubles. - the financial result from the purchase of foreign currency is reflected.

⇒Courses Stimulus ›Directory› Useful materials ›1C: Enterprise 8.2› Accounting for Ukraine ›Closing the period and ...

1C: Enterprise 8.2 /

Accounting for Ukraine /

Period-end closing and reporting

Revaluation of currencies

Operation "Revaluation of foreign exchange funds" in accounting is intended to recalculate the value of all accounts for which foreign exchange accounting is carried out, these accounts do not include accounts that are non-monetary listed in the information register "Non-monetary accounts". For the calculation and reflection in the accounting of exchange rate differences, the following must be carried out:

· Establishment of exchange rates for the last date of the period, which ends in the register "Currency rates"

Determination of the account for accounting for income and expenses from exchange rate differences and their values analytical accounting in the information register "Exchange rate differences accounting parameters".

Consider this operation "Revaluation of foreign exchange funds" in the generated document "Close of the month" on

Printable form for this operation "Help-calculation":

In tax accounting, you can perform a revaluation book value cash and non-cash foreign currency debt under agreements with the "Other" type and the "Revalued" feature. As a result, the exchange rate difference will be received, which is included in the income (expenses).

Other materials

Russian organizations have the right, without restrictions, to open foreign currency accounts with banks that have the appropriate license. The presence of a foreign currency account with a Russian organization, on which funds are registered, entails the need for periodic revaluation of foreign currency balances on it, regardless of the purposes for which it was opened. This is due to the fact that all obligations on the territory of our country are fulfilled in rubles. Accounting is also kept in the national currency of Russia: both accounting and tax. Let us consider the features of such a revaluation in the context of accounting and tax accounting.

Currency revaluation in accounting

Regardless of the foreign currency in which the resident opened an account in Russian bank, he is obliged to keep records in accordance with Russian legislation.

As mentioned above, the Russian ruble is the only one monetary unit, wherein Russian organizations and businesses should keep accounting records. Consequently, the currency available on the accounts of the person concerned is subject to conversion into the national currency of the Russian Federation at the rate set by the Central Bank.

As a rule, the terms for revaluation of foreign exchange funds are as follows:

- transaction date;

- the last day of the month.

It is on these dates that the recalculation is carried out at the appropriate rate set by the Central Bank for this date.

The recalculation must be carried out in relation to both the currency received on the account and accounts receivable.

Fluctuations in the Russian national currency in relation to the exchange rate of foreign countries will inevitably entail the emergence of exchange rate differences, which will be revealed in the form of a specific amount based on the results of the revaluation of the currency.

The recalculation result can be:

- with a positive difference. In this case, the difference is included in other income;

- with a negative margin. In this case, the difference is charged to other costs.

When revaluing currency balances in accounting, the following entries are made:

- with a positive difference: Dt 57- Kt 91-1;

- with a negative difference: Dt 91-2 - Kt 57.

It is advisable to reflect the rules of the revaluation in question in accounting policies organizations.

Revaluation of currency balances in tax accounting

Currency conversion is also necessary for tax accounting purposes.

The timing of revaluation in tax accounting does not differ from accounting, the recalculation is carried out in the same way:

- or revaluation on the day of the operation;

- or currency revaluation at the end of the month.

As a result of the revaluation due to the volatility of the ruble exchange rate, there is:

- or a positive difference. In this case, the difference is accounted for in non-operating income. Emergence non-operating income entails an increase taxable base on income tax and tax in connection with the application of the "simplified tax";

- or a negative difference. In this case, the difference is included in non-operating costs when calculating income tax. In the calculation of the "simplified", the negative difference from the revaluation currency values not taken into account (Letter of the Ministry of Finance dated 25.07.2012).

Thus, we come to the conclusion that the revaluation of currency in accounting and tax accounting is of great importance, since entails fixing the occurrence on a certain date additional income or expenses (depending on the result with which the exchange rate difference is calculated).

