Basic scenario for the development of the Russian economy. Development of scenarios for the development of the municipality

Every year it is more and more difficult for small St. Petersburg chains and individual grocery stores to compete with federal players. To survive, they are currently negotiating the creation of a single purchasing union, but large suppliers are hindering this in every possible way.

While there is no such center, large traders saw an opportunity to expand their sales markets in cooperation with local players. The wholesale departments of Lenta, Ryady Optical Club and METRO Cash and Carry are already supplying goods to stalls and small shops at a cheaper rate than wholesale companies or manufacturers do. Cash and Carry: In the fall of 2017, the company changed the signage at three of its six stores, and their revenues grew by 5-15%. The plans are to further develop under a foreign brand.

Found a sale

Fasol is a franchise project of the METRO Cash and Carry chain of stores for small and medium-sized businesses. The retailer helps grocery store owners to modernize their business, in return receiving a guaranteed distribution channel, since, by acquiring a franchise, a small business undertakes to purchase a certain amount of goods from METRO.

Currently, there are 220 stores under the Fasol brand in Russia, of which 24 are in St. Petersburg and the Leningrad Region. More than 10 stores will open soon.

The partnership between First Prize and METRO Cash and Carry is the first time in St. Petersburg when a whole chain of stores has changed a brand. Previously, only individual entrepreneurs and shops of the "Products 24 hours" format. As the commercial director of the First Prize Sergei Gorchinenko told DP, since September last year, the chain has converted three of the six stores into Fasol and is going to continue cooperation.

According to him, in the person of METRO Cash and Carry, "First Prize" received a major partner, a wide range of products and good prices.

From despair

Against the background of the rest Russian regions the project "Beans" in St. Petersburg did not develop very actively. Experts attribute this to high competition from federal networks. In St. Petersburg, more than 80% of retail turnover in the food segment is accounted for by chain retail, and it is formed by the top 10 retailers.

The number of small food retail facilities (non-stationary points or single stores retail space from 200 m2) is reduced. But the number of small specialized outlets selling baked goods, fruits, milk, etc. is growing, say InfoLine.

Several years ago, billionaires Dmitry Kostygin and August Meyer also relied on this audience, bringing to Russian market a new format for the country - the network of hypermarkets "Optical Club" Ryady ". Optical clubs are designed specifically for b2b-direction and cooperation with small and medium-sized businesses.

"It is obvious that for this category of buyers the offer in St. Petersburg is not developed. Now they come either to wholesale bases with the appropriate level of service and quality of goods, either to us, or to METRO," states the Ryady Optical Club. more than 1 thousand regular customers - legal entities.

Salvation in unification

Ivan Fedyakov believes that in the face of pressure from large chains, the only way for small grocery retailers to survive is to unite into purchasing alliances, following the example of retailers in the USA and Europe.

In Russia, attempts to create such associations have been made since 2001, but almost all of them have failed. A more or less active project in Russia is the Federal Purchasing Union (FZS), which unites 96 regional chains in Russia (more than 4.5 thousand stores), but from all over the North-West only the St. Petersburg "Smile of Rainbow" and the Novgorod network entered into it "Quarter".

"The union reduces the cost of purchases for its members through direct imports, the purchase of exchange commodities in large volumes and the development of its own brands. Now the union has six of them, and 20 more will appear by the end of the year," the FZS told DP.

The activities of Russian purchasing unions are stalled mainly for two reasons, Ivan Fedyakov is sure - this is the mistrust of entrepreneurs towards each other and the low discipline of entrepreneurs: the networks make purchases either through the union or on their own.

Alexander Myshinsky believes that the merger is really inevitable, otherwise the small chains will simply not be able to withstand the competition. "We are currently negotiating with our colleagues to create a purchasing alliance, but federal suppliers are doing everything possible to prevent this, for example, they threaten that they will not enter into direct contracts with the union or refuse to reduce prices," the retailer says.

In the summer, the chains experience a traditional decline in sales, many are trading in the red. According to Ivan Fedyakov, not all companies will be able to survive this summer season.

I do not see a massive transition of small grids in the near future to work with large grids. Projects "Fasol" and others are, in my opinion, an attempt to study the market of shops within walking distance of large chains. In fact, these are pocket nets, in which the matrix of products is formed, to put it mildly, unprofessionally. I would not argue that independent small retail is dying. See what happens to the bakery market, how bakeries are growing. "Products 24 hours" is generally a separate format that entrepreneurs from neighboring countries love, and they will certainly stick to the last.

The Bank of Russia, alarmed by external and internal factors of uncertainty, has drawn up several development scenarios Russian economy for the next three years: baseline, unfavorable and negative. Moreover, the baseline scenario does not take into account the introduction of a sales tax and long-term geopolitical tensions.

“Inflationary risks in Russia remain at an elevated level,” Central Bank Governor Elvira Nabiullina warned on Friday, September 12, during the presentation of the new “Guidelines for a single monetary policy for 2015-2017 ".

In the next three years, the conditions for the development of the Russian economy, according to the document, will be characterized by a high degree of uncertainty. The Central Bank fears that, on the one hand, inflation can be dispersed by external factors - geopolitical tensions, sanctions, oil price dynamics, on the other hand, by the government's tax and tariff policy and internal infrastructure and resource constraints, including those associated with unfavorable demographic trends.

To outline its policy in the implementation of certain risks, the Bank of Russia considered three scenarios for the development of the Russian economy. Under the baseline scenario, the introduction of special measures to support the financial sector will not be required; an increase in the volume of refinancing of the banking system will be sufficient. If less favorable scenarios are realized, the Central Bank will be ready to use additional tools corresponding to the scale of risks - from foreign exchange intervention to stabilize the situation in the domestic foreign exchange market before foreign exchange refinancing and unsecured loans.

Basic scenario

According to the published document, the Bank of Russia considers the most likely scenario, which is also the most favorable: geopolitical risks will decrease after the first half of 2015, oil prices will be relatively stable, and the government's tariff and tax policies will not create additional pressure on inflation. In general, the baseline scenario is close to the forecast of the Ministry of Economic Development for the same period.

It does not imply the introduction of new sanctions, although the old ones, including the deterioration of access to external financial markets will become a deterrent to economic growth in 2015. Domestic demand will be the main contributor to GDP growth, but it will also be limited by low growth rates wages and retail lending. Financing of infrastructure projects at the expense of the Fund national welfare, investment project to expand gas exports to China and the use of refinancing instruments by the Central Bank should help restore investment activity.

Even under the most optimistic scenario, the growth rate of demand for money and credit will be slightly lower than in previous years, and the money supply will be formed mainly due to refinancing operations of the Bank of Russia, which will lead to further growth debts of banks to the Central Bank. Earlier, the Central Bank noted that the total volume of refinancing by the end of 2014 will reach 7 trillion rubles, the maximum value since the 2008 crisis: today it exceeds 8% of all banks' liabilities, three years ago it was at the level of 1.7%.

However, under the baseline scenario, this will be practically the only challenge for the Central Bank, "risks to financial stability will be moderate and the introduction of special measures to support the financial sector will not be required."

Unfavorable scenario

The Central Bank believes that the prerequisites for the implementation of a less optimistic scenario are the persistence of foreign policy tension throughout all three years, the longer duration of mutual sanctions and an increase in the tax burden on the economy. Only the introduction of a sales tax can lead to a one-time significant acceleration of inflation by 1-1.5%, Nabiullina noted. If this scenario is implemented, a larger capital outflow is also expected, which will cause the ruble to weaken. The change in the exchange rate, on the one hand, partially compensates for the negative impact of external conditions, supporting economic activity through an increase in exports, on the other hand, it will lead to an increase in inflationary pressure. Under these conditions, in 2015–2016 inflation will be above the target values - at the level of 6–6.5 and 4.5–5%, respectively.

In this case, the Bank of Russia will strive to reduce inflation "gradually, without creating a threat of an excessive slowdown in economic activity." And in case of signs of destabilization of the situation in the financial sector, the regulator is ready to use additional instruments corresponding to the scale of risks - from foreign exchange interventions to foreign exchange refinancing, unsecured loans.

Negative scenario

The third scenario assumes the most negative external and internal conditions for the development of the Russian economy. It is based on assumptions similar to the previous scenario in terms of prolonged sanctions and parameters tax policy, but also assumes a decrease in oil prices by $ 20 per barrel by 2017.

According to RBC daily, the first two scenarios proceeded from the forecast for the preservation of a moderate downward trend in oil prices - from $ 106.5 per barrel on average since the beginning of 2014 to $ 102.5 in 2017 - due to a faster expansion of world supply compared to world demand with sufficient profitability of oil production from unconventional sources. In a negative scenario, weaker growth rates of the world economy, primarily China, and a dynamic increase in oil exports from the United States and the Middle East lead to a sharp decline in oil prices to $ 86.5 per barrel. Moreover, as noted by Nabiullina, "this is not a stressful scenario, it is also quite realistic." If this scenario is realized, the resources of the Reserve Fund can be used to stabilize the situation. This will increase domestic demand, but will not be able to completely replace external demand. The weakening of the ruble, which will lead to a drop in oil prices, will create conditions for an increase in exports and will intensify import substitution, but will accelerate inflation.

The Central Bank in such conditions will have to maintain confidence in national currency and to prevent the outflow of funds from ruble deposits and the growth of inflationary expectations. “We can say that now the implementation of the first and second scenarios is most likely. There is quite a lot of uncertainty about everything related to the government's budgetary policy and the realization of the risks associated with the prolonged effect of the sanctions, and it is difficult to predict what exactly will happen, ”explains Natalya Orlova, chief economist at Alfa-Bank. “In any case, there is a very high probability that the Central Bank will have to reintroduce non-standard instruments like unsecured loans. In the coming years, the regulator will need to replace funds that will not be available from external debt markets, and in banking system there is no longer enough free pledges. Foreign exchange refinancing appears to be less likely as it will lead to forecasting problems gold and foreign exchange reserves and destabilizes sentiment in the foreign exchange market. If someone needs currency, he can get it on the foreign exchange market, ”adds Orlova.

Larin S.N., Sokolov N.A.

1. Candidate of Technical Sciences, Leading Researcher

2. Candidate of Physical and Mathematical Sciences, Leading Researcher

FGBUN Central Economics and Mathematics Institute RAS, Moscow

Larin Sergey Nikolaevich, Sokolov Nikolay Aleksandrovich

1. Candidate of Technical Sciences, Leading Researcher

2. Candidate of Physical and Mathematical Sciences, Leading Researcher

FGBUS Central Economical and Mathematical Institute RAS, Moskow

Annotation: The article examines some of the forecast scenarios for the development of the Russian economy in 2017-2020, taking into account the negative impact of the sanctions restrictions. They were developed by specialists from leading foreign and domestic organizations, the main profile of which is associated with forecasting the development of the economy of individual countries or a specific country and assessing its dynamics. In this regard, the object of research in this article was the Russian economy, and the subject of the study was the forecast scenarios of its development for the next three years. The main objective of the study was to identify the presence of the influence of key factors and the prospects for the implementation of new opportunities for recovery and transition to sustainable growth of the Russian economy. To solve it, we considered a number of forecast scenarios for the development of the Russian economy and identified the key factors contributing to their implementation. In addition, a comparative analysis of forecast scenarios developed by specialists from leading foreign and domestic organizations was carried out. Its results, as well as statistical assessments of the current state, made it possible to formulate the conclusion that, despite the negative impact of the complex of sanctions restrictions, the Russian economy during 2017 demonstrated higher rates of recovery growth and outrunning development in a number of leading industries. This fact serves as convincing evidence that the Russian economy has significant potential for recovery and transition to sustainable growth, as well as opportunities to minimize the negative impact of sanctions restrictions in the near future.