The exchange rates against the ruble, established by the Central Bank on a specific date, are the basis for calculating the revaluation of foreign exchange funds both in tax and accounting.

Let's first turn to legislative framework RF. In it we will see that according to PBU 3/2006, if the value of assets and liabilities is expressed in foreign currency, then for reflection in accounting, this value is converted into rubles on the date of the transaction in foreign currency and on the reporting date, that is, the last day of the month.

How is currency accounting and currency revaluation implemented in 1C 8.3 Accounting 3.0?

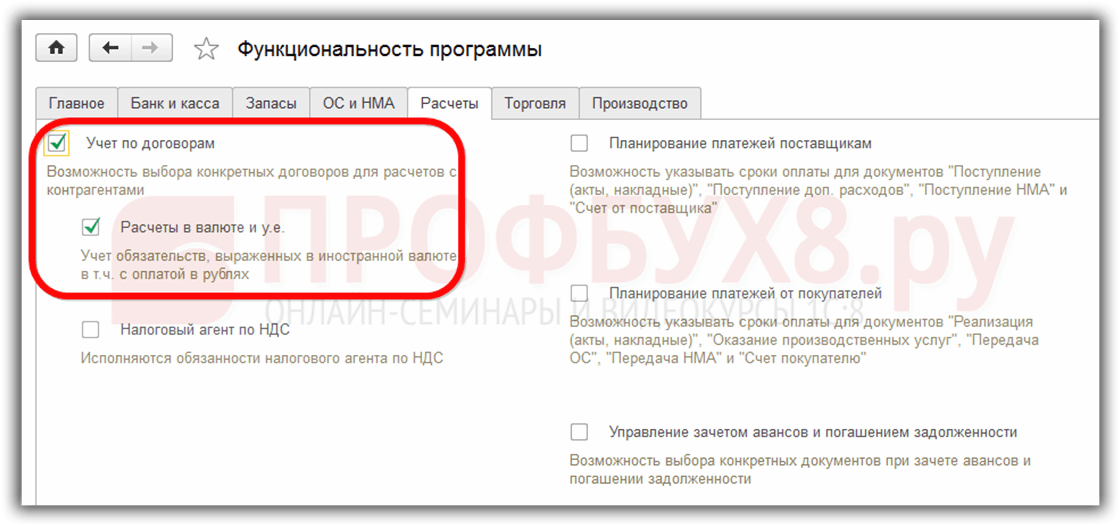

To be able to keep currency accounting in the 1C 8.3 program at the start of operation, you need to configure Functionality allowing. Menu Main - Settings - Functionality:

It is also necessary in the reference book Currencies:

add foreign currencies required for work in 1C 8.3:

and ensure that the values are updated on a regular basis in a timely manner. exchange rates in the eponymous information register:

Accounting for currency transactions in 1C 8.3

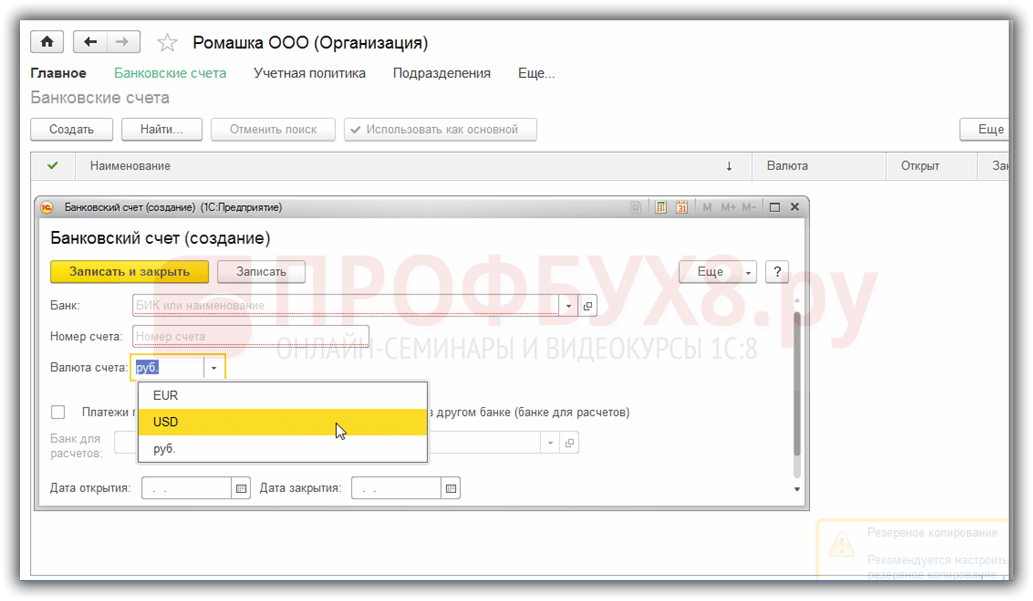

If the company has a foreign currency bank account, the data about it must be entered in Directory Bank accounts of the organization:

To conduct foreign exchange transactions in the program 1C 8.3 Enterprise Accounting 3.0 in the chart of accounts, there are special accounts that have the sign of foreign exchange accounting:

This feature allows in the standard reports of the 1C 8.3 program to see the balances on these accounts not only in the regulated currency - rubles, but also in the required foreign currency:

Revaluation of foreign exchange funds in 1C 8.3

Nothing stands still and exchange rates change. Accordingly, the amount of the ruble equivalent of balances on foreign currency accounts should be recalculated with the same amount of foreign currency balance. Depending on whether the rate rose or fell, the organization will incur other income or expenses when revaluing.

Where in 1C 8.3 currency revaluation

As soon as in the information base of the 1C 8.3 Accounting 3.0 program there are foreign currency accounts with balances of amounts on them, in processing Closing of the month a line will appear transactions Revaluation of foreign exchange funds... This operation is precisely designed to analyze the balances of the foreign currency accounts of the chart of accounts and to revalue the foreign currency amounts with the recognition of other income or other expenses, forming the corresponding postings in automatic mode.

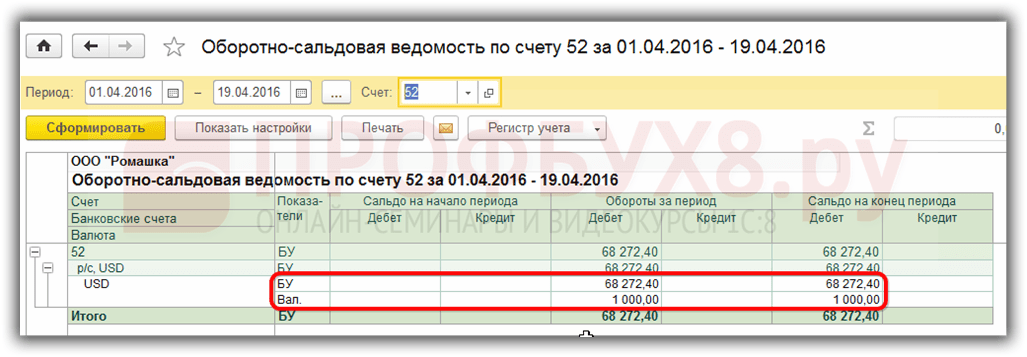

For example, in April, the Romashka LLC organization opened a foreign currency current account and a payment from a client in the amount of $ 1,000 was credited to it (rate 68.2724). Reflecting the receipt of currency in the 1C 8.3 program, in processing Closing of the month appeared transaction Currency revaluation:

although in March it was not:

So, now knowing all of the above, let's return to the 1C Accounting 3.0 program and use examples to figure out how currency revaluation occurs in automatic mode.