Abstract: In the article some of the forecast scenarios of the development of the Russian economy in 2017-2020 are considered taking into account the negative influence of sanctions restrictions. They are developed by specialists of leading foreign and domestic organizations whose main activity profile is related to forecasting the development of the economy of individual countries or a particular country and assessing its dynamics. In this regard, the object of the study in this article was chosen by the Russian economy, and the subject of the study were the forecast scenarios of its development for the next three years. The main objective of the study was to identify the presence of the influence of key factors and the prospects for realizing new opportunities for recovery and transition to a sustainable growth of the Russian economy. To solve it, we considered a number of forecast scenarios for the development of the Russian economy and identified key factors that facilitate their implementation. In addition, a comparative analysis of forecast scenarios developed by specialists from leading foreign and domestic organizations was carried out. Its results, as well as statistical assessments of the current state, made it possible to formulate the conclusion that, despite the negative impact of the sanctions package, the Russian economy in 2017 demonstrated higher rates of recovery growth and outstripping development in a number of leading industries. This fact is a convincing confirmation of the Russian economy "s significant potential for recovery and transition to sustainable growth, as well as opportunities to minimize the negative impact of sanctions restrictions in the short term.

Keywords: Russian economy, sanctions restrictions, impact assessment, development scenarios.

Keywords: Russian economy, sanctions restrictions, impact assessment, development scenarios.

Introduction

Four years have passed since the introduction of the United States, most of the EU member states and a number of other economically developed countries(Australia, Canada, Japan, etc.) a set of sanctions restrictions aimed at stifling the development of the Russian economy. During this time, quite significant damage from these restrictions became obvious, which was experienced by both the Russian economy as a whole, and its individual industries and sectors, as well as households. First of all, it was felt by the key sectors of the Russian economy - the oil and gas and military-industrial complexes, practically the entire sphere of space activity and many branches of heavy industry (machine-building and machine-tool complex, transport and shipbuilding complexes, automobile and aviation industry, industry building materials and others), a number of specific enterprises and corporations, as well as individual individuals, the lists of which are updated and expanded at regular intervals. The steps and measures taken by the countries that initiated the introduction of sanctions restrictions in international politics with great confidence make it possible to assert that their mitigation or lifting is not foreseen even in the distant future.

Objects and research methods

The situation in the international arena is more and more definitely taking the direction of a rather long period of the sanctions restrictions against the Russian economy. But this does not mean at all that Russia will meekly accept this situation. Rather, one should expect a response and the adoption of a set of asymmetric measures to counter the sanctions restrictions and reduce their negative impact on the development of the Russian economy. In this regard, it seems appropriate to explore the possibilities and analyze various scenarios for the development of the Russian economy, made by both foreign and domestic specialists, experts and analysts. This article will present such forecast estimates, as well as briefly analyze the conditions that determine them.

experimental part

- Assessment of the prospects for the development of the Russian economy by foreign analysts

As a rule, foreign analysts give less optimistic assessments of the current state and forecasts of the expected prospects for the development of the Russian economy in comparison with domestic specialists from the Government of the Russian Federation, the Central Bank of the Russian Federation, relevant ministries and departments. This is mainly due to the fact that they are forced to operate with limited volumes of economic information and cannot see the general picture of the changes taking place in the Russian economy from the inside. Therefore, foreign analysts and specialized agencies are cautious in their assessments. Taking into account the high instability of external markets, the presence of internal inflation and the incompleteness of the processes of structural adjustment, in their forecasts they assume a rather long period of development of the Russian economy with insignificant growth rates.

1.1 Forecast scenarios of the World Bank analysts

Analysts of the World Bank (WB) considered justified the adoption by the Government of the Russian Federation of a special anti-crisis plan, as well as the efforts of the state to attract funds from reserve fund to finance a fairly significant (up to 2.4% of GDP) budget deficit in 2015. In their opinion, the household economy suffered the greatest damage from the sanctions restrictions. They resulted in a sharp devaluation of the ruble, currency depreciation up to 12% and inflation growth of more than 9%. As a result, the real level of wages, pensions and other social benefits decreased, which led to a decrease in consumption of the population in 2015 by 9.6%. Against this background, the Central Bank of Russia managed to develop and implement in practice a well-grounded monetary policy, the main goal of which was to gradually reduce the inflation rate in the country. This policy led to the fact that already at the end of 2017 the real inflation rate was 2.4%, while its planned value was 4%.

The World Bank report notes that changes in the global market environment have led to the realization of the need for an accelerated transition of Russia's economic policy from the dominance of the export of raw materials to the innovative development of non-traditional sectors of its economy. Practice has shown that the raw materials orientation of the development of the Russian economy made it dependent on a decrease in market prices for energy resources and the introduction of sanctions restrictions on the purchase of high-tech equipment and components of foreign production. This circumstance has become a confirmation of the need for structural reforms in the country's economy, including reforming the regulatory and legal legislative framework, increasing the transparency of doing business and increasing the validity of the economic policy pursued in general. It is today that external circumstances are forcing the country's leadership to begin the real implementation of structural transformations.

The forecast scenarios of the WB specialists on the further development of the Russian economy differ from each other in terms of the dynamics of its recovery, as well as in taking into account the degree of influence of external factors on the growth of the population's well-being. Thus, the baseline scenario assumes an average oil price in 2016 within the range of USD 37-40 per barrel, followed by an increase in its price quotations during 2017 to USD 50 per barrel (Figure 1). At the same time, under the conditions of the baseline scenario, it is assumed that the entire range of sanctions restrictions will remain in effect until 2018-2020. If the baseline scenario is implemented, the GDP of the Russian economy will decrease by another 1.9% by the end of 2016, and a slight increase in this indicator is expected not earlier than 2017 by about 1.1%. And only in 2018 the Russian economy will grow at a higher rate - up to 1.8% of GDP.

Figure 1. Dependence of GDP growth in the Russian economy on the dynamics of market price quotations for oil.

Sources: Compiled from Rosstat and World Bank data.

Positive and negative scenarios for the development of the Russian economy are based on deviations in the dynamics of market price quotations for oil in the direction of their growth or decline, respectively. The positive scenario assumes positive dynamics of market price quotations for oil. However, even with such a development of events, there are not sufficient grounds for predicting a sharp growth of the Russian economy, since the high volatility of price quotations in the hydrocarbon markets will contribute to an increase in external risks. Only a real restructuring of the Russian economy will make it possible to hope for an improvement in the main macroeconomic indicators. The consequences of the shocks of 2014 and 2015 will be expressed in a further decrease in GDP by 0.7% in 2016, and only then is this indicator expected to increase slightly compared to the baseline scenario in 2017 to 1.7%, with its subsequent increase in 2018 to 2 %.

The negative scenario provides for a downward deviation of the dynamics of market price quotations for oil compared to the baseline scenario. In this case, the negative impact of external risks on the Russian economy will continue, which will lead to a loss of up to 2.5% of GDP in 2016. A recovery in the development of the Russian economy should be expected no earlier than 2017 - first by 0.3¸0.5% of GDP, and by the end of 2018 this indicator may grow to 1.6¸1.8%.

The above forecast scenarios for GDP growth in 2017-2019 are shown in Figure 2.

Figure 2. Forecast scenarios of GDP growth in the Russian economy in 2017-2019.

Source: compiled from the official website of the World Bank.

According to the WB forecasts, it can be concluded that the Russian economy has emerged from the recession and returned to moderate growth rates in 2017.

1.2 Forecasts of experts from the European Commission

The European Commission specialists slightly raised their previous forecasts regarding the development of the Russian economy for the period 2017-2019. Thus, they associate the improvement in the forecast for GDP growth with some stabilization of the ruble exchange rate and the dynamics of market price quotations in the hydrocarbon markets. Based on the action of these factors, they believe that the GDP growth of the Russian economy at the end of 2017 will be 1.7%, but then this forecast is dominated by pessimistic estimates, according to which the expected GDP growth of the Russian economy will slow down to 1.6% at the end of 2018. with its subsequent decline to 1.5% at the end of 2019.

These forecasts were made on the basis of adjustments to the GDP growth of the Russian economy made in the first ten days of November 2017 by the largest Swiss bank UBS and the European Bank for Reconstruction and Development (EBRD), which revised their estimates for the growth rate of this indicator in 2017, respectively, from 1.6 % to 1.9% and from 1.2% to 1.8%. In addition, the EBRD revised its GDP growth forecasts for the Russian economy for 2018 from 1.4% to 1.7%. At the same time, in the opinion of the EC experts, insufficient financial consolidation of assets of the banking and real sectors, prolongation of the sanctions restrictions, as well as its insufficiently rapid structural restructuring will have a negative impact on the growth rate of the Russian economy. It is expected that the next extension of the sanctions restrictions will have a negative impact on the growth of the Russian economy in the medium and long term, since it will continue to restrain the access of Russian banks and real sector enterprises to external sources of financing.

The EC notes that the growth prospects of the Russian economy are still strongly dependent on the growth prospects of the raw materials extractive industries, both in terms of the value of the value added indicator and the generation of tax revenues. According to forecast estimates, significant shifts in this direction are not expected in 2017-2019. Internal factors hindering the growth of the Russian economy will also retain their influence, such as: an unfavorable environment for doing business, insufficient inflow real investment, slow transformations in the labor market, etc. Given the continued weak dynamics of reforms, it is safe to say that these shortcomings will further exacerbate risks in the financial sector, and financial constraints are likely to have a negative impact on the growth of the Russian economy in the near future ...

At the same time, by the end of 2018, EC experts predict a decrease in unemployment in Russia to 5.6% and inflation rates to 4.7%.

The main indicators of the development of the Russian economy and their forecast estimates made by the experts of the European Commission are shown in Table 1.

1.3 Forecast estimates of the prospects for the development of the Russian economy by the IMF

The forecasts of the prospects for the development of the Russian economy, formed by the International Monetary Fund (IMF), are based on taking into account the cumulative influence of two fundamental factors, namely: the growth trend of long-term risks with a relative stabilization of the ruble and a slight increase in oil price quotations on world markets, as well as further The Central Bank Russia's tight monetary policy. The baseline scenario of the IMF for 2017 was formed based on the level of oil price quotations of USD 50.6 per barrel (for Brent).

Table 1

Main indicators of the development of the Russian economy and their forecast estimates

| The main indicators | RUB bln | % | Annual percentage change | |||||

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |||

| Gdp | 86043,6 | 100 | 0,7 | -2,8 | -0,2 | 1,7 | 1,6 | 1,5 |

| Private consumption | 44273,3 | 51,5 | 2,0 | -9,7 | -4,5 | 2,4 | 2,6 | 2,5 |

| Public consumption | 15549,4 | 18,1 | -2,1 | -3,1 | -0,5 | 0,2 | -0,4 | -0,2 |

| Gross fixed capital formation | 17169,5 | 20,0 | -1,3 | -10,4 | -1,4 | 3,5 | 2,3 | 2,0 |

| Export (goods and services) | 22124,4 | 25,7 | 0,5 | 3,7 | 3,1 | 5,1 | 4,3 | 4,2 |

| Import (goods and services) | 17685,8 | 20,6 | -7,3 | -25,8 | -3,8 | 9,7 | 6,2 | 5,9 |