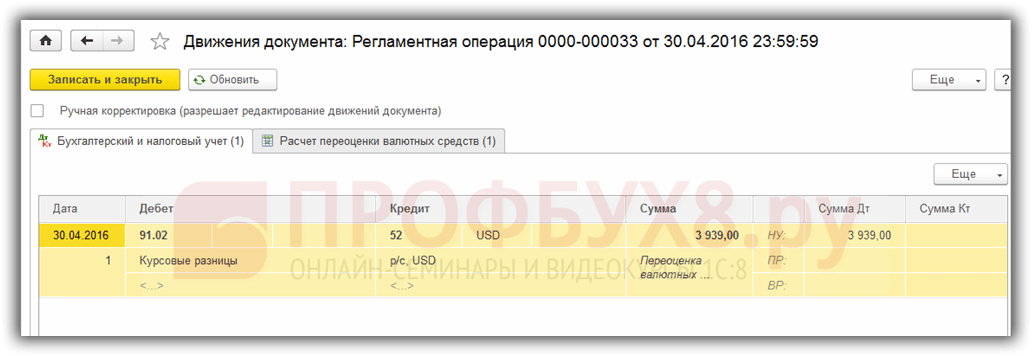

Example 1. If the rate has decreased

On 04/19/2016 the dollar exchange rate was 68.2724 rubles, as of the reporting date April 30, 2016. it dropped to 64.3334 rubles. In the currency amount, nothing has changed, but the ruble equivalent has decreased, and, accordingly, the enterprise incurred expenses, which is reflected transaction Currency revaluation at the end of the period in April:

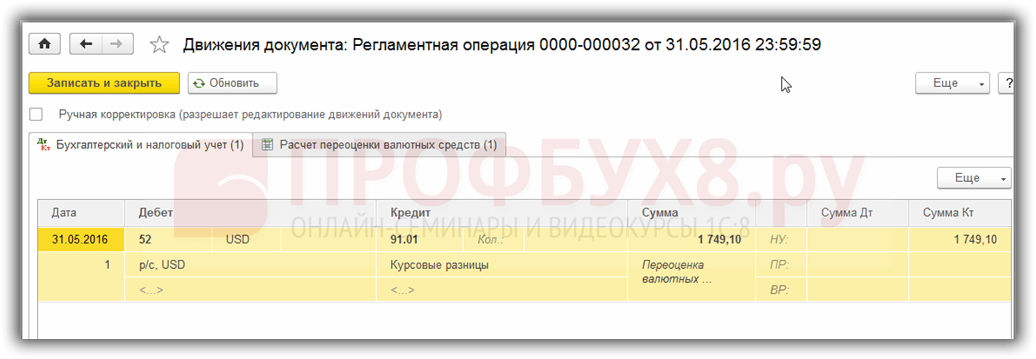

Example 2. If the rate has increased

During the month of May, no transactions were made on the account, respectively, as of the next reporting date, as of May 31, 2016, the need for revaluation arises again. The dollar exchange rate in comparison with the previous revaluation increased as of May 31, 2016. amounted to 66.0825 rubles. Thus, the organization has other income, which is reflected in Currency revaluation for May:

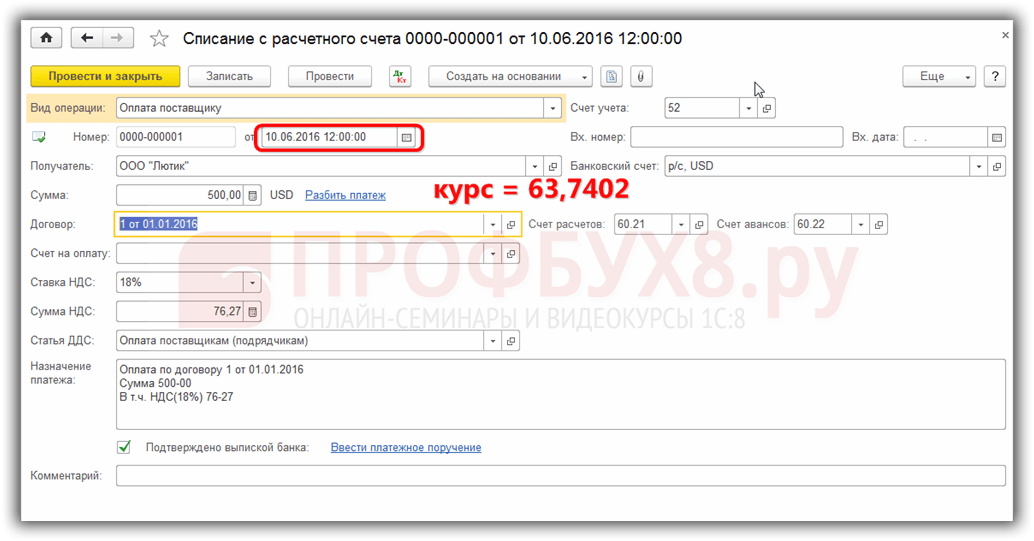

Example 3. Revaluation at the time of the transaction

As for the revaluation of currency in 1C 8.3 when performing an operation, the mechanism is similar to that discussed above, only the currency conversion rate is taken according to the day of the operation:

Relative to the previous revaluation date 05/31/2016. the rate fell on 06/10/2016. amounted to 63.7402 rubles. The organization must register the expense, which we see in the transactions:

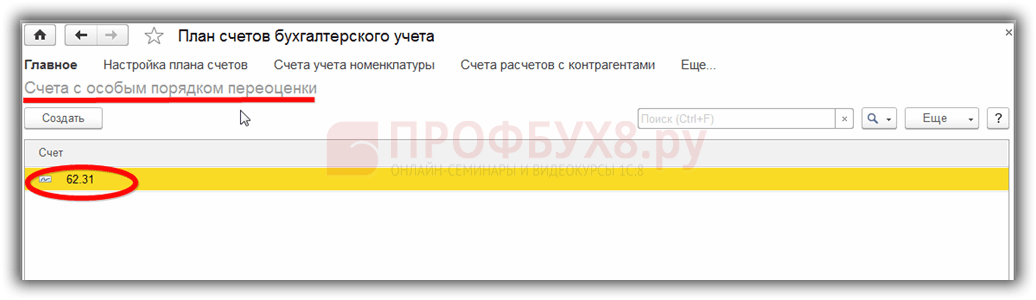

It is worth saying a few words about information register Accounts with a special revaluation procedure. You can get to this register through the menu Main - Chart of accounts - More - Accounts with a special revaluation order:

The accounts of the chart of accounts that require a different revaluation method than the one described above are entered here. If the account of the chart of accounts is included in this list, then automatically revaluation of balances when performing transactions on the reporting date routine operation will not happen. Revaluation must be done manually using Document Operations entered manually:

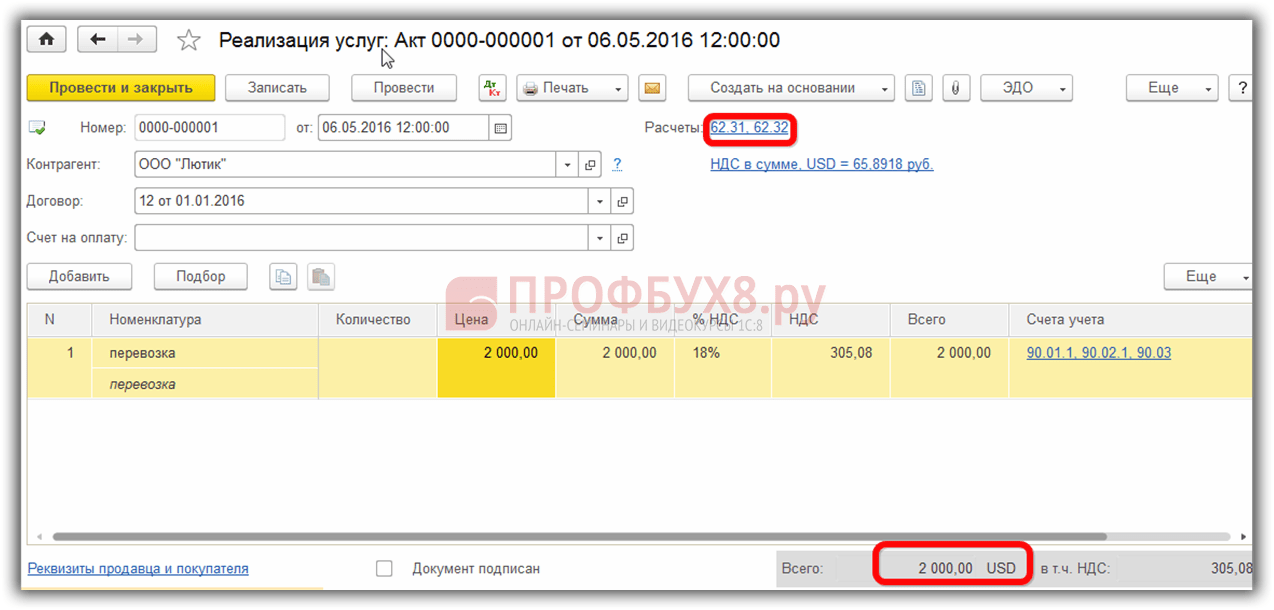

For example, 05/06/2016. the organization rendered a service in the amount of 2000 c.u.,

thus, the debt on account 62.31 was formed:

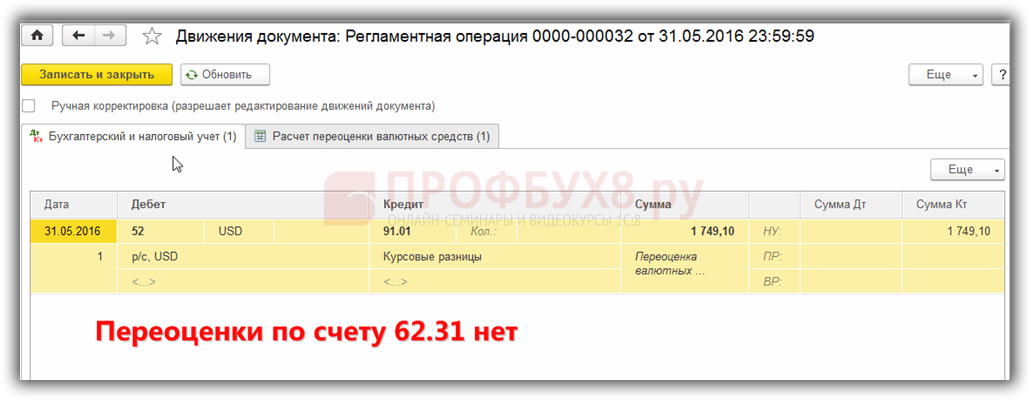

If information register Accounts with special revaluation procedure leave blank, then at the end of the period of May in transactions Currency revaluation there will be a revaluation of the balance on account 62.31:

If account 62.31 is added to this list:

then in Closing the month the balance on it will not be overestimated:

Thus, the family accounting program is able to help the user who is faced with the difficult issue of accounting and. The accountant just needs to set everything up correctly and control the generated transactions.

- How to get a Metro Cash & Carry card for an individual - getting a card and a list of documents Metro card registration

- An example of registration of an act of reconciliation of mutual settlements

- How to withdraw money from YouTube (YouTube) and Google Adsense (Google Adsense) to a Sberbank card: A Complete Guide

- Active income: types and creation of sources