| GNI (GDP deflator) | 83970,0 | 97,5 | 1,1 | -2,2 | -0,2 | 1,8 | 1,6 | 1,6 |

| Employment | 0,2 | 1,1 | -2,1 | 0,1 | 0,1 | 0,1 | ||

| Unemployment rate | 5,2 | 3,9 | 5,7 | 5,4 | 5,2 | 4,9 | ||

| Consumer price index | 7,8 | 15,5 | 7,1 | 3,9 | 3,7 | 3,5 | ||

| Trade balance (goods) | 9,0 | 10,7 | 7,0 | 7,5 | 7,4 | 7,2 | ||

| Current account balance | 2,6 | 4,8 | 1,8 | 2,0 | 1,8 | 1,5 | ||

| Overall balance | -1,0 | -3,4 | -3,7 | -2,5 | -1,7 | -1,1 | ||

| Total gross debt | 16,1 | 15,9 | 16,3 | 15,6 | 15,3 | 14,4 | ||

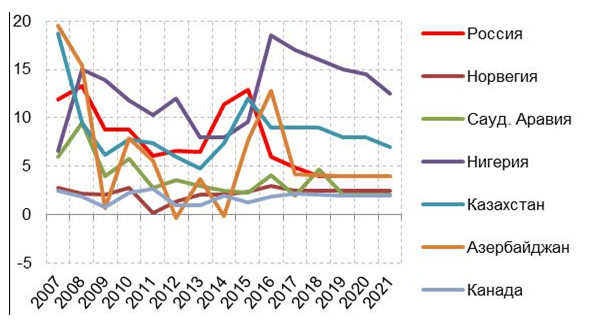

According to the IMF report on the development of the world economy, the projected GDP growth rates of the Russian economy will have a slight positive trend of up to 1.5% annually, starting in 2018. At the same time, the IMF proceeds from a further reduction in inflation estimates in Russia, which in 2018 should be lower to 4% and approach the average level for large "oil" economies, such as Kazakhstan, Azerbaijan and Nigeria (Figure 3).

IMF experts believe that taking into account the forcedly pursued tight monetary policy and all-round savings of budgetary funds, the Government of the Russian Federation will not be able to quickly use to accelerate economic growth institutional factors. Although certain prerequisites for this will be created in 2017-2021, namely: it is expected that household savings will exceed gross fixed capital formation by 3.5-4.0% of GDP, and their share in GDP will increase from 22.4% to 2018 to 24% in 2021. But at the same time, low investment activity will not allow for the progressive growth of net exports, which in the context of the devaluation of the ruble could lead to an increase in the GDP of the Russian economy in the analyzed period. In addition, the physical volumes of imports in value terms in this period may exceed the growth rates of exports, the value of which is projected at the level of 1-3% per year. They are in line with the averages for oil-dependent economies, but these projections are clearly lower compared to countries such as Kazakhstan or Nigeria. However, even with insignificant dynamics of growth in export volumes, the balance of the account current operations v the Russian budget will remain at the level of 3.9% of GDP in 2018 to 4.4% of GDP in 2021. This gives every reason to predict the stability of the development of the Russian economy and sustainability exchange rate ruble.

Figure 3. Actual rates and forecast of inflation dynamics, in%.

Source: compiled from the official website of the IMF.

1.4 Expert forecast analytical agency Standart & Poor's

Experts of the analytical agency Standart & Poor's (S&P) predict a transition to the development of the Russian economy during 2017, which, according to their calculations, will lead to a GDP growth of 1.4%. However, this value cannot be recognized as optimal, since the real development of the Russian economy, the agency's experts associate only with its restructuring. Until the structural reforms are carried out, the Russian economy, in their opinion, will remain influenced by the dynamics of market price quotations in the hydrocarbon markets. With stable price quotations or their insignificant growth, the value of the GDP indicator of the Russian economy in 2018-2020 may increase to 1.7% compared to 2017. In the event of a decrease in price quotations, the growth of the GDP indicator of the Russian economy will be characterized by lower values. Agency experts predict market price quotations for oil in 2017 at $ 52.4 per barrel. The specialists of the International Monetary Fund expect that the values of market price quotations for oil in 2017 will stabilize at about USD 50.6 per barrel in 2017, with a possible increase to USD 53.1 per barrel in 2018.

S&P experts believe that with a slight increase in macroeconomic indicators, the Russian economy will be able to ensure the normal functioning of its banking sector. It is still too early to count on the growth of consumption on the part of the population, since the drop in its real incomes has had a significant effect. To restore the consumption of the population at the level of 2014, according to the experts of the agency, it is necessary to ensure the annual growth, primarily of wages, in the range from 10% to 12%.

Based on the forecasts above, the International Analytical Agency (S&P) on March 17, 2017 also raised the outlook on Russia's sovereign rating from “stable” to “positive”.

1.5 Fitch Agency's Forecast Estimates of the Development Prospects of the Russian Economy

Many rating agencies have assigned the “Negative” level to the Russian economy for quite a long time. Against this background, a positive exception was the forecast quotes of the rating agency Fitch, which a year ago (in October 2016) assigned the level “Stable” according to the long-term issuer default rating (IDR) for a number of Russian banks and for the Russian economy as a whole (IDRs). The experts of the Fitch agency also noted that, in comparison with other oil exporting countries, the Government and the Central Bank of the Russian Federation conduct a more adequate macroeconomic policy, which takes into account the dynamics of changes in prices for oil and other natural resources.

International rating agency In the first ten days of November 2017, Fitch announced an increase in the forecast for Russia's GDP growth from 1.6% to 2%, and in 2018-2019 the growth of the Russian economy will average 2.1%. The reason for this was the implementation of a medium-term tax strategy in Russia, according to which it is planned to freeze or reduce budget expenditures on some items with a simultaneous increase in excise taxes and a number of other tax collections. Thus, the agency acknowledged the presence of a recovery trend in the development of the Russian economy when reaching a record low level inflation and stability financial system... As a result, the agency made a decision to change Russia's rating from “Stable” to “Positive”.

- Assessment of the prospects for the development of the Russian economy by specialists of domestic organizations

Of course, it makes no sense to say that specialists from domestic organizations have a common point of view regarding the prospects for the development of the Russian economy, since all specialists approach the solution of the problem under study taking into account different initial data, which, in fact, makes their assessments different. As a rule, the forecasts of government organizations are more optimistic than the estimates of independent specialized institutions and agencies. All of them recognize that, unlike other resource-based economies, the Russian economy really has, in fact, unlimited opportunities for quick adaptation to changes in market conditions. Many are in favor of the fact that the stable development of the Russian economy will begin as early as 2018. At the same time, practically none of the domestic specialists dares to predict the high dynamics and sustainability of economic growth. Most experts agree that the Russian economy has managed to get out of the recession from the second half of 2017 and begin the transition to gradual economic growth, albeit with insignificant, but still positive dynamics.

2.1 Forecasts of specialists of the Ministry of Economic Development of Russia

The main parameters of the Forecast of the Ministry of Economic Development of Russia for 2018 and for the planning period of 2019 and 2020 are determined taking into account the trends in the development of the world economy, the dynamics of the conjuncture of supply and demand in foreign markets, as well as the level of influence of the degree of changes in internal conditions and the current results of the development of the Russian economy in the first half of the year 2017 year ... It is based on a scenario approach, and the document itself presents three expected scenarios for the development of the Russian economy - basic, conservative and target. At the same time, all forecast scenarios assume the further implementation by the Central Bank of Russia of monetary policy aimed at targeting inflation and ensuring the value of the inflation target within 4% during the entire forecasting period. In addition, all forecast scenarios are based on a fixed base price Urals crude oil in the amount of USD 40 per barrel in real terms (in 2017 prices). This approach assumes the mutual linking of costs federal budget with oil and gas revenues calculated at the base oil price.

The baseline scenario assumes the preservation of a set of existing sanctions restrictions on the Russian economy throughout its entire length, as well as retaliatory measures taken by Russia to minimize their negative impact. This scenario predicts a gradual increase in the growth rate of the Russian economy from 2.1% in 2017 to 2.3% by 2020.

The target scenario is based on foreign economic prerequisites similar to the baseline scenario. Its difference lies in the higher demographic forecast of Rosstat, which suggests higher fertility rates and higher migration gain... With the implementation of the target scenario, an accelerated restructuring of the Russian economy is expected, which will allow it to reach an indicator of its growth of 3.1% of GDP by 2020.

The conservative forecast scenario provides for a more significant reduction in global economic growth, further weakening of the ruble due to deterioration in the terms of trade and increased capital outflow from the country. In these conditions, according to experts, the GDP growth rate will decline in 2018 to 0.8%, followed by their recovery by 2020 to 1.5%.

The expected dynamics of changes in the GDP indicator for the three main scenarios of the forecast for the development of the Russian economy for 2018-2020, made by the specialists of the Ministry of Economic Development, are shown in Table 2.

table 2

Expected dynamics of changes in the GDP indicator according to the scenarios of the Ministry of Economic Development

If signs of stabilization of the Russian economy were noted in some of its sectors back in the second half of 2016, then in 2017 the recovery of economic growth was observed in almost all sectors. At the same time, the main factors that ensured positive GDP growth were the recovery of inventories (0.7%), growth in investment in fixed assets (0.9%) and the recovery of consumer demand (1.2%). The main factor in the development of the Russian economy in 2018-2020 will be the growth of investment activity, mainly due to an increase in the share of private capital. The growth in investment in fixed assets is expected to lead to a gradual increase in GDP from 1.0% in 2018 to 1.3% in 2020.

Compared to the previous forecasts of the analysts of the Ministry of Economic Development, only the conservative scenario is focused on a decrease in the GDP growth rate, while the baseline and especially the target scenarios assume rather optimistic dynamics of changes in this indicator. Obviously, one of the determining factors for such forecasts was the decrease in inflation rates to 2.4% by November 2017. Another determining factor was the dynamics of growth in oil prices. If at the beginning of 2017, experts expected price fluctuations in the range of $ 40-50 per barrel, then again in November 2017, oil prices exceeded $ 60 per barrel. Naturally, this could not but affect the forecast scenarios for the development of the Russian economy, made by analysts of the Ministry of Economic Development.

2.2 Forecasts of specialists of the Central Bank of Russia

The main options for forecast scenarios for the development of the Russian economy are presented by specialists of the Central Bank of the Russian Federation in the "Main directions of the unified state monetary policy for 2018 and the period of 2019 and 2020", which were approved by the Board of Directors on November 10, 2017. When formulating forecast scenarios for the development of the Russian economy, the Bank of Russia specialists based on conservative estimates of inflation risks, as well as opportunities for economic growth under the influence of internal factors. This approach led to a steady trend of strengthening the ruble exchange rate during 2017 and, thus, made a significant contribution to the decline in inflation to 2.7% at the end of October this year.

The Bank of Russia managed to purposefully combine measures public policy(application of refinancing instruments) and efforts of the private sector to reduce costs, strengthen financial situation and the use of new opportunities for recovery and expansion of production in the real sector of the economy. The complex of these measures contributed to the change in the driver of industrial production growth in 2017. So, back in the second half of 2016, an increase in industrial output was ensured by an increase in production in the raw materials sectors, but since the beginning of 2017, the main contribution to the increase in this indicator has already accounted for manufacturing. At the same time, positive changes in the economy have not yet acquired a systemic character in the leading industries and regions of the country. Therefore, based on the results of 2017, the Bank of Russia specialists forecast GDP growth in the range of 1.7-2.2%.

Forecasting scenarios for the development of the nearest Russian economy, the Bank of Russia experts assume that the nature of the action of fundamental factors will not undergo significant changes. So, on the one hand, the lack of opportunities to increase the extraction of raw materials and increase the volume of their supply to international market, will significantly limit the growth potential of the Russian economy. On the other hand, a number of internal factors will act as a constraint on economic growth and modernization. Among them - the low quality of management at all levels, poor development of transport and logistics infrastructure, high monopolization, insufficient investment in the development of innovative technologies, a high degree of wear and tear of fixed assets. Under these conditions, the growth rates of the Russian economy in 2018-2020, according to the estimates of the Bank of Russia specialists, will not exceed 1.0-1.5% under the baseline scenario of forecasting its development and 1.5-2% under the alternative scenario.

At the same time, in the baseline scenario, the slowdown in the GDP growth rate of the Russian economy in 2018 to 1.0¸1.5% compared to 1.7¸2.2% according to estimates for 2017 will be associated with the expected decline in oil prices and a decrease in income from export. During 2019-2020, a gradual recovery of GDP growth rates is expected to 1.5-2%. There is no reason to expect higher GDP growth rates in this period, since the growth potential of the Russian economy is still significantly limited by the influence of structural factors.

An alternative scenario assumes higher rates of growth in wages, investments and consumption compared to the baseline, primarily due to an increase in average annual oil prices to $ 60 per barrel in 2018-2020. This will slightly increase the expected revenues from the export of raw materials. However, if the structural imbalances in the economy persist, sufficient large-scale import purchases will be required to meet part of the domestic demand. Therefore, the annual growth of the GDP indicator will remain at the level of the baseline scenario and will not exceed 1.5¸2%.

2.3 Expert forecasts non-governmental Russian organizations

By teams of specialists from non-governmental Russian economic organizations — Russian Academy national economy and public service under the President of the Russian Federation (RANEPA), the E.T. Gaidar (IEP) and All-Russian Academy foreign trade (RFTA) - about prepared their own scenarios for the development of the Russian economy in 2017-2018. When developing them, they proceeded from the fact that, starting from the second half of 2016, the Russian economy has been on the rise, which will continue throughout 2017-2018. At the same time, the growth rates of the Russian economy will be positive, but not high, and the main influence on its development will continue to be provided by oil prices. Taking into account the expected dynamics of oil prices, the specialists of the above organizations have developed forecast scenarios for the possible development of the Russian economy in 2017-2018 - basic and conservative.

The baseline scenario takes into account a positive trend in oil prices in the range of USD 50-60 per barrel. It seems most likely that it will be preserved over the next two years. The conservative scenario is based on oil prices up to $ 40 / bbl. In any scenario, the team of specialists of these organizations predicts the growth of the GDP indicator of the Russian economy. In the conservative scenario, it will amount to 0.6% in 2017 and 1.7% in 2018, while in the baseline scenario these indicators will increase to 1.4% and 2.2%, respectively. Higher GDP growth rates in the context of slow structural transformations can only be achieved with a sharp increase in oil prices to $ 100 per barrel, but this option is modern conditions seems unlikely.

It is easy to see that both of the scenarios under consideration assume that the instability of the Russian economy remains unstable for the period 2017-2018, and its stabilization and the prospects for strong growth are expected no earlier than 2019. At the same time, experts believe that the growth rate of the Russian economy in any of the scenarios considered will not reach the growth rate of countries belonging to the leaders of the world economy. At the same time, if oil prices stabilize or rise with a simultaneous slowdown in inflationary processes in the Russian economy, income growth of the country's population may resume. However, a significant increase in consumer demand will not happen, since the population will prefer not to spend money, but to accumulate it in the absence of stability. In addition, the slowdown in inflation, according to the specialists of these organizations, is of a temporary nature. As a result, they predict the inflation rate at the end of 2018 within 6%. As you can see, the position of experts from nongovernmental Russian economic organizations partly contradicts the statements of the President and the Government of the country, which asserted that Russia overcame the crisis back in 2015, and today its economy is showing steady growth.

Comparison of forecasts of foreign and Russian analysts

Analyzing the forecasts for the development of the Russian economy given above, we can conclude that practically all organizations form them on the basis of assessments of the dynamics of mainly external or internal factors. However, over time, most of these forecasts quickly change significantly. So, if in the first half of 2017, most foreign analysts predicted a further slowdown of the recession in Russia, then in most of the baseline scenarios of the middle of the year, their forecasts appear assertions about the possibility of the transition of the Russian economy to growth by the end of this year. At the same time, the forecast estimates of different organizations differ from each other in the range from 0.5% to 1.2% (see Table 3).

Table 3

Forecasts of GDP growth in the Russian economy, in%

| 2016 year | 2017 year | 2018 year | |

| Ministry of Economic Development of Russia (10.2017) | — 0,2 | 2,1 | 2,1 |

| Central Bank of Russia (11.2017) | — 0,2 | 1.7¸2.2 | 1.0¸1.5 (basic) 1.5¸2.0 (alternative) |

| RANEPA, IEP and VAVT (01.2017) | — 0,6 | 0.6 (conservative) 1.4 (basic) | 1.7 (conservative) 2.2 (basic) |

| World Bank (06.2017) | — 1,9 | 1,1 | 1,8 |

| European Commission | — | 1,7 | 1,6 |

| IMF (10.2017) | — 0,8 | 1,1 | 1,2 |

| Agency Standart & Poor's (10.2017) | — | 1,4 | 1,7 |

| Fitch Agency (10.2017) | — 0,8 | 2,0 | 2,1 |

In Russian practice, when developing planning documents, three main scenarios for the development of a territory are often distinguished:

- 1) inertial scenario - development oriented municipality under the influence of the trends prevailing at the beginning of the forecast period, it assumes sluggish processes of reforming economic relations, the conservation of existing contradictions, a passive attitude towards the future of the municipality on the part of the subjects of territorial planning and management;

- 2) recovery scenario - presupposes a transition from an inertial to an innovative way. At this stage, a reserve or the so-called critical mass is being formed for the transition of the economy to a new level of development, including new forms and methods of promoting local producers in foreign markets, the development of production clusters;

- 3) innovative scenario - focused on the trajectory of development of the municipality, which is fundamentally different from the preplanned period. It involves the modernization of the economy, as well as the formation of new relations between the civil society, business and government.

For the first two of the three scenarios, it is necessary to formulate the following scenario conditions:

- 1. Inertial (base) scenario. The tendency of the development of the municipality will continue, the approved measures and the current target programs included in the budget will be implemented. Forecasting methods - trend method.

- 2. Recovery script. In addition to the existing target programs, all activities of the Social and Social Program will be adopted and implemented. economic development municipality. Forecasting methods - expert assessment method, trend method.

To calculate the forecast parameters in the scenarios, the following economic assumptions should also be taken into account:

- 1. For inertial scenario:

- - the crisis is over, the rate of decline in manufacturing industries in the economy of the Russian Federation as a whole has slowed down;

- - no significant economic growth is expected for the next year or two, without taking into account the implementation of key activities of the developed Program, including subprograms.

- 2. For recovery scenario:

- - separate subprograms will be successfully implemented;

- - at the stage of organizing the events of the Program, the rates of economic growth (including industrial production, construction, small business) will be minimal or there will be a slight drop;

- - as a result of the implementation of the subprograms, growth rates by sectors of the economy will be noted.

As the main indicators of changes in social economic situation in the municipality, you should choose:

- - the volume of industrial production;

- - retail trade turnover;

- - the volume of investments (in fixed assets) from all sources of financing, including small businesses;

- - the number of people employed in the economy, including in small business;

- - real disposable cash income of the population, in% of the previous year;

- - an increase in the revenues of the municipal budget (an increase in the share of own revenues, a decrease in subsidies for equalizing the city's budget).

In the process of writing scenarios for the development of a municipality, it is necessary to take into account the following:

- 1. For inertial scenario as a basis, one should take the forecast developed by the employees of the administration of the municipality. Correct taking into account the opinion of specialists (experts) - project executors.

- 2. Forecast indicators for recovery scenario must be done using the above two methods. At the same time, the trend method is first applied, which takes into account the trends of the country's macroeconomic development (for example, data on the main indicators of the socio-economic development of Russia for 9 months of the current year) and forecasts of the Ministry of Economic Development of the Russian Federation (inflation rate, decline in GDP, industrial production, federal budget revenues ).

- 3. Forecast for recovery scenario must be finally agreed with the economists of the administration of the municipality: the deputy head of the administration for economic issues, the head of the department of architecture and urban planning, the management committee municipal property... The forecast of the indicators of the municipal budget must be coordinated in detail and adjusted with the finance department. Thus, in the process of developing a recovery scenario, the maximum number of departments and divisions of the administration should be involved.

- 4. To check the assumptions about tax revenues received additionally from the implementation of program activities, it is necessary to make a calculation taxable base on budget-forming taxes of the municipality.

V forecasting process for the municipality, as mentioned above, two methods must be used:

- 1) method of expert assessments, based on the opinion of experts, i.e. specialists in the field of economics and management;

- 2) trend method- a quantitative forecasting method, which is based on taking into account trends in changes in any indicator or event over previous periods. Based on this, the trend is extrapolated to future periods.

The predicted values of the indicators of the development of the municipality must be presented in a tabular form (Table 10).

Table 10.

Forecasted values of indicators of the development of the municipality according to two scenarios

|

Index |

Scripts |

Reporting |

Forecast period |

Total for 3 years,% |

||||

|

||||||||

|

The volume of goods (works, services) shipped in the field of industrial production, in current prices | ||||||||

|

Restorative |

||||||||

|

Industrial production index | ||||||||

|

Restorative |

||||||||

|

Construction,% to the previous year in comparable prices | ||||||||

|

Restorative |

||||||||

|

Commissioning of residential buildings | ||||||||

|

Restorative |

||||||||

|

Turnover retailers in current prices |

||||||||

|

In comparable prices, in% to the previous year | ||||||||

|

Restorative |

||||||||

|

The number of small enterprises (SE) - total | ||||||||

|

Restorative |

||||||||

|

Quantity individual entrepreneurs |

||||||||

|

Average number of workers employed at small enterprises - total | ||||||||

|

Restorative |

||||||||

|

Volume of goods and services sold by small businesses | ||||||||

|

Restorative |

||||||||

To visualize the results of the scenario, the data of the forecast results should be presented in graphical form: line graph, histogram and bubble chart.

Special attention in the development of scenarios for the development of the municipality should be given to budget indicators. In public administration, this is of key importance. In the practice of commercial companies, this is not so important, since planning is not strictly carried out, financing of expenses depends on sales proceeds. Financial solutions are often accepted promptly. On the contrary, in large corporations, as well as federal, regional and local budgets, they are distinguished by a special (strict) discipline of execution. All changes go through a certain procedure and are approved in the form of a law ( state level) or decisions (municipal level) adopted by legislative bodies: the Federal Assembly or meetings of local deputies (municipal level).

Here it is advisable to predict the indicators of revenues and expenditures of the municipal budget according to two scenarios - the baseline and the recovery (Table 11).

Table 11.

Municipal budget indicators

_(thousand roubles.)

|

Index |

Scripts |

Reporting period |

Forecast period |

|||

|

1. Budget revenues - total |

||||||

|

Restorative |

||||||

|

Tax and non-tax income (own funds) |

||||||

|

Restorative |

||||||

|

Including: |

||||||

|

tax |

||||||

|

Restorative |

||||||

|

non-tax |

||||||

|

Restorative |

||||||

|

The volume of non-refundable receipts |

||||||

|

Restorative |

||||||

|

Index |

Scripts |

Reporting period |

Forecast period |

|||

|

(funds received within the framework of inter-budgetary relations) |

||||||

|

Including: |

||||||

|

subsidies and subventions |

||||||

|

subsidies for equalizing budgetary security |

||||||

|

2. Costs |

||||||

|

budget - total |

Restorative |

|||||

|

3. Scarcity |

||||||

|

Restorative |

||||||

|

4. Share of own |

||||||

|

military income in total amount budget revenues,% |

Restorative |

|||||

The baseline budget figures are presented based on the official forecast, which is based on the index method. The recovery scenario was calculated by adding the effect of the implementation of individual subprograms of the municipality. Further, adjustment by the expert method is possible.

- See: Formation of comprehensive programs for the socio-economic development of municipalities: a teaching aid / V. I. Ivankov, A. V. Kvashnin, V. I. Psarev, T. V. Psareva; under total. ed. T.V. Psareva. - S. 141.

- Advantages of cottages in our residential complex "Ekodolie Sholokhovo" Profitable mortgage programs

- Residential complex "Novosnegirevsky" (RC "New Snegiri") Environment and transport accessibility

- Residential complex "Vidny Gorod" is frozen

- Advantages of cottages in our residential complex "Ekodolie Sholokhovo"